How to Safely Use Zelle for Business Transactions (2025 ...

In the modern digital economy, peer-to-peer payment systems have become deeply integrated into everyday financial life. Among these systems, Zelle occupies a unique position. Unlike standalone wallets or independent payment processors, Zelle operates directly within the U.S. banking system, allowing instant transfers between participating banks using verified bank accounts. Because of its speed, convenience, and direct connection to bank balances, Zelle is widely trusted by consumers and increasingly attractive to individuals seeking fast payments for online sales, services, and informal commerce. This demand has given rise to illicit offers claiming to sell “verified Zelle accounts,” often

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

If you want to more information just contact now.

24 Hours Reply/Contact

➤E-mail: topusaproy@gmail.com

➤WhatsApp: +1 (314) 489-2815

➤Telegram: @topusapro

➤Our Websites: www.topusapro.com

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

marketed alongside Instagram accounts or described as “trade with Insta” packages. These schemes promise immediate access to Zelle without bank verification, appealing to those who want to receive payments quickly or avoid scrutiny. Despite these claims, buying verified Zelle accounts is strictly prohibited, exceptionally dangerous, and almost always results in severe financial, legal, and reputational consequences. What appears to be a shortcut is, in reality, one of the fastest ways to invite banking bans, frozen funds, and long-term financial exclusion.

To understand why buying verified Zelle accounts is so risky, it is essential to understand what Zelle actually is and how it functions. Zelle is not a merchant processor or a transferable wallet service. It is a bank-to-bank transfer network owned and governed by U.S. financial institutions. Each Zelle profile is directly linked to a real bank account held in a real individual’s or business’s name. That bank account has already undergone identity verification, regulatory screening, and compliance checks under federal banking laws. When a user enrolls in Zelle, they are not creating an independent account; they are extending their bank identity into the Zelle network. This means that Zelle verification is inseparable from bank verification. There is no legitimate mechanism by which a Zelle account can be sold, transferred, rented, or reassigned to another person.

When someone attempts to buy a verified Zelle account, they are not merely violating an app’s terms of service. They are attempting to gain unauthorized access to a regulated bank account or to a bank-linked payment channel. This is fundamentally different from misusing a social media platform or even a standalone payment wallet. Banks are legally required to know who controls accounts and how funds move through them. Any attempt to disguise the true user of a bank-linked service directly conflicts with anti-money-laundering regulations, fraud prevention laws, and consumer protection rules. For this reason, Zelle and its participating banks enforce strict prohibitions against account sharing, third-party usage, and commercial misuse.

Despite these realities, underground markets continue to advertise verified Zelle accounts as if they were commodities. These schemes typically target individuals involved in online selling, social media commerce, digital services, or arbitrage activities who want instant payment acceptance without delays. The inclusion of Instagram in these offers is deliberate. Instagram is often perceived as a storefront, and sellers exploit this perception by marketing Zelle accounts as payment rails that can be seamlessly paired with social media sales. The phrase “trade with Insta” is used to suggest legitimacy, speed, and ease, implying that buyers can immediately receive customer payments through direct bank transfers. What these offers hide is that every such transaction is built on deception and unauthorized access.

The methods used to create and sell verified Zelle accounts are inherently fraudulent. In some cases, sellers recruit individuals to open bank accounts in their own names and enroll them in Zelle, then hand over login credentials to buyers. These individuals may be paid small sums and told that the risk is minimal, even though they remain legally responsible for all activity conducted through the account. In other cases, accounts are compromised through phishing, social engineering, or malware, and then resold without the original owner’s consent. There are also scenarios where fake or stolen identities are used to open bank accounts, though this is far riskier and more likely to trigger immediate detection. Regardless of the method, the buyer always ends up controlling an account that is legally owned by someone else.

