Monomethylsilane (MMS) Market Size, Share & Forecast 2034

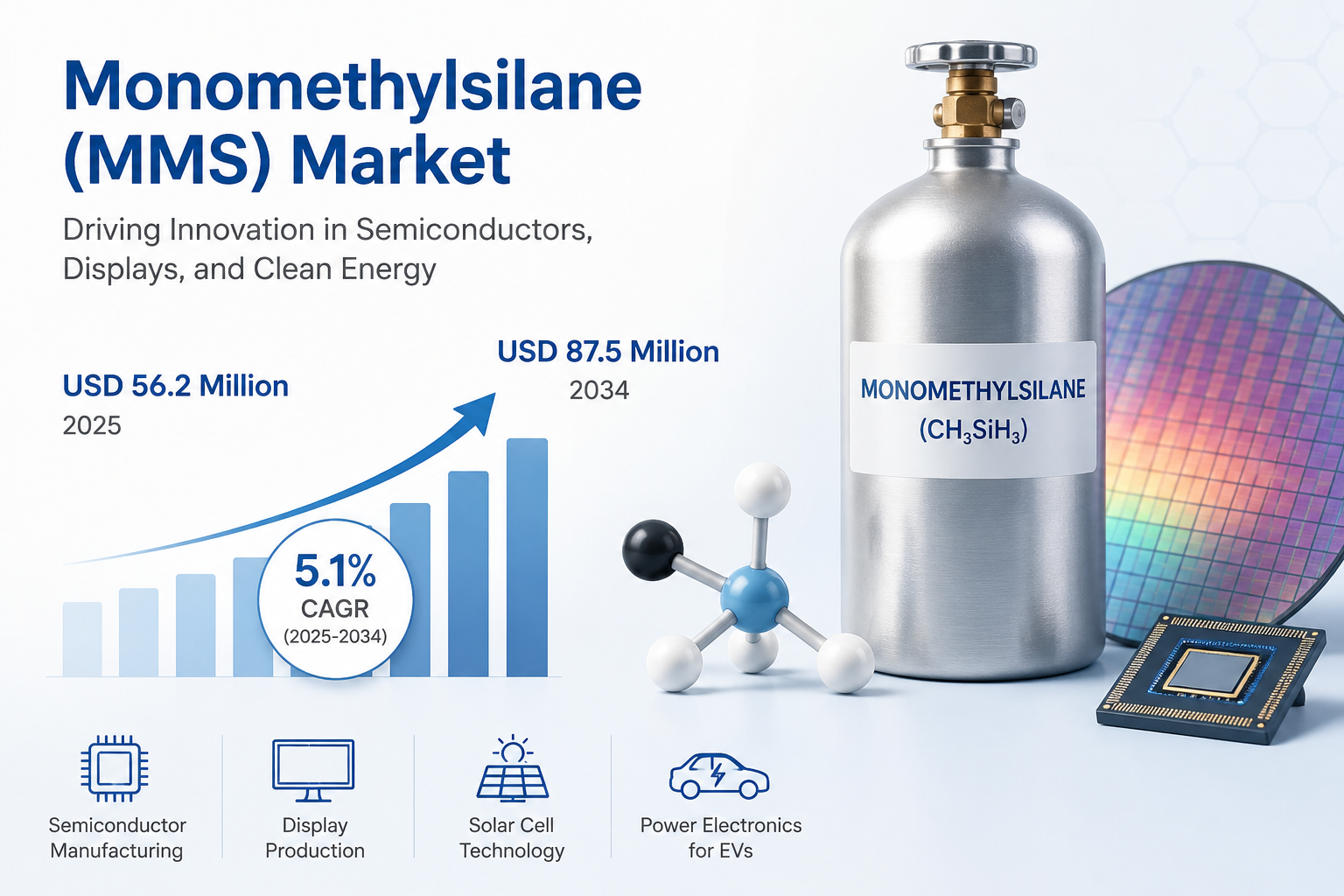

Global Monomethylsilane (MMS) market was valued at USD 56.2 million in 2025 and is projected to reach USD 87.5 million by 2034, exhibiting a compound annual growth rate (CAGR) of 5.1% during the forecast period. Market sales volume is anticipated to grow from an estimated 125 tons in 2025 to approximately 195 tons by 2034.

