Strain Gage Based Sensor Market to Grow at 5.9% CAGR Through 2032 Driven by Automation and IoT

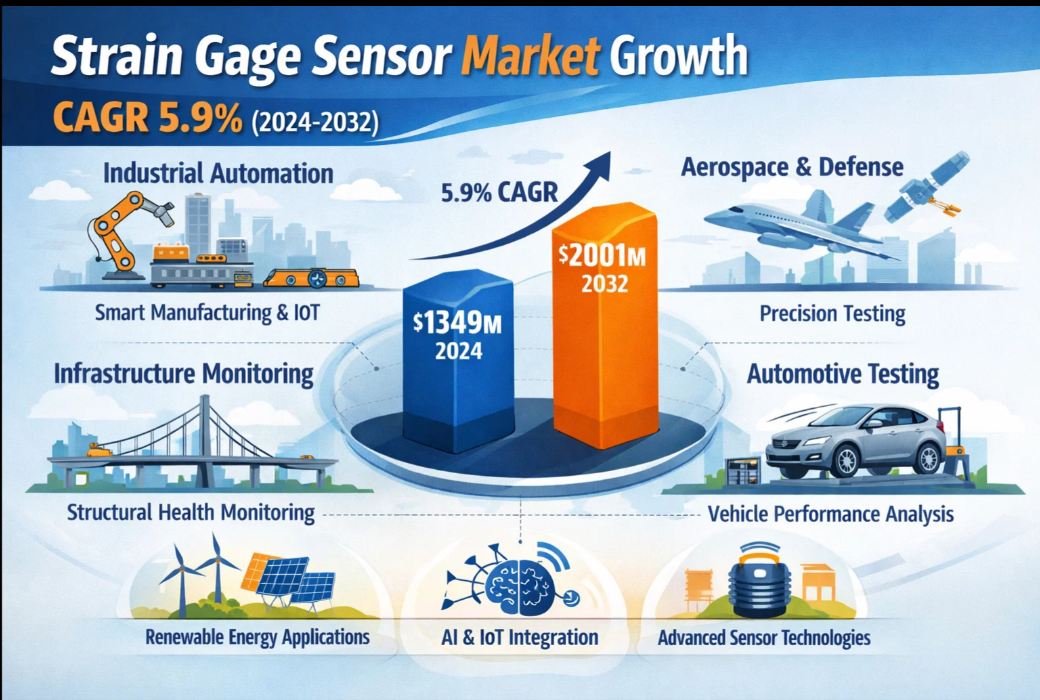

The global Strain Gage Based Sensor Market, valued at US$ 1349 million in 2024, is poised for substantial growth, projected to reach US$ 2001 million by 2032. This expansion, representing a compound annual growth rate (CAGR) of 5.9%, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the indispensable role these precision measurement devices play across industrial automation, aerospace, automotive testing, and infrastructure monitoring sectors.

Strain gage based sensors, fundamental for converting mechanical deformation into electrical signals, have become critical components in modern engineering systems. Their ability to provide accurate, real-time data on stress, force, pressure, and weight makes them essential for ensuring operational safety, quality control, and efficiency optimization across diverse industries. From monitoring structural integrity in bridges to enabling precision in manufacturing processes, these sensors form the backbone of measurement and control systems worldwide.

Industrial Automation and Smart Manufacturing: The Core Growth Drivers

The report identifies the rapid advancement of industrial automation and the global adoption of Industry 4.0 principles as primary catalysts for strain gage sensor demand. As manufacturing facilities increasingly integrate smart technologies and IoT-enabled systems, the need for precise, reliable measurement sensors has surged. These sensors provide critical data for predictive maintenance, process optimization, and quality assurance in automated production lines.

"The convergence of traditional industrial processes with digital technologies creates unprecedented demand for high-accuracy sensing solutions," the report states. "Strain gage sensors serve as the fundamental data acquisition point in countless automated systems, from robotic assembly arms to precision weighing stations. Their reliability under harsh industrial conditions and ability to provide micron-level accuracy make them irreplaceable in modern manufacturing ecosystems."

