Top Cheap Places to Buy Verified Huobi Global Accounts

The landscape of cryptocurrency trading has matured significantly since the early days of Bitcoin and its immediate successors. What began as a niche pursuit reserved for hobbyists and tech enthusiasts has transformed into a global financial phenomenon that attracts millions of participants each year. At the heart of this transformation are centralized cryptocurrency exchanges, platforms that facilitate the buying, selling, and exchange of digital assets. Among these exchanges, Huobi Global stands out as one of the more prominent players, having served an international user base and provided access to a broad array of tokens. Like other major exchanges, Huobi implements verification processes for its users,

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

If you want to more information just contact now.

24 Hours Reply/Contact

➤E-mail: topusaproy@gmail.com

➤WhatsApp: +1 (314) 489-2815

➤Telegram: @topusapro

➤Our Websites: www.topusapro.com

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

requiring individuals to undergo identity checks before they can access advanced features or higher withdrawal limits. This system, commonly referred to as Know Your Customer or KYC, has become an industry standard intended to comply with international financial regulations and to protect users and institutions alike from misuse of financial infrastructure. However, alongside the legitimate processes sanctioned by exchanges, a parallel shadow market has emerged, offering “verified accounts” for sale. These schemes typically promise instant access to a fully activated exchange account without the buyer having to go through the official verification procedures themselves. On the surface, such offers may sound attractive to those frustrated by slow or intrusive verification, but beneath the surface lies a complex web of deception, legal violations, systemic risk, personal peril, and long-term consequences that far outweigh any perceived convenience.

To understand the dangers and impropriety of buying verified Huobi accounts, one must first grasp why exchanges implement verification in the first place. When a user signs up for an exchange like Huobi, they are entering into a contractual relationship with the platform. The terms of service that govern this relationship outline the responsibilities and rights of both parties. Central to these agreements is the requirement that users provide accurate identification information and verify that they are who they claim to be. Exchanges use this information to comply with anti-money-laundering laws, counter-terrorism financing regulations, and other financial compliance frameworks that have been introduced globally in response to risks posed by unregulated financial channels. Verification is not merely bureaucratic red tape; it is a mechanism intended to ensure that financial platforms can deter and detect criminal activity, protect legitimate users, and maintain the integrity of the broader financial ecosystem. Without such measures, exchanges could unwittingly become conduits for fraud, illicit transfers, and other forms of financial abuse. Verification protects not only the exchange’s legal standing but also the interests of the users by enabling the platform to provide recourse when accounts are compromised or when disputes arise.

Despite these safeguards, some users find themselves impatient with official channels or intimidated by the verification process. Whether due to poor documentation, lack of familiarity with the required procedures, or fears about data privacy, they may be tempted by offers that promise to eliminate the need for verification altogether. Third-party sellers may advertise “verified Huobi accounts” that have already passed KYC checks and are available for immediate use. These accounts are often marketed through social media groups, online forums, or encrypted messaging channels, where anonymity and distance from regulatory oversight make it easier for scammers to operate. The premise is simple: for a fee, usually payable in cryptocurrency or another untraceable form, the buyer receives the login credentials to an account that has already been through the verification process. The allure of bypassing bureaucratic wait times or avoiding identity checks can be tempting, especially for inexperienced users eager to get started with trading or accessing certain features. Yet the reality is that these schemes are fundamentally incompatible with the rules of the exchange, the broader legal frameworks governing financial activities, and the basic principles of digital security.

The first major issue with buying a verified account from an external seller is that it violates the terms and conditions of the cryptocurrency exchange. Most reputable platforms explicitly state that accounts are non-transferable and that they must be maintained and used only by the verified individual whose identity is tied to the account. This clause is included to prevent misuse, protect user data, and uphold compliance standards. When an account is transferred or sold to another person, the foundational assumption of the verification process, that the verified identity matches the actual operator of the account, is breached. The exchange therefore views such activity as a violation of its user agreement, and the consequences can range from immediate account suspension to permanent bans. This contractual violation puts the buyer in a precarious legal position because they are knowingly using a service in a manner that the provider expressly prohibits. The exchange’s algorithms and compliance teams are equipped to detect irregular patterns, such as sudden changes in login location, device fingerprints, or unusual trading behavior. When such anomalies are detected, the account may be flagged for review, frozen, or terminated, often without warning. Users who obtain accounts through illicit channels may find themselves locked out with no recourse, as they cannot legitimately prove ownership or provide valid identification when the platform requests it.

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

If you want to more information just contact now.

