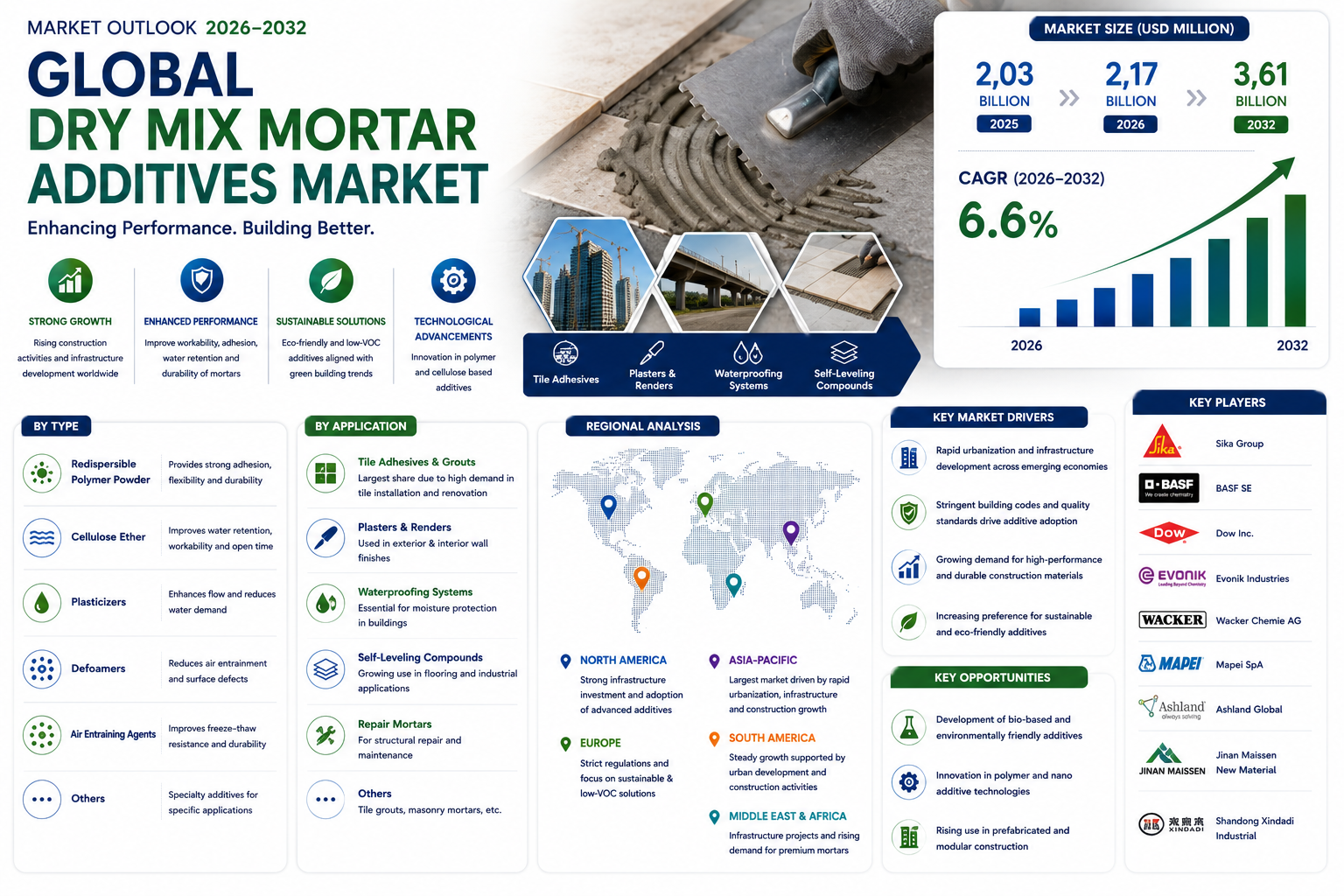

Global dry mix mortar additives market size was valued at USD 2.03 billion in 2025 and is projected to grow from USD 2.17 billion in 2026 to USD 3.61 billion by 2034, exhibiting a CAGR of 6.6% during the forecast period.

