Peptide API Market: Regional Expansion, Competitive Dynamics, and Next-Generation Growth Frontiers (2024–2034)

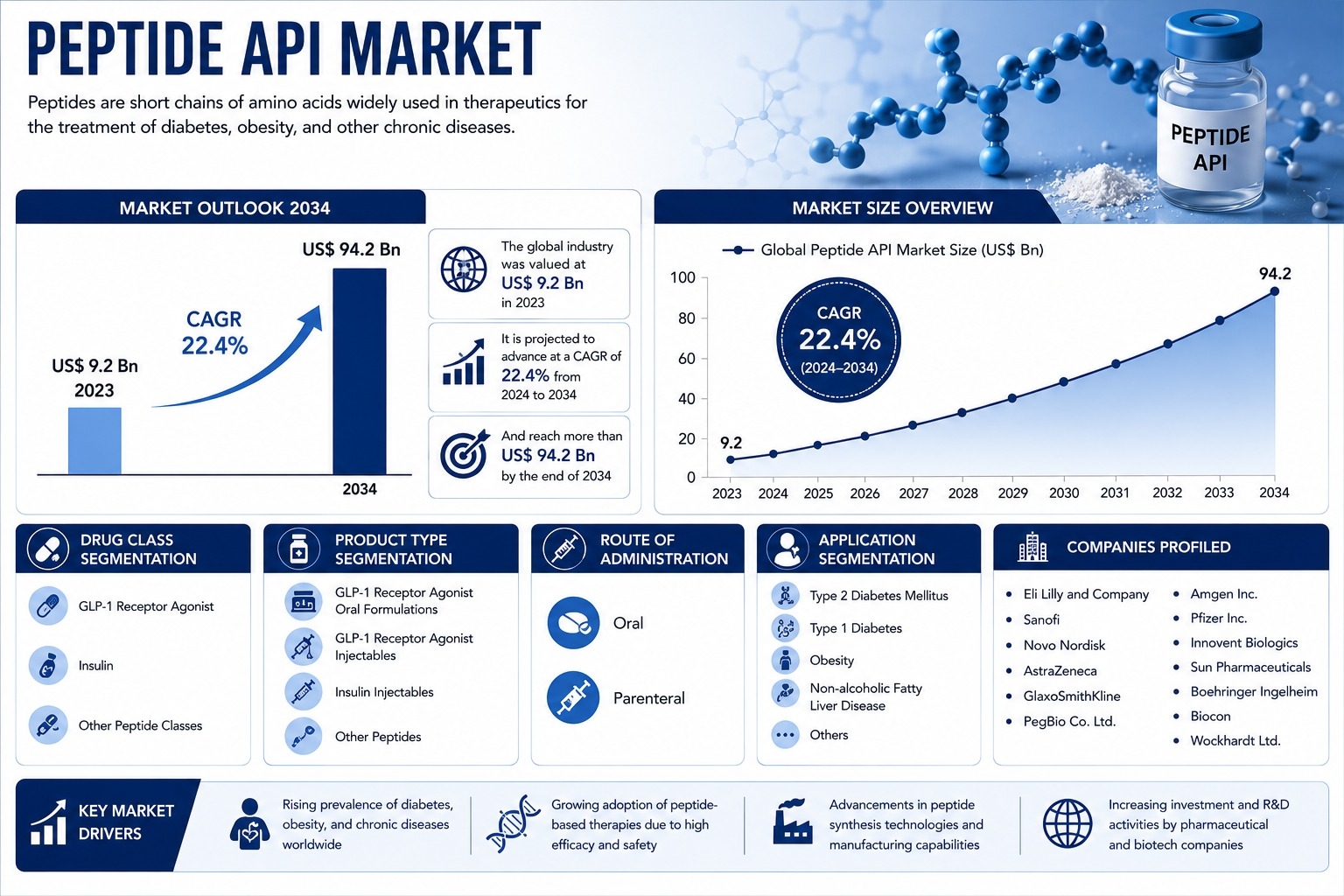

The Peptide Active Pharmaceutical Ingredient (API) market is entering a high-acceleration phase, supported by rising global demand for metabolic disease therapies, strong pharmaceutical innovation pipelines, and rapid advancements in peptide synthesis technologies. Valued at US$ 9.2 billion in 2023, the market is projected to surpass US$ 94.2 billion by 2034, expanding at a robust CAGR of 22.4% from 2024 to 2034.

While earlier growth was largely driven by insulin therapies, the current expansion cycle is fundamentally being reshaped by GLP-1 receptor agonists, obesity therapeutics, and next-generation peptide-based drugs. At the same time, regional manufacturing ecosystems and competitive strategies among global pharmaceutical leaders are playing an increasingly decisive role in defining market direction.