Monomethylsilane (CH3SiH3) is a highly specialized organosilicon compound that serves as a critical precursor in advanced material synthesis. Its unique molecular structure provides exceptional reactivity, making it indispensable for depositing high-purity silicon-containing films through chemical vapor deposition processes. The compound's pyrophoric nature requires sophisticated handling protocols, yet its value proposition in enabling next-generation semiconductor technologies continues to drive market adoption across multiple high-tech industries.

Get Full Report Here: https://www.24chemicalresearch.com/reports/304638/monomethylsilane-market

Market Dynamics:

The market's evolution demonstrates a fascinating interplay between technological advancement and practical implementation challenges. While demand grows steadily from core electronics applications, the industry must navigate complex safety requirements and evolving regulatory landscapes that shape commercial opportunities.

Powerful Market Drivers Propelling Expansion

-

Semiconductor Industry Evolution: The transformation toward wide-bandgap semiconductors represents the most significant growth vector for MMS adoption. Silicon carbide (SiC) and gallium nitride (GaN) technologies, which deliver superior performance in high-power and high-frequency applications, rely heavily on high-purity MMS for epitaxial growth processes. The global semiconductor industry's relentless pursuit of efficiency gains, particularly in electric vehicle power systems and 5G infrastructure, creates sustained demand for these advanced materials. Major semiconductor foundries have increased their SiC production capacity by 40-50% annually since 2022, directly correlating with MMS consumption growth.

-

Advanced Display Technologies: Flat-panel display manufacturers increasingly utilize MMS in the production of thin-film transistors and encapsulation layers. The transition to higher resolution displays and flexible form factors requires materials that can deliver superior electronic properties and environmental stability. MMS-enabled deposition processes allow for lower temperature processing compared to alternative precursors, making it particularly valuable for next-generation OLED and microLED displays where thermal budget constraints are critical.

-

Solar Energy Expansion: Photovoltaic manufacturers continue to adopt MMS for amorphous silicon layers in advanced solar cell architectures. The global push toward renewable energy infrastructure, with solar capacity installations growing at 15-20% annually, creates substantial opportunities for MMS suppliers. Recent advancements in tandem cell designs and perovskite-silicon hybrid structures further enhance the value proposition of high-purity silicon precursors like MMS.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/304638/monomethylsilane-market

Significant Market Restraints Challenging Adoption

Despite its technological advantages, the market faces substantial barriers that limit more widespread implementation across potential application areas.

-

Handling and Safety Requirements: The pyrophoric nature of MMS necessitates specialized infrastructure throughout the supply chain. Implementation of safety systems, including inert atmosphere handling equipment and explosion-proof facilities, increases capital expenditure by 25-35% compared to conventional chemical operations. Furthermore, transportation regulations for pyrophoric materials limit logistical options and increase costs by approximately 15-20% compared to non-hazardous alternatives.

-

Regulatory Compliance Burden: Stringent regulations governing hazardous chemical handling create significant administrative overhead. Compliance with standards such as REACH in Europe and TSCA in the United States requires extensive documentation and testing protocols. The approval process for new manufacturing facilities typically spans 18-24 months, delaying capacity expansion and increasing project costs by 20-25% through extended engineering and compliance verification phases.

Critical Market Challenges Requiring Innovation

The transition from laboratory-scale application to industrial implementation presents multifaceted challenges that impact both producers and end-users.

Production consistency remains a persistent issue, with batch-to-batch variation affecting approximately 10-15% of production output. Maintaining purity levels above 99.9% requires sophisticated purification systems that account for 30-40% of total production costs. The development of advanced analytical techniques for quality verification adds another layer of complexity, requiring investments in specialized instrumentation and trained personnel.

Supply chain vulnerabilities represent another significant challenge. Dependence on limited silicon metal sources and specialized processing equipment creates potential bottlenecks. Transportation restrictions limit inventory flexibility, forcing just-in-time delivery models that increase operational complexity. These factors collectively contribute to price volatility, with periodic supply constraints causing price fluctuations of 15-25% during market tightness.