Dry mix mortar additives are specialized chemical compounds designed to enhance the performance characteristics of dry mortar mixtures. These additives modify key properties such as workability, adhesion strength, water retention, and setting time, making them indispensable in modern construction applications. The product categories include redispersible polymer powders, cellulose ethers, air-entraining agents, plasticizers, and defoamers, each serving distinct functional purposes in mortar formulations.

The market is experiencing robust growth driven by rapid urbanization and infrastructure development worldwide, particularly in emerging economies. Residential construction dominates application segments, while commercial projects increasingly adopt high-performance mortars with specialized additives. Furthermore, technological advancements in additive formulations enable eco-friendly solutions with reduced VOC emissions, aligning with global sustainability trends. Key industry players like Sika Group, BASF, and Dow are actively expanding their product portfolios through R&D investments and strategic partnerships to capitalize on this growing demand.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/296799/global-dry-mix-mortar-additives-forecast-market

Market Overview & Regional Analysis

Asia-Pacific stands as the dominant region in the global dry mix mortar additives market, underpinned by its massive and continuously expanding construction sector. China alone represents the single largest national market for these additives, with enormous infrastructure spending allocations sustaining demand for waterproofing agents, bonding compounds, and cellulose ether-based formulations. India and Southeast Asian nations are experiencing rapid urbanization that is fundamentally reshaping construction material requirements, with contractors increasingly turning to performance-enhancing additives to meet rising quality standards in both residential and commercial segments.

The region's extraordinarily diverse climatic conditions - ranging from sub-zero temperatures in northern China to tropical humidity across Southeast Asia - drive demand for versatile additive formulations capable of performing reliably across a broad range of environmental settings. Redispersible polymer powders are gaining considerable traction in premium construction applications, while cellulose ether remains the most widely consumed additive category due to its cost-effectiveness and broad functionality. Local manufacturers compete aggressively on price, while multinational players such as BASF and Sika differentiate through technical innovation and application support. Green building initiatives are gradually elevating quality expectations, pushing the regional market toward more sophisticated and sustainable additive solutions.

China's construction industry remains the primary engine of regional additive consumption. Massive government-backed infrastructure programs continue to generate sustained demand for high-performance mortar additives, particularly in waterproofing and tile adhesive applications. The presence of established local producers keeps pricing competitive, while multinational firms compete by offering technically superior and application-specific formulations that command premium positioning in urban development projects.

India and Southeast Asian economies are urbanizing at an accelerating pace, creating strong and sustained demand for mortar additives suited to large-scale residential and commercial construction. Prefabricated building methods are gaining adoption, requiring rapid-setting and high-workability additive formulations. Rising awareness of green building certifications is gradually improving the quality threshold expected from mortar additives across this subregion.

The Asia-Pacific additive market features intense competition between cost-focused local manufacturers and technically differentiated multinational suppliers. Companies such as Jinan Maissen New Material and Shandong Xindadi Industrial have built significant regional positions by offering competitively priced cellulose ether and polymer powder products. Meanwhile, global players invest in application laboratories and technical training programs to retain premium market segments in higher-specification construction projects.

Environmental awareness is beginning to shape purchasing decisions across the region, with green building standards gaining influence in commercial construction procurement. Manufacturers are responding by developing bio-compatible and lower-emission additive formulations tailored to regional climate requirements. The push toward reduced water consumption in mortar applications is particularly relevant in water-stressed areas of South and Southeast Asia, opening new opportunities for advanced water-retention additives.

North America represents a mature but innovation-driven market for dry mix mortar additives, characterized by stringent building codes and a strong emphasis on sustainable construction practices. The United States is the dominant national market, where significant federal infrastructure investment is sustaining robust demand for high-performance mortar systems in transportation, commercial, and residential applications. Manufacturers such as DOW Chemical and Ashland have established strong local production and distribution capabilities, enabling them to deliver low-emission and technically advanced additive formulations that meet evolving Environmental Protection Agency requirements. The commercial construction segment leads in additive adoption, though residential prefabrication trends are gradually expanding demand in that segment as well. Premium performance expectations in the region support higher price points for specialized additives, and continued R&D investment by domestic manufacturers is fueling the development of next-generation polymer-modified mortar solutions suited to North America's varied climatic conditions.