Regional Market Expansion: A Global Growth Story

North America: Established Leader with Strong Innovation Engine

North America continues to dominate the global peptide API market, primarily due to its strong pharmaceutical infrastructure, advanced biotechnology ecosystem, and high healthcare spending.

Key strengths include:

- Concentration of leading pharmaceutical and biotech companies

- Advanced clinical trial infrastructure

- Strong regulatory and intellectual property frameworks

- High prevalence of obesity and diabetes

The United States remains the epicenter of peptide innovation, particularly in GLP-1 receptor agonist development and commercialization. Large-scale investments in manufacturing capacity and R&D pipelines further reinforce the region’s leadership position.

Europe: High-Value Manufacturing and Research Hub

Europe maintains a strong position in peptide API development, particularly in high-quality manufacturing and early-stage drug research.

Key factors supporting growth:

- Strong presence of pharmaceutical giants and biotech firms

- High regulatory standards ensuring product quality

- Well-established contract development and manufacturing organizations (CDMOs)

- Focus on sustainable and advanced biomanufacturing processes

Countries such as Germany, Switzerland, and the UK serve as major hubs for peptide research, while the broader European region continues to expand its footprint in biosimilars and next-generation peptide therapies.

Asia-Pacific: Fastest Growing Regional Market

Asia-Pacific is emerging as the fastest-growing region in the peptide API market, driven by a combination of demographic, economic, and industrial factors.

Key growth drivers:

- Rapid increase in diabetes and obesity prevalence

- Expanding middle-class population with rising healthcare access

- Strong pharmaceutical manufacturing base in India and China

- Increasing adoption of GLP-1 receptor agonists

India, in particular, has become a critical global supplier of pharmaceutical APIs, including peptide-based products, supported by cost advantages and strong chemical synthesis capabilities. China is also rapidly expanding its biotech ecosystem with increasing investment in innovative peptide drugs.

Rest of the World: Emerging Opportunities

Regions such as Latin America, the Middle East, and Africa are still developing their peptide API markets but are expected to grow steadily over the forecast period.

Growth is supported by:

- Gradual improvement in healthcare infrastructure

- Increasing awareness of chronic disease management

- Expanding access to insulin and metabolic therapies

- Entry of multinational pharmaceutical companies

Competitive Landscape: A Highly Innovation-Driven Industry

The peptide API market is highly competitive, characterized by strong participation from multinational pharmaceutical companies, biotechnology innovators, and specialized API manufacturers.

Key Competitive Strategies

1. Large-Scale Capacity Expansion

Companies are aggressively expanding manufacturing facilities to meet surging demand for GLP-1-based therapies. This includes investments in:

- Aseptic filling plants

- Peptide synthesis units

- High-capacity biomanufacturing infrastructure

These expansions are critical to addressing global supply constraints, especially for injectable peptide drugs.

2. Pipeline Diversification Beyond Diabetes

While diabetes and obesity remain core markets, companies are actively expanding into:

- Cardiovascular diseases

- Non-alcoholic fatty liver disease (NAFLD)

- Oncology applications

- Rare metabolic disorders

This diversification reduces dependence on a single therapeutic category and opens new revenue streams.

3. Strategic Collaborations and Partnerships

The complexity of peptide drug development has led to a surge in partnerships between:

- Large pharmaceutical companies

- Biotech startups

- Contract development and manufacturing organizations (CDMOs)

These collaborations accelerate drug discovery, reduce development timelines, and improve commercialization efficiency.

4. Mergers and Acquisitions (M&A) Activity

M&A activity is intensifying as companies seek to:

- Strengthen peptide manufacturing capabilities

- Acquire GLP-1 pipeline assets

- Expand geographic presence

- Gain access to novel peptide technologies

This consolidation trend is expected to continue as competition in the metabolic therapeutics space intensifies.

Leading Companies in the Peptide API Market

The market is dominated by several global pharmaceutical leaders and emerging biotech innovators, including:

- Eli Lilly and Company

- Novo Nordisk

- Sanofi

- Amgen Inc.

- AstraZeneca

- Pfizer Inc.

- Boehringer Ingelheim

- GlaxoSmithKline (GSK)

- Biocon

- Sun Pharmaceutical Industries

- Wockhardt Ltd.

- Innovent Biologics

- PegBio Co. Ltd.

These companies are heavily investing in GLP-1 receptor agonists, next-generation insulin analogs, and dual/triple agonist peptides designed to improve metabolic outcomes.

