Video Conference Equipment Market: Growth Factors, Industry Dynamics, and Outlook 2026-2034

The global Video Conference Equipment Market, valued at a robust figure in 2024, is on a trajectory of significant expansion. The market is projected to continue its upward momentum through 2032, driven by the pervasive adoption of hybrid work models, rapid advances in AI‑enabled video technologies, and the increasing demand for secure, high‑definition collaboration tools across enterprise, education, and health‑care sectors.

Video conference equipment, encompassing dedicated hardware such as conference room endpoints, all‑in‑one codecs, intelligent cameras, and integrated audio solutions, is becoming indispensable for organizations seeking to maintain productivity, reduce travel costs, and ensure business continuity. The ease of deployment of cloud‑based platforms combined with the reliability of on‑premise appliances creates a versatile ecosystem that supports a broad range of use cases-from boardroom meetings to large‑scale virtual events.

Download FREE Sample Report:

Video Conference Equipment Market - View in Detailed Research Report

Hybrid Work as the Primary Growth Engine

The acceleration of hybrid work arrangements worldwide is the primary catalyst for market growth. Companies are investing heavily in solutions that enable seamless transition between in‑office and remote participants. According to the competitive landscape analysis, leading providers like Zoom Video Communications and Cisco Systems (WebEx) have expanded their hardware portfolios to complement their software services, creating integrated ecosystems that lock in enterprise customers.

Security and compliance requirements are also reshaping the market. GDPR‑compliant solutions dominate the European segment, while HIPAA‑ready hardware is driving adoption in North American health‑care institutions. The need for end‑to‑end encryption, data residency controls, and flexible authentication mechanisms is prompting vendors to embed advanced security features directly into their devices.

Emerging AI capabilities are further differentiating product offerings. AI‑powered noise cancellation, automatic framing, real‑time language translation, and meeting analytics are now standard expectations for premium equipment. These intelligent functions not only enhance user experience but also provide actionable insights that improve meeting efficiency and organizational productivity.

Competitive Landscape

COMPETITIVE LANDSCAPE

Key Industry Players

Video Conference Equipment Market Dominated by Hybrid Solutions and Cloud Platforms

The video conference equipment market is dominated by established players like Zoom Video Communications and Cisco (WebEx), which control significant market share through integrated hardware‑software ecosystems. Poly (formerly Polycom) remains a leader in professional‑grade conference room systems, while Microsoft Teams has rapidly gained traction through Office 365 integration. The market structure shows clear segmentation between high‑end enterprise solutions (Cisco, Poly) and mass‑market cloud platforms (Zoom, GoToMeeting).

Niche players like Sony specialize in premium AV equipment for boardrooms, while regional champions like Huawei and Tencent Meeting dominate Asian markets. Emerging competitors like Owl Labs are disrupting traditional setups with AI‑powered 360° cameras. The rise of hybrid work has enabled newer entrants like Whereby and Around to gain traction with browser‑based solutions requiring minimal hardware.

List of Key Video Conference Equipment Companies Profiled

-

Poly (Polycom)

-

Microsoft (Teams)

-

Huawei

-

Logitech

-

Tencent Meeting

-

Alibaba (DingTalk)

-

Owl Labs

-

Around

-

BlueJeans (Verizon)

-

Pexip

Segment Analysis

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Cloud-based solutions dominate as enterprises prioritize flexibility and scalability.

|

| By Application |

|

Corporate Enterprises remain the primary adopters with evolving needs:

|

| By End User |

|

SMEs show accelerated adoption due to:

|

| By Technology |

|

AI‑powered Solutions drive innovation:

|

| By Deployment |

|

Integrated Suites gain preference:

|

Regional Analysis

Regional Analysis: Video Conference Equipment Market

Large corporations account for the majority of video conference equipment purchases, investing heavily in integrated room systems and executive‑grade solutions. Financial services and tech firms lead adoption with dedicated video conferencing budgets.

Telemedicine adoption has accelerated demand for HIPAA‑compliant video conference systems. Hospitals deploy specialized equipment for remote consultations, combining medical imaging with conferencing capabilities.

Universities and K‑12 districts invest in classroom video systems supporting hybrid learning. Smartboards with integrated cameras and microphones are becoming standard in academic institutions.

Federal and state agencies prioritize secure video conferencing solutions for interdepartmental communications. Requirements include end‑to‑end encryption and compatibility with existing security protocols.

Europe

Europe demonstrates robust growth in video conference equipment adoption, driven by multinational corporations and public sector modernization. GDPR‑compliant solutions gain traction, with Germany and the UK leading in enterprise deployments. The region sees increasing demand for all‑in‑one systems that combine hardware and software with data‑protection features. Hybrid work policies across EU countries sustain steady equipment purchases.

Asia‑Pacific

APAC emerges as the fastest‑growing market, fueled by digital transformation in India and China. Small and medium enterprises increasingly adopt cost‑effective video conference solutions. Government initiatives for smart cities integrate advanced conferencing infrastructure. Japan and South Korea focus on high‑end equipment with AI features.

