Best place to buy Verified Revolut accounts in USA ...

Buy Verified Revolut Accounts: Understanding Risks, Compliance Realities, and Long-Term Consequences in Digital Banking

Buying verified Revolut accounts attracts attention because people seek faster access to financial features, yet this shortcut introduces serious legal and security risks.

Revolut operates as a regulated financial institution, meaning account ownership, identity verification, and usage are governed by strict compliance obligations.

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

✅⇒Order Now: https://smmusaall.com/

✅⇒24-hour Reply/Contacts

✅⇒Whatsapp:+1 (314) 489-2815

✅⇒Telegram: @smmusaall

✅⇒Telegram: @smmusaall

✅⇒Telegram Link: @smmusaall

✅⇒Whatsapp::+1 (314) 489-2815

✅⇒Website Visit Now:

▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

Verified accounts are permanently linked to the individual whose documents passed know your customer checks during the original onboarding process.

When such accounts are sold or transferred, the buyer never becomes the legitimate owner in the eyes of Revolut systems.

This ownership mismatch creates immediate vulnerability, because Revolut prioritizes verified identity holders during disputes, reviews, and security investigations worldwide today.

Many sellers advertise fully verified Revolut accounts, but buyers cannot confirm how identities were obtained or whether documents were authentic.

Using accounts verified under another person exposes buyers to accusations of impersonation, fraud, or facilitating financial misconduct under regulatory scrutiny.

Revolut continuously monitors login behavior, device fingerprints, transaction patterns, and geographic consistency to detect unauthorized account control changes promptly globally.

Sudden changes in location, spending habits, or security settings often trigger enhanced reviews resulting in account freezes and fund restrictions.

Even if purchased accounts function initially, delayed enforcement frequently occurs, locking balances and limiting access without meaningful appeal options available.

Financial risk becomes extreme when funds are frozen, because buyers cannot prove rightful ownership during compliance investigations conducted internally repeatedly.

Most marketplaces selling Revolut accounts operate anonymously, offering no legal protection, customer support, or reimbursement guarantees to buyers whatsoever globally.

Scams are widespread, including recycled accounts, stolen identities, or credentials resold to multiple buyers simultaneously through underground marketplaces online today.

Security settings like two factor authentication may remain partially controlled by original owners, increasing recovery and takeover risks significantly over time.

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

✅⇒Order Now: https://smmusaall.com/

✅⇒24-hour Reply/Contacts

✅⇒Whatsapp:+1 (314) 489-2815

✅⇒Telegram: @smmusaall

✅⇒Telegram: @smmusaall

✅⇒Telegram Link: @smmusaall

✅⇒Whatsapp::+1 (314) 489-2815

✅⇒Website Visit Now:

▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰▰

⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐⭐

Buyers often underestimate Revolut’s ability to correlate behavioral data with verified identities across devices and sessions continuously and accurately worldwide.

When discrepancies appear, Revolut prioritizes regulatory compliance over user convenience, regardless of how much money is involved legally required standards.

Appeals processes require identity verification documents that buyers cannot legitimately provide, resulting in permanent account closures without exception in practice.

Businesses attempting to use purchased Revolut accounts face heightened risk due to audits, reporting obligations, and partner scrutiny from regulators globally.

Misrepresentation of account ownership can violate contractual agreements, internal compliance policies, and financial crime prevention standards enforced internationally today widely.

Reputational damage follows exposure of illicit practices, reducing trust among customers, investors, and financial partners significantly over timeframes globally.

Operational instability becomes common as buyers cycle through accounts, losing continuity, data access, and transaction history repeatedly without warning signs.

Stress and uncertainty accompany frozen balances, unanswered support requests, and sudden loss of financial access during critical personal situations often.

Community forums contain numerous reports of users losing funds permanently after purchasing verified Revolut accounts from unknown sellers online marketplaces.

Revolut support responses consistently reference terms violations and identity mismatches when addressing unauthorized account control cases across reported incidents publicly.

Once an account is flagged, recovery options are extremely limited, regardless of balance size or transaction history at that point.

Buyers also risk involvement in identity theft cases if accounts were created using stolen personal information unknowingly or indirectly sometimes.

Such involvement can attract law enforcement attention, even when buyers claim ignorance of account origins during subsequent financial investigations later.

Ignorance rarely protects users within regulated financial systems designed to enforce accountability and traceability across jurisdictions worldwide today increasingly strictly.

Ethical considerations also matter, as misuse undermines trust in digital banking ecosystems built for security and fairness globally today widely.

Revolut and similar institutions implement verification to protect users, prevent fraud, and meet regulatory obligations imposed by authorities worldwide today.

Circumventing these systems weakens collective safety and increases costs passed onto compliant customers through higher fees and restrictions later on.

Long term digital finance adoption depends on transparency, responsibility, and trust between institutions and users operating globally today securely together.

Shortcuts like buying verified accounts damage perception of fairness and slow progress toward inclusive financial systems worldwide over time periods.

Legitimate onboarding provides stability, predictable access, and proper customer support during disputes or emergencies when they arise unexpectedly later on.