24 Hours Reply/Contact

➤E-mail: topusaproy@gmail.com

➤WhatsApp: +1 (314) 489-2815

➤Telegram: @topusapro

➤Our Websites: www.topusapro.com

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

Beyond the contractual breaches, there are significant legal and ethical dimensions to consider. Financial regulations in many countries require that identity verification be performed on individuals who engage in trading activities, especially when fiat currency is involved or when certain transaction thresholds are crossed. These regulations have been put in place to prevent money laundering, tax evasion, and other forms of financial crime. When a user purchases access to a verified account, they are effectively impersonating someone else in the financial system. Depending on the jurisdiction, this can constitute fraud, identity theft, or other criminal offenses. Law enforcement agencies take cases of financial fraud seriously, and the penalties can include substantial fines or even imprisonment. Even if the buyer at first assumes they are merely participating in a harmless shortcut, they are engaging in activity that undermines regulatory compliance and potentially violates statutory provisions designed to protect the financial system and its participants.

The way these verified account schemes typically operate is inherently deceptive and fraught with technological and security risks. Sellers often acquire accounts through illicit means, such as using stolen identification documents, creating synthetic identities, or exploiting lax verification processes on other platforms. Once an account has been verified under false pretenses, it is then offered to unsuspecting buyers. In some cases, the seller merely provides login credentials, while in others they may offer a temporary window of access before reclaiming the account. Because the original identity documentation belongs to someone else, the account remains tied to that identity in the exchange’s records. This means that the seller retains indirect control through recovery information, linked email addresses, or other associated credentials. Should the buyer deposit funds into the account, those assets could be at risk of seizure by the original owner, reclaimed by the seller, or frozen by the exchange upon detection of suspicious activity. The entire transaction is built on a foundation of deceit, and there is no guarantee that the buyer will retain access or that the account will remain functional for any length of time.

In practice, many buyers have reported waking up one day to find their access abruptly terminated, their funds inaccessible, and their attempts to seek support ignored or dismissed. Because the buyer is not the verified owner of the account, they lack the documentation necessary to satisfy the exchange’s support or recovery processes. Customer service teams are trained to protect user accounts and sensitive data, and they cannot provide access to someone who cannot authenticate as the legitimate account holder. As a result, funds stored in these illicitly obtained accounts can be lost permanently, without any mechanism for reimbursement or dispute resolution. The financial loss is compounded by the fact that the buyer’s original payment to the seller is usually irreversible, especially when made in cryptocurrency or through untraceable means. There is no bank to contest the charge, no intermediary to mediate, and no regulatory body to enforce restitution.

Aside from the immediate financial loss and account termination, there are deeper, more insidious consequences for individuals who engage in these schemes. The act of using someone else’s verified identity in a financial context can create a digital footprint that binds the buyer to fraudulent activity. Should law enforcement or regulatory agencies investigate suspicious transactions, the digital trail may lead back to the user’s device, IP address, or other identifiable information. This can place the individual under scrutiny for broader networks of fraud or money laundering, even if their participation was limited to acquiring a supposedly verified account. Digital forensics tools are sophisticated and capable of reconstructing activity across multiple platforms, especially when cross-referenced with data from compromised exchanges or third-party sources. The buyer may find themselves subject to civil or criminal investigation, with little opportunity to explain that they were unaware of the legal implications of their actions.

The systemic impact of these illicit markets extends beyond individual cases. When third-party actors traffic in verified accounts, they undermine the integrity of the entire verification ecosystem. Exchanges invest heavily in compliance infrastructure to satisfy regulatory demands and to secure their platforms from exploitation by bad actors. When verified accounts are bought and sold, it signals that these safeguards have been bypassed, creating potential loopholes that criminals could exploit to launder funds, move assets under false pretenses, or evade sanctions. This not only harms the reputation of the exchange but also shakes the confidence of regulators and legitimate users. Financial systems, whether traditional banks or emerging cryptocurrency platforms, rely on trust. When trust is eroded by fraudulent practices, the cost of doing business increases for everyone, as exchanges must divert more resources to address abuses and maintain compliance.

Critically, there is also a personal data privacy risk associated with these schemes. In some cases, sellers may retain copies of identifying information used to verify the account, meaning that sensitive data such as names, birthdates, or even government identification numbers remain accessible to unauthorized parties. This creates a risk not only for the original identity owner, whose information has been misused, but also for the buyer, whose interaction with the seller exposes them to potential data breaches, phishing, or other forms of cybercrime. The web of deception in these schemes is not limited to financial loss; it extends into the realms of identity theft, digital surveillance, and long-lasting harm to personal reputation.