Bundling Instagram accounts with Zelle access increases the illusion of a complete business setup. Sellers imply that the buyer is acquiring not just a payment channel but a ready-made commerce system. In reality, the Instagram accounts included in these packages are often themselves purchased, hijacked, or created using false information. Using such accounts violates Instagram’s policies and exposes the buyer to enforcement actions on that platform as well. When a payment account and a social media account are both operating under false ownership, the risk compounds. A customer complaint, disputed payment, or report of suspicious activity can quickly lead to investigations across platforms, unraveling the entire scheme.

Banks and Zelle have sophisticated monitoring systems designed to detect exactly this kind of misuse. These systems analyze transaction patterns, transfer frequency, payment descriptions, geographic access data, device fingerprints, and behavioral anomalies. Zelle is designed primarily for personal transfers and limited business use under specific conditions. When an account suddenly begins receiving frequent payments from unrelated individuals, especially with notes suggesting sales activity, it raises immediate red flags. If login behavior indicates access from different locations or devices inconsistent with the account holder’s profile, suspicion increases further. Purchased accounts almost always exhibit such anomalies because the buyer’s behavior does not match the verified owner’s normal financial profile.

Once suspicious activity is detected, the response is often swift. Banks may restrict or close the underlying bank account, disable Zelle access, and freeze funds pending investigation. Unlike disputes with standalone platforms, bank actions are difficult to reverse. Funds may be held for extended periods or returned to senders, leaving the buyer without access to money they believed they had earned. Because the buyer is not the legal account holder, they cannot communicate effectively with the bank to resolve the issue. Customer service will only speak with the verified account owner, whose identity is on record. This leaves the buyer powerless as funds are frozen and accounts are closed.

The financial consequences of these actions can be devastating. Many individuals using illicit Zelle accounts rely on fast cash flow to sustain their activities. When funds are frozen, obligations to customers, suppliers, or partners cannot be met. Refunds may be impossible, leading to disputes and complaints. Advertising expenses may continue while income disappears. In some cases, banks may debit accounts to reverse transactions or cover losses, pushing balances negative and creating additional liabilities. For buyers who invested heavily in scaling operations using a purchased account, the collapse can be sudden and total.

Legal consequences are even more serious. Unauthorized use of a bank account or bank-linked payment service can constitute fraud, identity theft, wire fraud, and conspiracy, depending on jurisdiction and circumstances. Banks are obligated to report suspicious activity to regulatory authorities. Once reported, investigations can involve transaction histories, IP addresses, device data, and communication records. Buyers may find themselves questioned by banks, law enforcement, or regulatory bodies. Even if the buyer did not personally create the fraudulent account, knowingly using an account that does not belong to them can still result in legal liability. Claiming ignorance rarely provides protection, particularly when transactions show clear signs of intentional misuse.

Tax implications further complicate matters. Zelle transactions are tied directly to bank accounts, which are subject to tax reporting obligations. Income received through a purchased account is attributed to the account holder of record, not the buyer. This creates discrepancies between actual income earned and income reported to tax authorities. Such discrepancies can trigger audits, penalties, and allegations of tax evasion. Attempting to explain that the income flowed through someone else’s account because it was purchased does not mitigate the issue and may instead confirm deliberate noncompliance. Resolving tax disputes can be costly, time-consuming, and emotionally draining.

For businesses, the long-term damage can be irreversible. Banks share risk information and maintain internal records of customers involved in fraudulent or noncompliant activity. Being associated with Zelle misuse can lead to account closures across multiple banks, not just one institution. Individuals may be denied the ability to open new bank accounts, a situation often referred to as banking exclusion. Without access to basic banking services, operating a legitimate business becomes nearly impossible. Even personal financial life can be severely impacted, affecting housing, employment, and credit access.

Reputational damage adds another layer of harm. Customers expect professionalism and reliability when sending money. When payments are reversed, accounts disappear, or sellers suddenly become unreachable, trust evaporates. Negative reviews, social media complaints, and public accusations of fraud can spread quickly. If the Instagram account used for sales is also suspended or shut down, the loss of visibility and communication channels compounds the damage. Rebuilding a reputation after such events is extraordinarily difficult, especially when the underlying cause involves intentional misuse of financial systems.