South America

Brazil and Mexico show growing interest in video conference equipment among financial and educational institutions. Price sensitivity drives demand for mid‑range solutions, while multinational subsidiaries invest in premium systems. Infrastructure limitations in remote areas present both challenges and opportunities.

Middle East & Africa

GCC countries lead regional adoption through smart government initiatives and corporate expansions. Dubai and Abu Dhabi require advanced video conferencing in business hubs. African growth is concentrated in South Africa and Kenya, focusing on cloud‑based solutions for mobile workforce connectivity.

Get Full Report Here:

Video Conference Equipment Market, Trends, Business Strategies 2025-2032 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

Click Here to Explore More Insightful Result

https://semiconductorinsight.com/blog/tag/sensors-for-cold-chain-monitoring-market-price/

https://semiconductorinsight.com/blog/tag/sensors-for-cold-chain-monitoring-market-size/

https://semiconductorinsight.com/blog/tag/photomasks-in-semiconductor-market-size/

https://semiconductorinsight.com/blog/tag/miniature-current-transformer-market-share/

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us

閱讀更多

(圖/ 截自YouTube陽明山國家公園管理處INFO) 陽明山國家公園擎天崗近日爆出一起罕見的即時影像爭議事件,一對男女於草原涼亭及木椅區停留期間,疑似出現不雅親密行為,過程被官方設置的24小時監控攝影機錄下,並透過YouTube即時影像系統外流,引發網路大量討論與輿論熱議。 該即時影像原屬於陽明山國家公園管理處用於觀光資訊與環境監測之公開直播系統,但因夜間畫面雖昏暗仍持續運作,加上同步收音,使得相關行為被完整記錄並在網路端擴散,形成罕見的「直播事故」事件。管理單位在發現後,已緊急將該路段影像調整為不公開,以避免內容持續流傳。...

Introduction Entering the Indian market offers vast opportunities for foreign manufacturers, but it also comes with strict regulatory requirements. One of the most important compliances is obtaining certification under the Foreign Manufacturers Certification Scheme (FMCS). This is where a BIS FMCS Consultant becomes essential. In this blog, we will explore the role of a BIS FMCS Consultant, the...

Buy Verified GitHub Accounts from GetPvaZone.com – Trusted Source for Developers and Businesses📢🌐📊📈💰📢We are available online 24/7.📢🌐📊📈💰📢Telegram:getpvazone.com📢🌐📊📈💰📢Whatsapp:+1(219) 396-6971📢🌐📊📈💰📢Email:getpvazon@gmail.com IntroductionGitHub is the world’s leading platform for developers, programmers, and organizations to collaborate on code, manage repositories, and build...

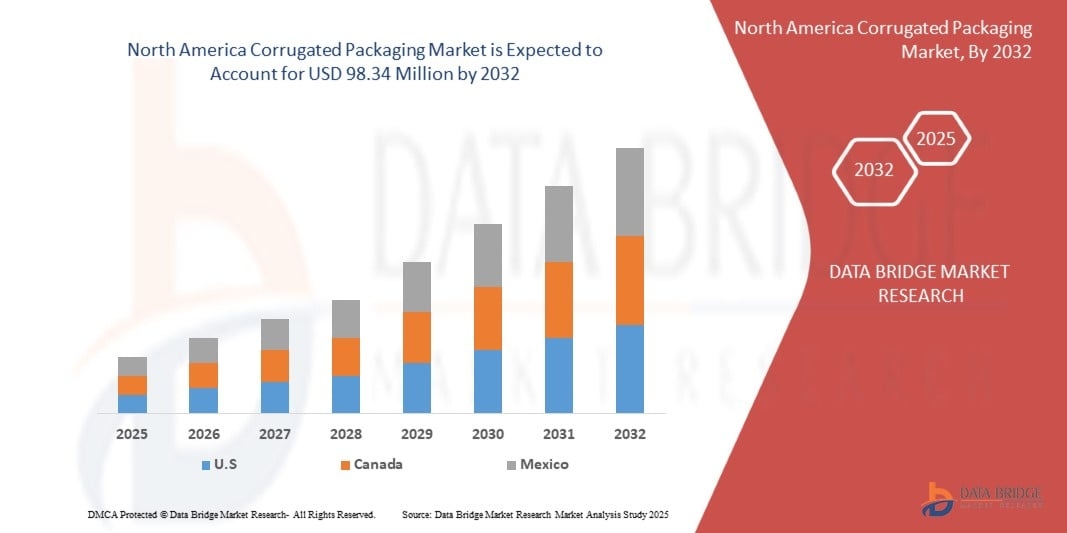

According to the latest report published by Data Bridge Market Research, the North America Corrugated Packaging Market The North America corrugated packaging market was valued at USD 66.68 million in 2024 and is expected to reach USD 98.34 million by 2032. During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 5.1%, primarily...