Users facing regional limitations should understand that circumvention increases legal exposure rather than solving access challenges sustainably or safely long term.

Regulatory cooperation between financial platforms and authorities continues expanding, reducing tolerance for identity based violations across borders and regions globally.

Detection technology improves constantly, meaning unauthorized accounts that work today may fail suddenly tomorrow without advance notice whatsoever given users.

Blockchain transparency and banking logs further reduce anonymity assumptions often associated with digital finance misuse among inexperienced users online today.

Responsibility follows activity, not convenience, making buyers accountable for transactions conducted through compromised accounts regardless of intent claims later made.

Professional financial planning prioritizes stability, security, and compliance over risky acceleration methods promising short term convenience or speed benefits alone.

Retail users often suffer greatest losses, lacking resources to contest freezes or pursue lengthy legal remedies independently without expert assistance.

Emotional stress compounds financial harm when savings become inaccessible during unexpected enforcement actions affecting livelihoods and families directly sometimes severely.

Forums frequently document regret from individuals who believed sellers promising safe verified Revolut access without long term consequences involved initially.

Support tickets often close with policy references, leaving buyers frustrated and without meaningful resolution options available under current regulations today.

Once trust is broken, rebuilding compliant access requires starting again through legitimate verification channels with patience and documentation readiness fully.

Time spent managing risky accounts could be invested learning financial tools, budgeting, or compliant trading strategies yielding durable skills instead.

Education and compliance provide compounding benefits absent from shortcut approaches reliant on borrowed identities and fragile access arrangements overall today.

Financial institutions design systems assuming long term relationships, not anonymous users rotating through accounts frequently to avoid detection attempts online.

Using purchased accounts contradicts this model, creating friction and enforcement responses that escalate quickly under scrutiny conditions globally today widely.

Long term success in digital banking comes from transparency, patience, and respect for regulatory boundaries established by authorities worldwide today.

分类

閱讀更多

The biomedical industry is experiencing rapid innovation, and resorbable microspheres have become an essential solution for controlled drug delivery and tissue regeneration. These microspheres are widely used for applications including minimally invasive procedures, oncology therapies, and targeted drug release. Their biodegradable nature and compatibility with human tissue make them a...

New Releases on Netflix This week has been particularly exciting for Netflix enthusiasts, with a trio of fresh original films arriving on the platform between November 10 and 14. Each of these movies offers a unique experience, catering to diverse tastes and preferences. Among the latest releases, viewers can expect a variety of genres and storytelling styles, ensuring there's something for...

The Tokenization Market research industry size is expanding rapidly as organizations recognize the critical importance of data security and privacy. Tokenization replaces sensitive information with tokens that retain transactional value but are meaningless to cybercriminals, enhancing enterprise cybersecurity. The market is projected to grow from 3.75 USD Billion in 2025 to 15 USD...

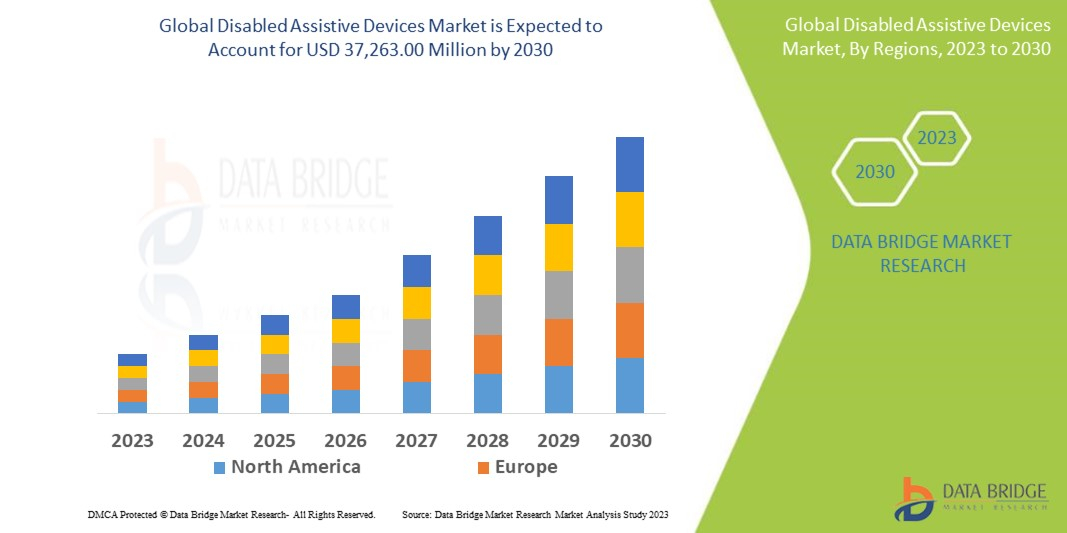

"Key Drivers Impacting Executive Summary Disabled Assistive Devices Market Size and Share CAGR Value The global disabled assistive devices market size was valued at USD 26.64 billion in 2024 and is expected to reach USD 42.14 billion by 2032, at a CAGR of 5.90% during the forecast period Accomplishment of maximum return on investment (ROI) is one of the...