Understanding these risks leads to the acknowledgment that there is no legitimate shortcut around verification. Centralized exchanges have little choice but to enforce strict identification protocols if they are to operate within the legal frameworks of multiple jurisdictions. While the process may feel intrusive or slow to some users, it exists to protect both the platform and its customers. Verification ensures that if something goes wrong, there is a verifiable human being behind the account who can be contacted, held accountable, or assisted in case of security incidents. It also allows for regulatory reporting in situations where suspicious activity meets thresholds that necessitate disclosure to authorities. These protections are part of a larger infrastructure that enables cryptocurrency trading to coexist with established financial and legal norms. Far from being an optional inconvenience, verification is a foundational element of a secure and compliant exchange.

For users frustrated with verification delays, there are legitimate ways to improve the process and avoid falling prey to illicit account sellers. Preparing accurate documentation, following the exchange’s stated guidelines, and reaching out to official support channels if verification becomes stalled can often resolve issues more efficiently than turning to third-party offers. Many exchanges have dedicated verification support teams precisely because they recognize that users may need assistance, and these teams operate within the framework of regulatory compliance. Moreover, some regions have local exchanges that offer streamlined processes tailored to residents, potentially reducing wait times and documentation burdens. Peer-to-peer trading platforms also exist that do not require the same level of centralized verification, though they trade off certain protections and features for flexibility. The critical point is that all legitimate pathways to access cryptocurrency markets involve working within the rules established by platforms and legal systems rather than circumventing them through prohibited schemes.

Another dimension to consider is the reputational damage a user may suffer by associating with illicit activity. Even if the individual never faces legal prosecution, being linked to fraudulent schemes can harm future opportunities in the broader financial and tech industries. References to compromised accounts, suspicious transactions, or participation in black market activities may surface on platforms that share reputation data, potentially limiting the individual’s ability to open accounts on other exchanges or engage in financial services in the future. Reputation systems in digital finance are becoming more sophisticated, and bad actors are increasingly flagged across interconnected networks of exchanges and service providers. This can create long-term barriers that far outlast the immediate financial loss incurred from a frozen account.

Some might argue that the prevalence of these illicit markets is a symptom of broader systemic issues, such as overly burdensome verification procedures or lack of access for certain populations. While it is true that digital identity infrastructure and regulatory environments vary across countries, the answer to these challenges should not be to seek shortcuts that undermine fundamental legal and ethical norms. Instead, industry stakeholders must work toward more inclusive, efficient, and secure verification systems that respect user privacy while satisfying compliance imperatives. Emerging technologies such as decentralized identity frameworks offer promise in this regard, enabling users to verify their identity in a privacy-preserving manner without compromising regulatory oversight. These systems still require rigorous design and broad adoption, but they represent a direction that aligns user needs with legal obligations rather than pitting one against the other.

In reflecting on the reasons why buying a verified Huobi account is risky and prohibited, it becomes clear that the issue is not simply about personal inconvenience or frustration with a process. It is about recognizing that financial systems, digital or otherwise, must operate within a framework of trust, accountability, and legal compliance. Verification is one of the cornerstones of that framework, connecting digital activity to real human agents in a way that enables both security and accountability. When individuals attempt to bypass these linkages through third-party schemes, they are not only flouting the rules of a single platform, they are participating in a practice that erodes the foundations of trusted finance. The short-term gain of instant access, if it is even realized, comes at the expense of long-term risk: financial loss, legal jeopardy, compromised personal data, reputational harm, and the broader weakening of trust in the digital financial ecosystem.

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

If you want to more information just contact now.

24 Hours Reply/Contact

➤E-mail: topusaproy@gmail.com

➤WhatsApp: +1 (314) 489-2815

➤Telegram: @topusapro

➤Our Websites: www.topusapro.com

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

The message that must be communicated to anyone considering such schemes is straightforward but profound. There is no legitimate way to circumvent verification on a regulated cryptocurrency exchange. Attempting to do so is inherently risky, often illegal, and almost always counterproductive. Those who value their financial security, their legal standing, and their future opportunities would do well to engage with cryptocurrency platforms responsibly, respecting both the letter and spirit of the agreements they enter into. By doing so, they contribute to a more secure, fair, and sustainable financial future for all participants in the digital economy.

閱讀更多

According to a new report from Intel Market Research, Global Medical Packaging Transparent Deposition Film market was valued at USD 709 million in 2024 and is projected to reach USD 1,122 million by 2031, growing at a robust CAGR of 6.9% during the forecast period (2025–2031). 📥 Download Sample Report: Medical Packaging Transparent Deposition Film Market - View in Detailed Research...

Buy New & Old Twitter Accounts Are you looking to expand your social media presence quickly and effectively? Buying new or old Twitter accounts might be the solution you’ve been searching for. Whether you’re a business aiming to connect with a larger audience or an individual wanting to boost your personal brand, acquiring established Twitter accounts can save you time...