Security risks inherent in buying verified Zelle accounts are often underestimated. Sellers frequently retain some level of control, whether through access to the bank account recovery process, knowledge of security questions, or influence over the original account holder. This means the buyer never truly controls the account. At any moment, access can be revoked, funds withdrawn, or the account reported. In some cases, sellers intentionally wait until significant balances accumulate before reclaiming the account. Buyers may also expose themselves to malware, phishing, or surveillance during the acquisition process, leading to further identity theft and financial loss.

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

If you want to more information just contact now.

24 Hours Reply/Contact

➤E-mail: topusaproy@gmail.com

➤WhatsApp: +1 (314) 489-2815

➤Telegram: @topusapro

➤Our Websites: www.topusapro.com

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

Operating under constant risk takes a psychological toll. Fear of detection encourages short-term thinking and risky behavior, such as rushing transactions, avoiding customer communication, or limiting growth to stay under perceived thresholds. This mindset undermines sustainable business development and leads to burnout. Even if enforcement actions are delayed, the constant uncertainty prevents long-term planning and investment. A business built on an illicit foundation cannot achieve stability, regardless of short-term gains.

Many individuals are drawn to these schemes because legitimate payment onboarding can feel restrictive. Banks impose rules, limits, and reviews that may frustrate those seeking speed or anonymity. However, these requirements exist to protect the financial system and its users. Attempting to bypass them through purchased accounts does not remove scrutiny; it merely postpones it while magnifying the consequences. Legitimate alternatives exist, including using approved payment processors for business transactions, complying with bank requirements, and structuring operations transparently. While these paths may require patience, they provide long-term security and access to financial services.

From an ethical perspective, buying verified Zelle accounts undermines trust in the banking system. Peer-to-peer payment networks rely on honest participation and accurate identity representation. Abuse of these systems leads to stricter controls, reduced limits, and increased scrutiny for everyone, including legitimate users. Participation in illicit schemes contributes to a cycle of tightening regulation that ultimately harms the broader community.

The belief that a purchased Zelle account can operate indefinitely without detection is a dangerous illusion. Banks continuously refine their monitoring tools and conduct retrospective reviews. An account that appears functional today may be flagged months later due to changes in behavior, customer complaints, or external investigations. When enforcement occurs at a later stage, the financial losses and legal exposure are often far greater than they would have been earlier. Delayed detection creates false confidence that encourages deeper entanglement in an unsustainable setup.

At its core, buying a verified Zelle account, especially when marketed as a “trade with Insta” solution, reflects a fundamental misunderstanding of what Zelle is. Zelle is not a product that can be transferred or resold. It is an extension of a verified bank identity. Attempting to purchase access to that identity does not confer legitimacy or protection. It only creates a fragile illusion that collapses under scrutiny. The financial system is designed specifically to identify and dismantle such arrangements.

In conclusion, buying verified Zelle accounts, including those bundled with Instagram or promoted as social commerce shortcuts, is risky, prohibited, and ultimately self-destructive. These schemes rely on deception, unauthorized access, and violations of banking rules. Buyers face frozen funds, legal consequences, reputational harm, security risks, and long-term exclusion from essential financial services. What may appear to be a convenient workaround is, in reality, one of the fastest paths to financial instability and lasting damage. Sustainable success in online commerce and digital finance can only be achieved through transparency, compliance, and respect for the rules that govern bank-linked payment systems.

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

If you want to more information just contact now.

24 Hours Reply/Contact

➤E-mail: topusaproy@gmail.com

➤WhatsApp: +1 (314) 489-2815

➤Telegram: @topusapro

➤Our Websites: www.topusapro.com

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

分类

閱讀更多

Comprehensive Outlook on Executive Summary Non Alcoholic Beverages Market Size and Share Global non alcoholic beverages market size was valued at 1,796.60 Billion in 2024 and is projected to reach USD 2614.16 Billion by 2032, with a CAGR of 4.80% during the forecast period of 2025 to 2032 A competitive era calls for businesses to be equipped with acquaintance of the major happenings...