Europe occupies a prominent position in the dry mix mortar additives market, particularly in terms of technological advancement and regulatory sophistication. Germany and France collectively account for the largest share of regional consumption, supported by well-established construction industries and high standards for building material performance. The European Union's regulatory agenda - including the Circular Economy Action Plan and ambitious building renovation targets - is actively stimulating demand for bio-based and low-VOC additive formulations. Leading regional manufacturers such as BASF, Wacker Chemie, and Evonik Industries are investing substantially in reformulating their product ranges to align with REACH compliance requirements. The renovation and retrofitting segment presents a particularly important growth avenue, as aging building stock across Western Europe requires advanced mortar solutions for energy-efficient upgrades. However, elevated raw material and energy costs continue to present margin pressures for additive producers operating in this region.

South America presents a moderately growing market for dry mix mortar additives, with Brazil and Argentina serving as the principal consumption centers. Construction activity remains concentrated in urban areas, where basic mortar additives for residential applications represent the dominant demand category. While the region relies significantly on imported advanced formulations, local production of cellulose-based additives is gradually expanding to reduce this dependency. Economic volatility and currency fluctuations in key markets create pricing challenges that push contractors toward value-oriented additive solutions rather than premium offerings. Nevertheless, growing awareness of sustainable building certifications in commercial construction is beginning to elevate interest in higher-performance additive categories. Trade frameworks within MERCOSUR facilitate regional product distribution, though inconsistent testing and certification standards across countries continue to complicate market entry for international suppliers seeking to expand their presence in the region.

The Middle East and Africa region displays notably divergent market characteristics between its two constituent subregions. Gulf Cooperation Council countries, led by the UAE and Saudi Arabia, are adopting premium dry mix mortar additives at a substantial scale, driven by landmark infrastructure and urban development programs. Redispersible polymer powders and high-performance tile adhesive additives are particularly favored in these high-specification projects. In contrast, African markets are largely constrained to basic cellulose ether products due to cost sensitivity, although rapid urbanization rates are gradually encouraging quality upgrades in construction materials. Extreme climatic conditions prevalent across both subregions - intense heat, aridity, and in some areas high humidity - create a specific technical requirement for additives with exceptional water resistance and thermal stability. Joint ventures between regional investors and international additive manufacturers are beginning to strengthen local production capacity, though political instability in parts of Africa continues to create uncertainty for long-term market investment.

Key Market Drivers and Opportunities

The global construction sector's expansion, particularly in emerging economies, fuels demand for dry mix mortar additives. These additives enhance mortar properties like workability, adhesion, and water retention, making them essential for tile adhesives, renders, and plasters. With urbanization rates accelerating-over 55% of the world's population now lives in urban areas-this trend drives consistent market growth.

Builders increasingly adopt advanced additives such as cellulose ethers and redispersible polymer powders to meet stringent performance standards in modern construction. Furthermore, the push for eco-friendly formulations aligns with green building certifications, boosting additive usage by improving durability and reducing material waste. This evolution supports a market projected to grow at a 6.2% CAGR through the decade.

Key additives like hydroxypropyl methylcellulose (HPMC) improve sag resistance and open time, critical for vertical applications in high-rise projects. While regulatory pressures encourage innovation, the integration of multifunctional additives streamlines production processes, further propelling adoption across residential and commercial segments.

Government-led initiatives, including China's Belt and Road and India's Smart Cities Mission, create vast demand for durable mortars in roads, bridges, and housing. Additives tailored for these projects can capture a 7-8% annual growth slice.

The rise of prefabricated construction and 3D printing accelerates need for flowable, high-strength additives. Starch ethers and silicone-based modifiers excel here, offering precise control over rheology.

Sustainability trends open doors for bio-degradable and low-carbon additives, aligning with net-zero goals. Partnerships with construction firms for customized solutions will drive premium segment growth, especially in Europe and North America.

Challenges & Restraints

Fluctuations in petrochemical and cellulose-based raw materials create supply chain disruptions, impacting production costs for dry mix mortar additives. Manufacturers face margins squeezed by up to 15-20% during peak volatility periods, complicating long-term pricing strategies. However, hedging mechanisms offer partial mitigation in mature markets.