Read Full Report: https://semiconductorinsight.com/report/strain-gage-based-sensor-market/

Market Segmentation: Industrial Measurement and Alloy Steel Sensors Dominate

The report provides detailed segmentation analysis, offering clear insights into market structure and key growth areas:

Segment Analysis:

By Type

Alloy Steel Sensors

Aluminum Sensors

Stainless Steel Sensors

Other Material Sensors

By Application

Industrial Measurement and Control

Industrial and Commercial Weighing

Aerospace and Defense

Automotive Testing

Others

By End-User Industry

Manufacturing

Aerospace and Defense

Automotive

Construction and Infrastructure

Others

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=122853

Competitive Landscape: Key Players and Strategic Focus

The report profiles key industry players, including:

HBK (Hottinger Brüel & Kjær) (Germany)

Vishay Precision Group (U.S.)

Mettler-Toledo International Inc. (U.S.)

Flintec (Sweden)

MinebeaMitsumi Inc. (Japan)

KeLi Sensing Technology (China)

ZEMIC Europe B.V. (Netherlands)

Kistler Group (Switzerland)

Guangdong South China Sea Electronic Measuring Technology Co., Ltd. (China)

Guangzhou Electrical Measuring Instruments Factory (China)

LCT (China)

These companies are focusing on technological innovations, including the development of wireless strain gage sensors, enhanced environmental resistance, and integration with IIoT platforms. Geographic expansion into emerging markets and strategic partnerships with automation solution providers represent additional growth strategies being pursued by industry leaders.

Emerging Opportunities in Renewable Energy and Infrastructure Monitoring

Beyond traditional industrial applications, the report highlights significant emerging opportunities in renewable energy and smart infrastructure development. The global transition toward sustainable energy sources requires sophisticated monitoring systems for wind turbine blades, solar panel structures, and hydroelectric facilities. Similarly, aging infrastructure in developed economies and new construction in emerging markets drive demand for structural health monitoring systems utilizing strain gage technology.

Furthermore, the integration of artificial intelligence and machine learning with sensor data creates new value propositions. Smart strain gage systems can now predict maintenance needs, optimize operational parameters, and provide insights that were previously inaccessible. This technological convergence represents a major trend transforming how industries utilize measurement data for decision-making and process improvement.

Report Scope and Availability

The market research report offers comprehensive analysis of the global and regional Strain Gage Based Sensor markets from 2025–2032. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and evaluation of key market dynamics.

For detailed analysis of market drivers, restraints, opportunities, and competitive strategies of key players, access the complete report.

Download FREE Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=122853

Get Full Report Here: https://semiconductorinsight.com/report/strain-gage-based-sensor-market/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

Website: https://semiconductorinsight.com/

International: +91 8087 99 2013

LinkedIn: Follow Us

#StrainGageSensors #SensorMarket #IndustrialAutomation #Industry40 #SmartManufacturing #IIoT #AerospaceTechnology #AutomotiveTesting #InfrastructureMonitoring #RenewableEnergy #SensorTechnology #MarketResearch #SemiconductorInsight

The global Strain Gage Based Sensor Market, valued at US$ 1349 million in 2024, is poised for substantial growth, projected to reach US$ 2001 million by 2032. This expansion, representing a compound annual growth rate (CAGR) of 5.9%, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the indispensable role these precision measurement devices play across industrial automation, aerospace, automotive testing, and infrastructure monitoring sectors.

Strain gage based sensors, fundamental for converting mechanical deformation into electrical signals, have become critical components in modern engineering systems. Their ability to provide accurate, real-time data on stress, force, pressure, and weight makes them essential for ensuring operational safety, quality control, and efficiency optimization across diverse industries. From monitoring structural integrity in bridges to enabling precision in manufacturing processes, these sensors form the backbone of measurement and control systems worldwide.

Industrial Automation and Smart Manufacturing: The Core Growth Drivers

The report identifies the rapid advancement of industrial automation and the global adoption of Industry 4.0 principles as primary catalysts for strain gage sensor demand. As manufacturing facilities increasingly integrate smart technologies and IoT-enabled systems, the need for precise, reliable measurement sensors has surged. These sensors provide critical data for predictive maintenance, process optimization, and quality assurance in automated production lines.