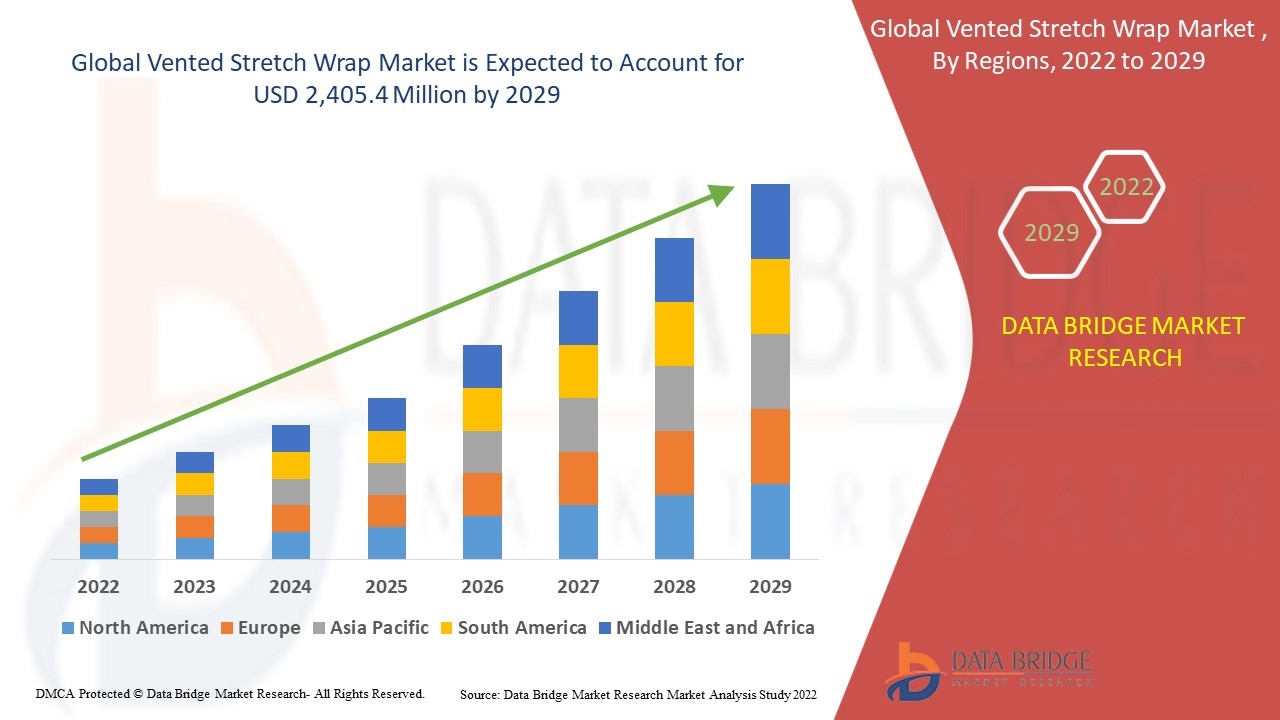

"Comprehensive Outlook on Executive Summary Vented Stretch Wrap Market Size and Share CAGR Value Data Bridge Market Research analyses that the vented stretch wrap market will witness a CAGR of 6.2% for the forecast period of 2022-2029 and is likely to reach at USD 2,405.4 million by 2029. For powerful business growth, companies must take up market research report service which has...

Introduction to Buying Verified Paytm Accounts and Digital Payment Usage Verified Paytm accounts are widely discussed in India’s digital economy because Paytm enables mobile payments, banking services, and everyday financial transactions across millions of users. Rapid Growth of Paytm in Digital India Paytm has become a central pillar of India’s cashless movement,...

Buy Edu Email If you want to buy Edu emails instant for unlocking educational and resources, and want to connect with businesses, place your order at Bestpvaservice.COM . Edu emails can unlock exclusive benefits for businesses. So, buy Edu emails instant of all country including USA, UK and others. 🤨🙌✊🫱 ➤💼If you want to more information just knock us 🤨🙌✊🫱...