The market hosts numerous players, from global giants to regional suppliers, leading to price wars and quality inconsistencies. This fragmentation hinders standardization, while smaller firms struggle with R&D investments needed for next-gen additives like bio-based polymers. Additionally, skilled labor shortages in construction slow the uptake of advanced mortar systems, as improper mixing reduces additive efficacy. While training programs help, regional disparities persist.

Elevated costs associated with premium additives, such as polymer powders, deter widespread use in cost-sensitive developing regions. These materials can increase mortar prices by 10-25%, limiting appeal in low-margin projects. Consequently, traditional cement-based mixes remain dominant.

Environmental regulations on volatile organic compounds (VOCs) in synthetic additives add compliance burdens, slowing innovation. Recycling challenges for polymer-modified mortars further complicate disposal, raising lifecycle costs for end-users. Moreover, dependency on imported raw materials in non-producing countries exposes the market to geopolitical risks and tariffs, restraining expansion. Short-term fixes like local sourcing emerge, but scaling takes time.

Market Segmentation by Type

● Redispersible Polymer Powder

● Cellulose Ether

● Plasticizers

● Defoamers

● Air Entraining Agents

● Others

Redispersible Polymer Powder commands the leading position within this segment owing to its exceptional binding properties, superior flexibility, and broad compatibility across mortar formulations. This additive type significantly improves adhesion strength and crack resistance in finished mortar applications, making it indispensable in tile adhesives, exterior insulation systems, and self-leveling compounds. Cellulose ether follows as a widely adopted additive valued for its ability to enhance water retention, extend open time, and improve workability without compromising structural integrity. Plasticizers are gaining traction as formulators seek to reduce water-to-cement ratios while maintaining pumpability and flow characteristics in complex mortar blends. Air entraining agents serve a critical role in climates where freeze-thaw cycles pose durability challenges, while defoamers are essential in ensuring surface quality and consistency in machine-applied mortars. Emerging additive categories, including nano-modified and bio-based compounds, are gradually entering the market as manufacturers respond to evolving performance demands and environmental standards.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/296799/global-dry-mix-mortar-additives-forecast-market

Market Segmentation by Application

● Tile Adhesives and Grouts

● Plasters and Renders

● Waterproofing Systems

● Self-Leveling Compounds

● Repair Mortars

● Others

Tile Adhesives and Grouts represent the dominant application segment, driven by the widespread adoption of ceramic and porcelain tiles across both residential and commercial construction projects globally. The demand for high-bond, flexible adhesive formulations has intensified as architects and builders increasingly specify large-format tiles that place greater stress on bonding layers. Plasters and renders constitute another significant application area, where additives enhance surface finish quality, reduce shrinkage cracking, and improve resistance to weathering. Waterproofing systems are experiencing accelerating adoption as building codes in flood-prone and water-stressed regions mandate enhanced moisture protection in both below-grade and above-grade structures. Self-leveling compounds are gaining importance in renovation and commercial flooring projects where precision surface preparation is critical. Repair mortars present a growing niche, particularly in aging infrastructure markets where structural rehabilitation demands materials with rapid-setting characteristics and strong substrate compatibility. Collectively, these applications underscore the versatility and functional breadth of dry mix mortar additives across the construction value chain.

Market Segmentation and Key Players

● Sika Group (Switzerland)

● BASF SE (Germany)

● Wacker Chemie AG (Germany)

● Nouryon (Netherlands)

● Dow Inc. (U.S.)

● Evonik Industries (Germany)

● Mapei SpA (Italy)

● Ashland Global (U.S.)

● Jinan Maissen New Material (China)

● Shandong Xindadi Industrial (China)

● RPM International Inc. (U.S.)

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Dry Mix Mortar Additives, covering the period from 2025 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

● Sales, sales volume, and revenue forecasts

● Detailed segmentation by type and application

The report features in-depth competitive intelligence including:

● Market share analysis of leading manufacturers

● Production capacity expansions

● Product portfolio assessments

● Strategic partnership evaluations

Our research methodology combines primary interviews with industry leaders and comprehensive data analysis of:

● Production facilities and their geographical distribution

● Raw material sourcing patterns

● End-user industry consumption trends

● Regulatory impact assessments

Get Full Report Here: https://www.24chemicalresearch.com/reports/296799/global-dry-mix-mortar-additives-forecast-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch