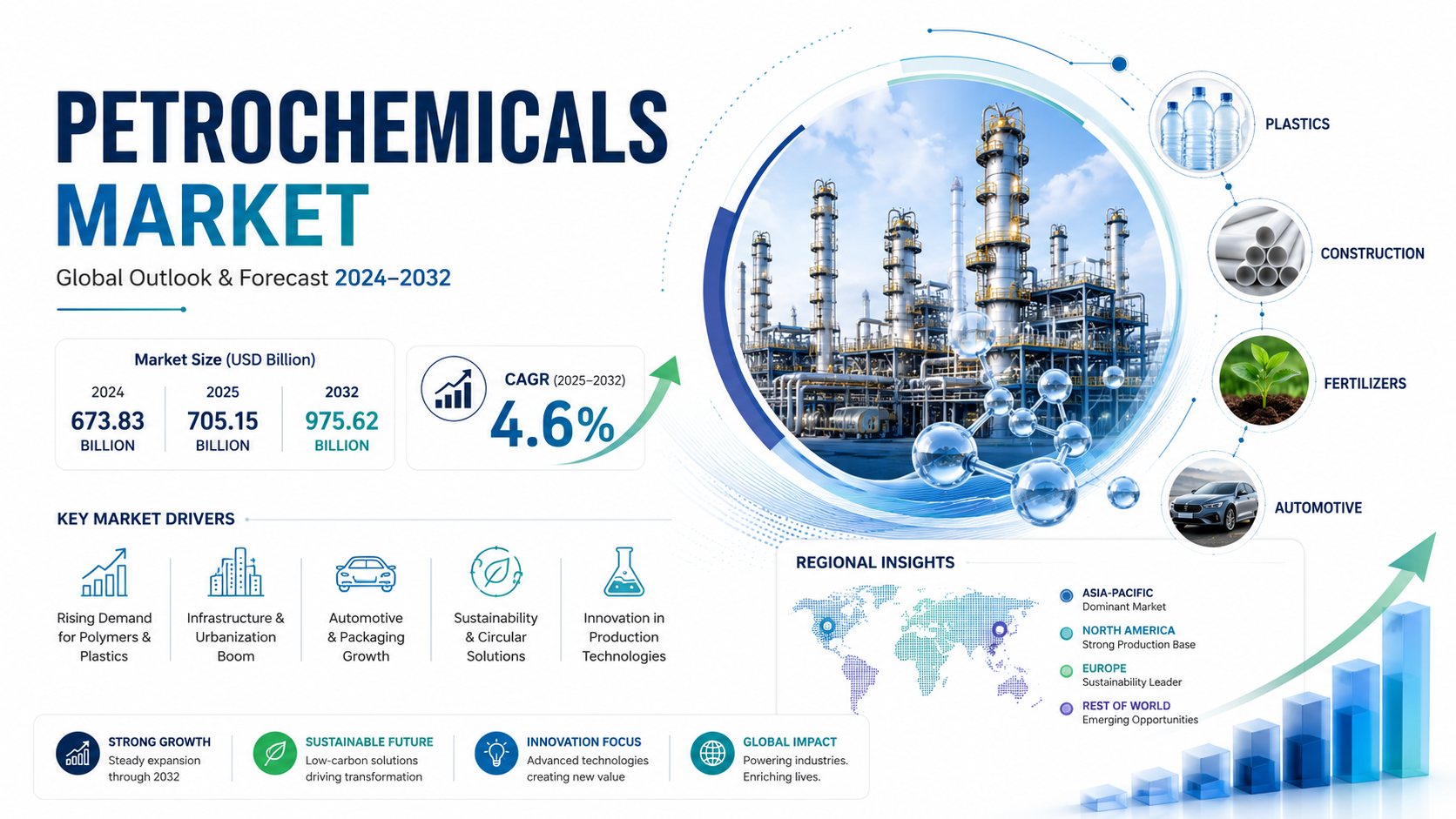

Global Petrochemicals Market to Reach USD 975.62 Billion by 2032, Growing at 4.6% CAGR

The global petrochemicals market size was valued at USD 673.83 billion in 2024. The market is projected to grow from USD 705.15 billion in 2025 to USD 975.62 billion by 2032, exhibiting a CAGR of 4.6% during the forecast period.

Petrochemicals are chemical compounds derived from petroleum and natural gas that serve as foundational materials for countless industrial and consumer products. These include olefins (ethylene, propylene), aromatics (benzene, toluene, xylene), and synthesis gas - essential building blocks for plastics, synthetic rubbers, fertilizers, pharmaceuticals, and adhesives.

The market expansion is driven by robust demand from packaging and construction sectors, where petrochemical-derived plastics and resins remain indispensable. However, environmental concerns about plastic waste and carbon emissions present growing challenges. Major players like BASF, SABIC, and Dow are responding with investments in circular economy solutions and low-carbon production technologies. For instance, in March 2024, LyondellBasell announced a USD 100 million expansion of its advanced polymer recycling capacity to meet sustainability demands while maintaining product performance.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/264557/global-petrochemicals-forecast-market

Market Overview & Regional Analysis

Asia-Pacific stands as the dominant force in the global petrochemicals market, fueled by explosive industrialization, urbanization, and a burgeoning demand for consumer goods and infrastructure development. Countries like China and India lead the charge, with massive investments in manufacturing and construction sectors that heavily rely on petrochemical derivatives such as plastics, synthetic fibers, and fertilizers. The region's strategic position benefits from abundant access to feedstocks like natural gas and coal, alongside government initiatives promoting chemical industry growth. Major applications span across packaging, automotive components, and agricultural enhancements, where olefins and aromatics play pivotal roles. While the area grapples with environmental pressures, its scale ensures it accounts for the largest share of worldwide production and consumption, supporting the overall market's projected expansion from US673.83billionin2024toUS673.83billionin2024toUS 950.07 billion by 2030 at a 4.6% CAGR, with continued momentum toward 2032.

Regulatory framework in China, India, and Southeast Asian nations are increasingly enforcing stricter environmental standards and emission controls, pushing petrochemical producers toward cleaner technologies and compliance measures. These regulations, while adding compliance costs, encourage innovation in sustainable practices, ensuring steady demand for high-efficiency petrochemical processes that align with national sustainability goals and international trade requirements.

China alone drives a substantial portion of the region's output, supported by state-owned giants like Sinopec and extensive downstream industries. This dominance stems from integrated refineries and a vast consumer base, with India following suit through expansions by Reliance Industries, bolstering petrochemical use in everything from textiles to electronics amid rapid economic growth.

Surging urbanization and industrial expansion create robust demand for petrochemical-based materials in construction and automotive sectors. Furthermore, rising food needs amplify fertilizer usage, while advancements in production technologies improve yields and reduce waste. Partnerships between local firms and international players are fostering customized solutions, particularly in high-value derivatives like specialty polymers, propelling long-term market acceleration.

Volatility in crude oil prices and supply chain disruptions from geopolitical tensions pose ongoing hurdles, compounded by a shift toward bio-based alternatives in response to environmental concerns. High capital needs for new facilities also strain smaller players, yet the region's resilient infrastructure and policy support mitigate these issues, maintaining a positive trajectory despite competitive pressures.

North America maintains a strong presence in the petrochemicals landscape, primarily through the United States and Canada, where the shale gas revolution has unlocked low-cost feedstocks, enabling competitive production of ethylene and propylene. Advanced refining infrastructure and innovation hubs drive efficiency, with key players like ExxonMobil and Chevron Phillips investing heavily in capacity expansions to meet domestic and export demands in plastics and fuels. However, the region faces intensifying environmental regulations aimed at reducing carbon footprints, prompting a pivot toward greener technologies such as carbon capture. This balance between resource abundance and sustainability efforts supports steady growth, particularly in high-tech applications like lightweight automotive materials and pharmaceutical intermediates. While economic fluctuations can impact energy prices, the area's technological edge ensures resilience, contributing significantly to global supply chains through exports to Asia and Europe.

Europe's petrochemical market is characterized by a strong emphasis on sustainability and regulatory compliance, with nations like Germany, France, and the Netherlands leading in eco-friendly innovations. The European Union's REACH framework and carbon border adjustment mechanisms enforce rigorous standards, accelerating the transition to circular economy practices and bio-based feedstocks. Major companies such as BASF and TotalEnergies are channeling resources into renewable petrochemicals and recycling initiatives to counter plastic waste concerns. Despite higher production costs compared to other regions, the focus on high-value products like advanced polymers for automotive and construction sustains demand. Challenges from energy price volatility, especially post-geopolitical events, test the sector, but collaborative R&D and policy incentives foster opportunities in green chemistry, positioning Europe as a leader in sustainable petrochemical advancements amid global shifts toward net-zero emissions.

In South America, the petrochemical sector is gaining momentum, anchored by resource-rich countries like Brazil and Mexico, which leverage vast natural gas and oil reserves to fuel domestic production. Expansions in ethylene crackers and derivative plants cater to growing needs in agriculture, where fertilizers derived from synthesis gas are crucial, and in packaging for expanding consumer markets. However, economic instability and infrastructure limitations occasionally disrupt progress, while environmental advocacy pushes for reduced deforestation impacts from upstream activities. Opportunities arise from trade agreements and foreign investments, enabling integration into global value chains. As urbanization accelerates, demand for construction materials and automotive parts rises, though the region must navigate regulatory harmonization to attract more sustainable technologies and enhance competitiveness against larger producers.

The Middle East & Africa region emerges as a petrochemical powerhouse, driven by abundant hydrocarbon reserves in countries such as Saudi Arabia and the UAE, which position it as a major exporter of basic chemicals like aromatics and olefins. State-backed entities like SABIC invest in mega-projects to diversify economies beyond oil, targeting downstream applications in plastics and textiles for both local and international markets. Africa's nascent industry, particularly in South Africa and Nigeria, shows promise through new refineries, but faces hurdles from funding shortages and underdeveloped infrastructure. Environmental regulations are evolving, with a focus on water management and emissions in arid climates. Geopolitical stability and skill development will be key to unlocking growth, as rising urban populations boost demand for affordable housing and consumer goods reliant on petrochemicals.

Key Market Drivers and Opportunities

Expanding polymer demand across industries accelerates petrochemical market growth. The global shift toward lightweight materials in automotive manufacturing and the unrelenting demand for flexible packaging solutions are propelling petrochemical consumption to new heights. In 2024, polymer demand accounted for nearly 60% of total petrochemical output, with polyethylene and polypropylene witnessing 5.2% year-over-year growth. This surge stems from manufacturers replacing traditional materials with high-performance plastics that offer superior durability-to-weight ratios. The electric vehicle revolution further intensifies this trend, as battery components and interior panels increasingly utilize specialized polymer composites that depend on petrochemical feedstocks.

Emerging economies drive infrastructure-led petrochemical consumption. Asia-Pacific's construction boom requires 28 million metric tons of petrochemical-derived materials annually for applications ranging from PVC piping to insulation foams. India's construction sector alone is projected to consume 12% more petrochemical products in 2025 compared to 2024 levels. This growth aligns with governmental initiatives like China's "New Infrastructure" program, which prioritizes 5G networks and smart cities – both reliant on plastic components and synthetic materials. Rapid urbanization across Southeast Asia further compounds this demand, with Vietnam and Indonesia emerging as secondary growth hotspots beyond the traditional Chinese market.

Industrial analysts note that every 1% increase in GDP across developing nations correlates with a 1.8% rise in basic petrochemical consumption. The fertilizer segment demonstrates equally robust dynamics, with ammonia production – heavily dependent on petrochemical feedstocks – growing at 3.7% annually to meet global food security needs. This multilayered demand architecture ensures sustained market expansion through 2032.

Electrification megatrend creates specialty chemical demand surge. The energy transition paradoxically strengthens certain petrochemical segments, particularly lithium battery components requiring ultra-pure solvents and separator films. Battery-grade NMP solvent demand is projected to grow at 22% CAGR through 2032, while PVDF binder production for cathodes will require 280,000 additional tons of fluorochemical capacity. Beyond energy storage, the semiconductor industry's insatiable need for high-purity isopropanol and hydrogen peroxide presents another high-margin avenue, with each new chip fab consuming 15-20% more specialty chemicals than legacy facilities.

Carbon-to-value technologies open new profit pools. First-mover advantage in CO2 utilization is creating differentiated business models, with innovators converting emissions into polycarbonates, polyurethanes, and synthetic fuels. The 2024 launch of commercial-scale CO2-derived polyol plants in Germany and China demonstrates technical feasibility, with lifecycle assessments showing 35-50% lower carbon footprints versus conventional methods. This aligns with corporate net-zero commitments while capturing green premiums – early adopters report 8-12% margin expansion on sustainable product lines. The development of carbon-negative polymerization techniques could further revolutionize the sector's environmental and economic calculus.

Challenges & Restraints

Carbon regulatory frameworks reshape production economics. The petrochemical sector faces mounting pressure as 43 national governments have implemented carbon pricing mechanisms covering 68% of global production capacity. Compliance costs for emissions-intensive steam crackers and reformers could erode 8-12% of EBITDA margins by 2027, particularly in regions with aggressive decarbonization timelines. Facilities in the European Union already grapple with carbon credit prices exceeding €90 per metric ton, compelling operators to either absorb costs or risk becoming globally uncompetitive. The technology gap presents another hurdle – while carbon capture systems for ethylene plants exist, their $120-180 million implementation cost per facility creates significant barriers to adoption.

Supply chain vulnerabilities threaten just-in-time feedstock models. Geopolitical tensions have exposed critical weaknesses in the petrochemical industry's reliance on concentrated feedstock corridors. The 2024 Red Sea shipping disruptions caused naphtha price volatility exceeding 30%, while U.S. Gulf Coast hurricanes repeatedly interrupt 40% of global ethylene glycol supplies. The concentration of 2+ million tons annually in export corridors creates risks that amplify outage impacts. The January 2025 freeze-induced shutdown of a Texas ethylene hub removed 15% of North American capacity for six weeks, illustrating this operational fragility.

Circular economy initiatives disrupt virgin material demand. Legislative mandates for recycled content are reshaping end-market demand patterns, with the EU's Single-Use Plastics Directive requiring 30% recycled PET in bottles by 2030. Advanced mechanical and chemical recycling technologies now compete directly with virgin production, potentially displacing 18 million metric tons of traditional petrochemical demand annually by 2032. Brand owner commitments compound this effect – 76% of FMCG companies have pledged to incorporate 50% recycled content across packaging portfolios within the decade. This structural shift forces petrochemical producers to either integrate recycling operations or risk stranded assets in conventional production lines.

Alternative feedstock development alters competitive landscape. Bio-based pathways are gaining commercial traction, with sugarcane-derived ethylene capacity reaching 3.2 million tons annually across Brazil and Southeast Asia. While currently representing just 4% of global supply, these alternatives command 25-30% price premiums in green-conscious markets. The technology evolution extends beyond biofuels – carbon capture utilization (CCU) projects now demonstrate commercial-scale viability, with the first methanol-from-CO2 facility operational in Iceland since 2023. As these technologies achieve economies of scale, traditional naphtha-based producers face demand erosion in premium market segments.

Market Segmentation by Type

● Olefins (Ethylene, Propylene, Butadiene)

● Aromatics (Benzene, Toluene, Xylenes)

● Synthesis Gas

Olefins dominate the market due to their critical role as building blocks for polymers and plastics.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/264557/global-petrochemicals-forecast-market

Market Segmentation by Application

● Plastics

● Solvents

● Detergents

● Adhesives

● Paints and Coatings

● Rubber

● Fertilizers

● Pharmaceuticals

Plastics lead the applications segment owing to widespread use in packaging and consumer products.

Market Segmentation and Key Players

● ExxonMobil Corporation (U.S.)

● SABIC (Saudi Arabia)

● BASF SE (Germany)

● Reliance Industries Limited (India)

● TotalEnergies SE (France)

● LyondellBasell Industries N.V. (Netherlands)

● Sinopec Group (China)

● Shell plc (Netherlands/UK)

● Chevron Phillips Chemical Company (U.S.)

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Petrochemicals, covering the period from 2024 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

● Sales, sales volume, and revenue forecasts

● Detailed segmentation by type and application

The report features in-depth competitive intelligence including:

● Market share analysis of leading manufacturers

● Production capacity expansions

● Product portfolio assessments

● Strategic partnership evaluations

Our research methodology combines primary interviews with industry leaders and comprehensive data analysis of:

● Production facilities and their geographical distribution

● Raw material sourcing patterns

● End-user industry consumption trends

● Regulatory impact assessments

Get Full Report Here: https://www.24chemicalresearch.com/reports/264557/global-aluminum-plate-sheet-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

分类

閱讀更多

Buy GitHub Accounts From SmartSMMworld: A Complete Guide for Developers, Startups, and Digital Businesses In today’s digital-first world, having a strong online presence is no longer optional. Whether someone is building a software company, launching a new SaaS product, managing open-source projects, or creating automation tools, platforms like GitHub have become an essential part of the...

The deployment of a revenue management facility is a strategic move that requires careful planning to ensure long-term scalability and operational success. When selecting an Anti Plagiarism Software Market solution, organizations must move beyond simple price comparisons and focus on the total cost of ownership (TCO) and operational flexibility. A successful deployment starts with a...

Need high-volume emails that actually land in the inbox? Grab our aged bulk accounts today at unmatched rates. Contact allvirtualsolution now! ♦️ ═════════ 🟢 ONLINE 24/7 ═════════ ♦️ 📥 CONTACT US ANYTIME FOR PREMIUM SERVICES 💎 ◥◣━━━━━━━━━━━━━━━━━━━━━━━━━━━━◢ │ │ 📢 Telegram...

(圖/ 總統府) 賴清德總統昨(6)日上午出席「2026行政院科技顧問會議」開幕式時表示,2026年將是臺灣邁向智慧繁榮的關鍵年。政府除持續鞏固半導體既有優勢,也將全面推進「AI新十大建設」,同步投入矽光子、量子科技與機器人等三大關鍵技術研發,擴充算力基礎建設,期盼讓臺灣不僅是全球知識創新的重要樞紐,更成為AI時代中值得信賴、具高度韌性的領航者。 MGBOX (圖/ 總統府) 賴總統指出,臺灣以科技立國,科技政策攸關國家進步、經濟發展與人民福祉。政府每年持續寬列科技預算,並由行政院院長擔任召集人,召開國家最高層級的科技策略諮詢會議,廣邀專家學者凝聚前瞻共識,為國家科技發展指引方向。他也感謝科技顧問長期提供專業建言,協助政府在快速變動的國際情勢中,作出穩健而關鍵的決策。...