"The convergence of traditional industrial processes with digital technologies creates unprecedented demand for high-accuracy sensing solutions," the report states. "Strain gage sensors serve as the fundamental data acquisition point in countless automated systems, from robotic assembly arms to precision weighing stations. Their reliability under harsh industrial conditions and ability to provide micron-level accuracy make them irreplaceable in modern manufacturing ecosystems."

Read Full Report: https://semiconductorinsight.com/report/strain-gage-based-sensor-market/

Market Segmentation: Industrial Measurement and Alloy Steel Sensors Dominate

The report provides detailed segmentation analysis, offering clear insights into market structure and key growth areas:

Segment Analysis:

By Type

Alloy Steel Sensors

Aluminum Sensors

Stainless Steel Sensors

Other Material Sensors

By Application

Industrial Measurement and Control

Industrial and Commercial Weighing

Aerospace and Defense

Automotive Testing

Others

By End-User Industry

Manufacturing

Aerospace and Defense

Automotive

Construction and Infrastructure

Others

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=122853

Competitive Landscape: Key Players and Strategic Focus

The report profiles key industry players, including:

HBK (Hottinger Brüel & Kjær) (Germany)

Vishay Precision Group (U.S.)

Mettler-Toledo International Inc. (U.S.)

Flintec (Sweden)

MinebeaMitsumi Inc. (Japan)

KeLi Sensing Technology (China)

ZEMIC Europe B.V. (Netherlands)

Kistler Group (Switzerland)

Guangdong South China Sea Electronic Measuring Technology Co., Ltd. (China)

Guangzhou Electrical Measuring Instruments Factory (China)

LCT (China)

These companies are focusing on technological innovations, including the development of wireless strain gage sensors, enhanced environmental resistance, and integration with IIoT platforms. Geographic expansion into emerging markets and strategic partnerships with automation solution providers represent additional growth strategies being pursued by industry leaders.

Emerging Opportunities in Renewable Energy and Infrastructure Monitoring

Beyond traditional industrial applications, the report highlights significant emerging opportunities in renewable energy and smart infrastructure development. The global transition toward sustainable energy sources requires sophisticated monitoring systems for wind turbine blades, solar panel structures, and hydroelectric facilities. Similarly, aging infrastructure in developed economies and new construction in emerging markets drive demand for structural health monitoring systems utilizing strain gage technology.

Furthermore, the integration of artificial intelligence and machine learning with sensor data creates new value propositions. Smart strain gage systems can now predict maintenance needs, optimize operational parameters, and provide insights that were previously inaccessible. This technological convergence represents a major trend transforming how industries utilize measurement data for decision-making and process improvement.

Report Scope and Availability

The market research report offers comprehensive analysis of the global and regional Strain Gage Based Sensor markets from 2025–2032. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and evaluation of key market dynamics.

For detailed analysis of market drivers, restraints, opportunities, and competitive strategies of key players, access the complete report.

Download FREE Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=122853

Get Full Report Here: https://semiconductorinsight.com/report/strain-gage-based-sensor-market/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

Website: https://semiconductorinsight.com/

International: +91 8087 99 2013

LinkedIn: Follow Us

#StrainGageSensors #SensorMarket #IndustrialAutomation #Industry40 #SmartManufacturing #IIoT #AerospaceTechnology #AutomotiveTesting #InfrastructureMonitoring #RenewableEnergy #SensorTechnology #MarketResearch #SemiconductorInsight

Strain Gage Based Sensor Market to Grow at 5.9% CAGR Through 2032 Driven by Automation and IoT

The global Strain Gage Based Sensor Market, valued at US$ 1349 million in 2024, is poised for substantial growth, projected to reach US$ 2001 million by 2032. This expansion, representing a compound annual growth rate (CAGR) of 5.9%, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the indispensable role these precision measurement devices play across industrial automation, aerospace, automotive testing, and infrastructure monitoring sectors.