Key Industry Trends Shaping the Market

1. Shift Toward Long-Acting and Convenient Therapies

There is a strong trend toward:

- Once-weekly or monthly injectables

- Improved patient adherence formulations

- Combination peptide therapies

These innovations improve convenience and long-term treatment success rates.

2. Rise of Oral Peptide Formulations

Historically, peptides were limited to injectables due to poor oral bioavailability. However, new drug delivery technologies are enabling:

- Oral GLP-1 formulations

- Enhanced absorption mechanisms

- Protective delivery systems against enzymatic degradation

This is expected to significantly expand patient adoption.

3. Dual and Multi-Agonist Therapies

Next-generation peptides are being designed to target multiple metabolic pathways simultaneously, such as:

- GLP-1 + GIP receptor agonists

- GLP-1 + glucagon receptor combinations

These therapies show superior weight loss and glycemic control outcomes compared to single-target drugs.

4. Artificial Intelligence in Peptide Drug Design

AI and machine learning are increasingly used to:

- Predict peptide structures

- Optimize synthesis pathways

- Improve binding efficiency

- Accelerate drug discovery timelines

This is significantly reducing R&D costs and development cycles.

Manufacturing Landscape and Supply Chain Evolution

Peptide API manufacturing is becoming more advanced and globally distributed. Key developments include:

- Expansion of high-capacity peptide synthesis facilities

- Increased outsourcing to CDMOs

- Automation of production processes

- Improved purification and quality control systems

Supply chain resilience has become a strategic priority, particularly after global disruptions that exposed vulnerabilities in pharmaceutical manufacturing networks.

Application Landscape: Expanding Beyond Metabolic Diseases

While metabolic disorders dominate current demand, peptide APIs are increasingly being explored for:

- Oncology: Targeted cancer therapies and immune modulation

- Neurology: Neuroprotective peptides for degenerative diseases

- Cardiology: Blood pressure and heart failure treatments

- Endocrinology: Hormonal regulation therapies

- Rare diseases: Specialized orphan drug applications

This diversification significantly expands the long-term market potential.

Future Outlook (2024–2034)

The peptide API market is expected to evolve rapidly over the next decade, shaped by several transformative forces:

- Continued dominance of GLP-1 receptor agonists

- Expansion of obesity treatment as a standalone therapeutic category

- Increased adoption of oral peptide drugs

- Growth of personalized and precision medicine approaches

- Strong investment in global manufacturing capacity

- Emergence of next-generation multi-target peptide therapies

These factors collectively point toward a sustained high-growth trajectory.

Conclusion

The peptide API market is undergoing a global transformation driven by regional expansion, intense competitive innovation, and rapid technological advancements. With GLP-1 therapies leading the charge and new peptide applications emerging across multiple disease areas, the industry is positioned for extraordinary growth through 2034.

分类

閱讀更多

(圖/ 總統府) 總統賴清德19日上午接見「114年全國模範公務人員代表」,肯定獲獎者在各自崗位上以專業與熱忱推動政策、服務人民,並期勉新的一年持續團結合作,以專業守護國家,朝向安全韌性、智慧繁榮、公平永續與民主團結等四大目標邁進,為臺灣的民主、安全與繁榮奠定更穩固的基礎。 (圖/ 總統府) 賴總統致詞時首先代表國家與國人向獲獎者表達祝賀,並感謝其以責任感與使命感投入公共服務,是促進國家進步、社會安定與人民福祉的重要力量。...

✨🍁⭐⚡💫💎📲✨🌍✨🍁⭐⚡💫💎📲✨🌍 ✨🍁⭐⚡💫💎📲✨🌍whatsApp;+1(530)768-9411 ✨🍁⭐⚡💫💎📲✨🌍⇒Telegram:@smmtopit ✨🍁⭐⚡💫💎📲✨🌍website link;https://smmtopit.com/ ✨🍁⭐⚡💫💎📲✨🌍✨🍁⭐⚡💫💎📲✨🌍 https://smmtopit.com/product/buy-old yahoo-accoun https:/smmtopit.com/product/buy-old yahoo-accoun Get Yahoo Accounts In the fast-paced world of digital marketing, having a reliable email strategy is vital for success. With millions of...

The Global Dipropylene Glycol (DPG) market size was valued at US 422 million by 2029, exhibiting a CAGR of -3.7% during the forecast period. The decline reflects market adjustments post-pandemic and geopolitical impacts from the Russia-Ukraine conflict. Dipropylene Glycol is a versatile chemical compound primarily used as a solvent, plasticizer, and...