Hoyoverse hat kürzlich eine offizielle Präsenz in den sozialen Medien für Astra Yao eingerichtet, eine neu vorgestellte Figur aus dem Handyspiel Zenless Zone Zero. Die Bekanntgabe erfolgte im Rahmen eines Trailers bei den Game Awards 2024, wodurch die Fans erstmals einen Blick auf den Charakter werfen konnten. Astra wird ihr spielbares Debüt im Spiel mit dem nächsten...

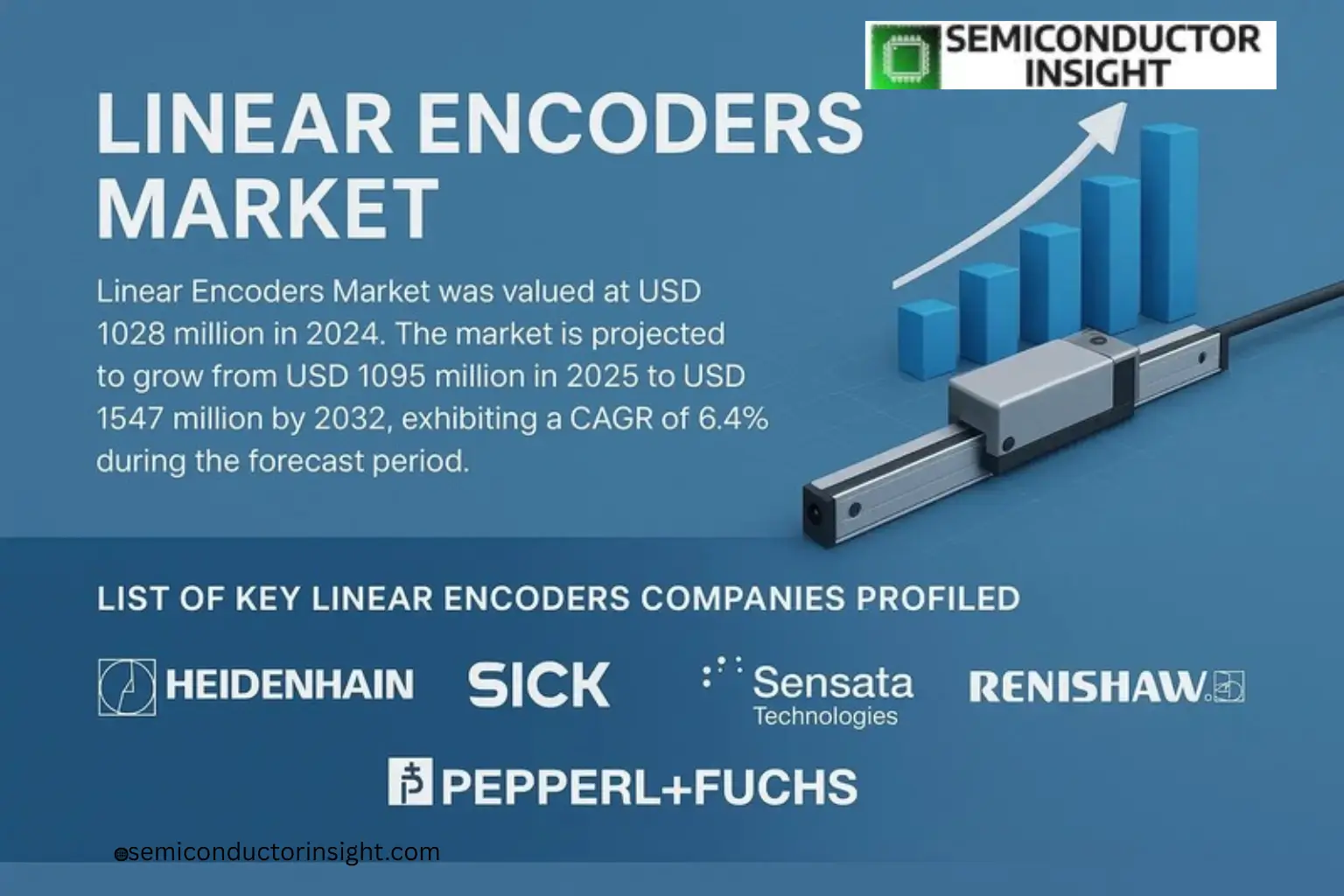

Linear Encoders Market, valued at a robust USD 1028 million in 2024, is poised for a steady growth trajectory, projected to grow from USD 1095 million in 2025 to USD 1547 million by 2032, according to a comprehensive new report published by Semiconductor Insight. This expansion, representing a compound annual growth rate (CAGR) of 6.4%, underscores the increasing reliance on...