Vast Market Opportunities on the Horizon

-

Electric Vehicle Revolution: The automotive industry's transition to electrification creates unprecedented opportunities for MMS applications. Silicon carbide power electronics, essential for efficient traction inverters and onboard chargers, could consume 40-50% of global MMS production by 2030. Partnerships between chemical suppliers and automotive OEMs are accelerating technology adoption, with several major manufacturers announcing dedicated SiC production facilities.

-

Emerging Applications in Quantum Technologies: Research institutions and technology companies are exploring MMS for quantum computing and sensing applications. The compound's ability to create ultra-pure silicon layers makes it attractive for qubit formation and quantum device fabrication. While still in early stages, this segment represents a potential high-value market with applications ranging from computing to medical imaging.

-

Advanced Packaging Solutions: The semiconductor industry's shift toward 3D packaging and heterogeneous integration creates new opportunities for MMS in deposition applications. As traditional scaling approaches reach physical limits, new packaging technologies require advanced materials that can deliver superior thermal and electrical performance in increasingly constrained form factors.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into three purity grades: 95-97%, 97-99%, and >99% purity. The >99% purity segment dominates market value, representing approximately 65% of revenue despite comprising only 40% of volume. This segment's growth is driven by stringent semiconductor industry requirements where even minute impurities can significantly impact device performance and yield rates.

By Application:

Application segments include Semiconductor Manufacturing, Display Production, Solar Cells, and Research & Development. The Semiconductor Manufacturing segment accounts for the largest share, driven by continuous innovation in device architectures and materials requirements. The Display Production segment shows strong growth potential as manufacturers adopt new technologies requiring superior barrier properties and electronic characteristics.

By End-User Industry:

The end-user landscape includes Electronics, Automotive, Energy, and Research Institutions. The Electronics industry remains the dominant consumer, leveraging MCS for advanced device fabrication. The Automotive sector demonstrates the fastest growth rate as electric vehicle adoption accelerates, driving demand for power electronics components that utilize silicon carbide technology.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/304638/monomethylsilane-market

Competitive Landscape:

The global Monomethylsilane market features a concentrated competitive environment with several established players dominating production capabilities. The market structure combines large chemical corporations with specialized producers focusing on high-purity segments. Innovation strategies emphasize purity improvement, safety enhancements, and application development partnerships with key end-users.

List of Key Monomethylsilane Companies Profiled:

-

Gelest Inc. (USA)

-

Linde plc (Ireland)

-

Evonik Industries (Germany)

-

Shin-Etsu Chemical (Japan)

-

Air Liquide (France)

-

Merk KGaA (Germany)

-

Albemarle Corporation (USA)

-

Wacker Chemie AG (Germany)

-

Versum Materials (USA)

-

SAFC Hitech (USA)

-

Anderson Europe (Belgium)

-

Voltaix (USA)

Competition primarily focuses on technological capability, supply reliability, and customer support services. Leading players invest significantly in research and development, with top companies allocating 8-12% of revenue to innovation programs. Strategic partnerships with semiconductor manufacturers and research institutions represent another key competitive strategy, enabling co-development of application-specific solutions.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Dominates the global market with approximately 60% share, driven by concentrated semiconductor and electronics manufacturing in China, Taiwan, South Korea, and Japan. The region benefits from established supply chains, government support for high-tech industries, and continuous capacity expansion in semiconductor fabrication facilities.

-

North America: Holds a 25% market share characterized by strong technology development and specialized manufacturing. The United States leads in research and development activities, particularly in advanced semiconductor technologies and emerging applications. The region's well-developed electronics ecosystem and presence of major technology companies support sustained demand.

-

Europe: Accounts for approximately 12% of global demand, with strength in specialty chemicals and research applications. Germany, France, and the United Kingdom host several key players and research institutions focusing on advanced materials development. The region's strong automotive industry provides growth opportunities through electric vehicle adoption.

Get Full Report Here: https://www.24chemicalresearch.com/reports/304638/monomethylsilane-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/304638/monomethylsilane-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/