Strain gage based sensors, fundamental for converting mechanical deformation into electrical signals, have become critical components in modern engineering systems. Their ability to provide accurate, real-time data on stress, force, pressure, and weight makes them essential for ensuring operational safety, quality control, and efficiency optimization across diverse industries. From monitoring structural integrity in bridges to enabling precision in manufacturing processes, these sensors form the backbone of measurement and control systems worldwide.

Industrial Automation and Smart Manufacturing: The Core Growth Drivers

The report identifies the rapid advancement of industrial automation and the global adoption of Industry 4.0 principles as primary catalysts for strain gage sensor demand. As manufacturing facilities increasingly integrate smart technologies and IoT-enabled systems, the need for precise, reliable measurement sensors has surged. These sensors provide critical data for predictive maintenance, process optimization, and quality assurance in automated production lines.

"The convergence of traditional industrial processes with digital technologies creates unprecedented demand for high-accuracy sensing solutions," the report states. "Strain gage sensors serve as the fundamental data acquisition point in countless automated systems, from robotic assembly arms to precision weighing stations. Their reliability under harsh industrial conditions and ability to provide micron-level accuracy make them irreplaceable in modern manufacturing ecosystems."

Read Full Report: https://semiconductorinsight.com/report/strain-gage-based-sensor-market/

Market Segmentation: Industrial Measurement and Alloy Steel Sensors Dominate

The report provides detailed segmentation analysis, offering clear insights into market structure and key growth areas:

Segment Analysis:

By Type

Alloy Steel Sensors

Aluminum Sensors

Stainless Steel Sensors

Other Material Sensors

By Application

Industrial Measurement and Control

Industrial and Commercial Weighing

Aerospace and Defense

Automotive Testing

Others

By End-User Industry

Manufacturing

Aerospace and Defense

Automotive

Construction and Infrastructure

Others

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=122853

Competitive Landscape: Key Players and Strategic Focus

The report profiles key industry players, including:

HBK (Hottinger Brüel & Kjær) (Germany)

Vishay Precision Group (U.S.)

Mettler-Toledo International Inc. (U.S.)

Flintec (Sweden)

MinebeaMitsumi Inc. (Japan)

KeLi Sensing Technology (China)

ZEMIC Europe B.V. (Netherlands)

Kistler Group (Switzerland)

Guangdong South China Sea Electronic Measuring Technology Co., Ltd. (China)

Guangzhou Electrical Measuring Instruments Factory (China)

LCT (China)

These companies are focusing on technological innovations, including the development of wireless strain gage sensors, enhanced environmental resistance, and integration with IIoT platforms. Geographic expansion into emerging markets and strategic partnerships with automation solution providers represent additional growth strategies being pursued by industry leaders.

Emerging Opportunities in Renewable Energy and Infrastructure Monitoring

Beyond traditional industrial applications, the report highlights significant emerging opportunities in renewable energy and smart infrastructure development. The global transition toward sustainable energy sources requires sophisticated monitoring systems for wind turbine blades, solar panel structures, and hydroelectric facilities. Similarly, aging infrastructure in developed economies and new construction in emerging markets drive demand for structural health monitoring systems utilizing strain gage technology.

Furthermore, the integration of artificial intelligence and machine learning with sensor data creates new value propositions. Smart strain gage systems can now predict maintenance needs, optimize operational parameters, and provide insights that were previously inaccessible. This technological convergence represents a major trend transforming how industries utilize measurement data for decision-making and process improvement.

Report Scope and Availability

The market research report offers comprehensive analysis of the global and regional Strain Gage Based Sensor markets from 2025–2032. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and evaluation of key market dynamics.

For detailed analysis of market drivers, restraints, opportunities, and competitive strategies of key players, access the complete report.

Download FREE Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=122853

Get Full Report Here: https://semiconductorinsight.com/report/strain-gage-based-sensor-market/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us

#StrainGageSensors #SensorMarket #IndustrialAutomation #Industry40 #SmartManufacturing #IIoT #AerospaceTechnology #AutomotiveTesting #InfrastructureMonitoring #RenewableEnergy #SensorTechnology #MarketResearch #SemiconductorInsight