Examining The Global Competitive Landscape And Trends Within Continuous Delivery Market Share

The competitive distribution of market share in the global deployment sector is currently a battleground between massive, multi-national infrastructure firms and specialized, highly focused platform providers. A thorough examination of the Continuous Delivery Market share reveals that while generalist IT services initially captured significant usage, the tide is turning toward dedicated delivery platforms that offer integrated security and compliance tools. This shift is happening because corporations are realizing that generic integration services lack the specific functionality required for effective software release—such as specialized data cleansing libraries, industry-specific compliance templates, and integrated project management dashboards. Consequently, market share is increasingly concentrating among players who offer a holistic, end-to-end deployment experience rather than just a staffing service.

Geographically, the market share is heavily concentrated in regions with high digital literacy and a strong emphasis on professional services efficiency, such as North America and Europe. In these regions, the culture of "billable velocity" and digital compliance is deeply ingrained, providing a stable and lucrative foundation for software providers and their integration partners. However, emerging markets in Latin America and Asia-Pacific are showing the fastest growth rates. As digital infrastructure improves in these areas, the competitive landscape is shifting to accommodate the unique needs of these regions, such as localized tax support and multi-language interfaces. Providers that capture the "first-mover" advantage in these high-growth regions are likely to see their market share expand significantly as these economies modernize their corporate IT sectors.

The influence of "ecosystem stickiness" cannot be overstated when analyzing market share. Many of the leading platforms are now integrating with cloud-based business technology platforms and specialized industry clouds. By becoming the "default" choice for a company's ERP strategy, these providers create a significant barrier to exit for their clients. The cost of switching platforms, in terms of both data migration and retraining staff on new security workflows, is high, effectively locking in market share for the top-tier providers. This dynamic favors larger companies with the resources to pursue deep integrations and strategic partnerships, making it increasingly difficult for new, smaller players to gain a foothold without a truly disruptive innovation.

Finally, the future of market share will likely be dictated by the ability to cater to the "global enterprise" demographic. As the economy shifts toward truly distributed, multi-national operations, the demand for delivery software is moving beyond local offices into global corporate headquarters. Software platforms that can pivot to address these global needs—offering features like multi-region deployment, global corporate governance dashboards, and synchronized release scheduling—will capture a new and highly valuable segment of the market. The providers that successfully bridge the gap between regional compliance and global corporate governance will be the leaders in the next phase of market share distribution.

Top Trending Reports:

Mobile Business Process Management Bpm Market

Mobile Campaign Management Platform Market

閱讀更多

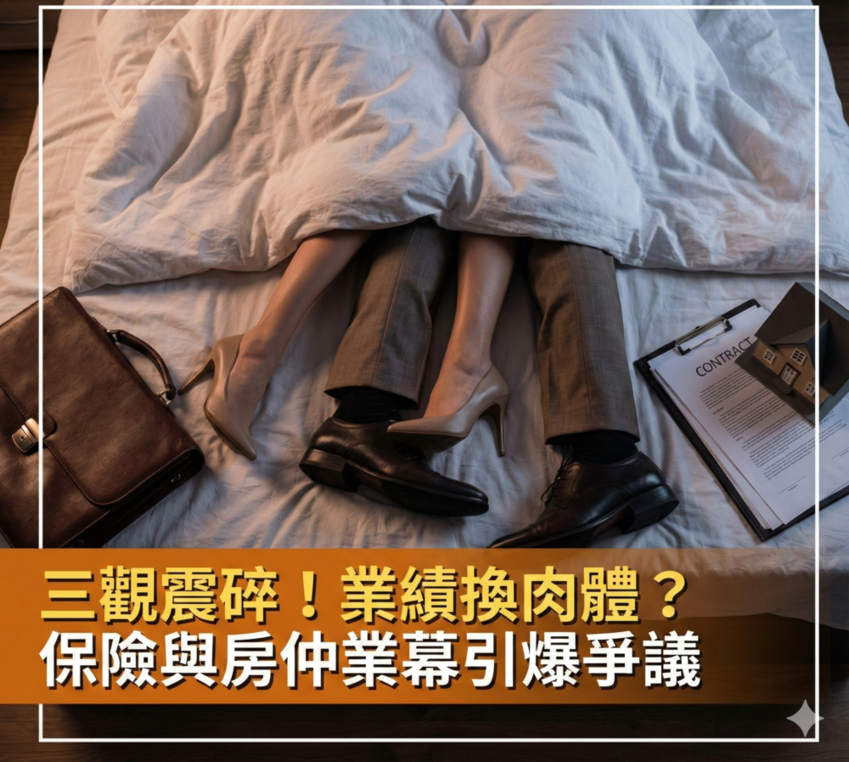

(圖/ AI生成示意圖) 保險與房地產仲介長期被視為高度業績導向的銷售產業,雖然入行門檻相對明確,但競爭激烈與高淘汰率的生態,也讓職場文化與倫理界線屢屢成為社會關注焦點。近日,一名曾短暫投入保險業的女性在網路論壇發文爆料,揭露業界內部可能存在的灰色生態,相關內容迅速引發網路熱議。 她直指,在業績掛帥的高壓環境下,部門裡流傳不少「不能見光的成交祕辛」。除了削價退傭、同業之間搶單競爭外,甚至傳出部分主管或資深業務為了衝刺成交,不惜涉及不當性行為,以曖昧甚至肉體關係換取業績成果。相關耳語多在私下流傳,也讓她形容「三觀幾乎被打碎」,開始質疑自己踏入的究竟是專業服務產業,還是殘酷的業績戰場。 MGBOX (圖/ AI生成示意圖)...

(圖/ 經濟部商業發展署) 經濟部商業發展署「2026集品生活 遊.食.購」展22日起在臺北車站正式開展,集結全臺商圈、市場、夜市、美食與生活品牌,透過大型城市生活市集形式,吸引民眾在假日期間走進臺北車站感受臺灣在地特色消費文化。 (圖/ 經濟部商業發展署) 經濟部商業發展署表示,商業服務業長期扮演臺灣內需市場的重要支柱,此次活動以「遊、食、購」為核心概念,規劃「悠遊生活」、「美食生活」與「質感生活」三大展區,希望透過實體展售與互動體驗,帶動消費市場熱度,同時展現各地特色商業品牌的創新能量。 (圖/ 經濟部商業發展署)...