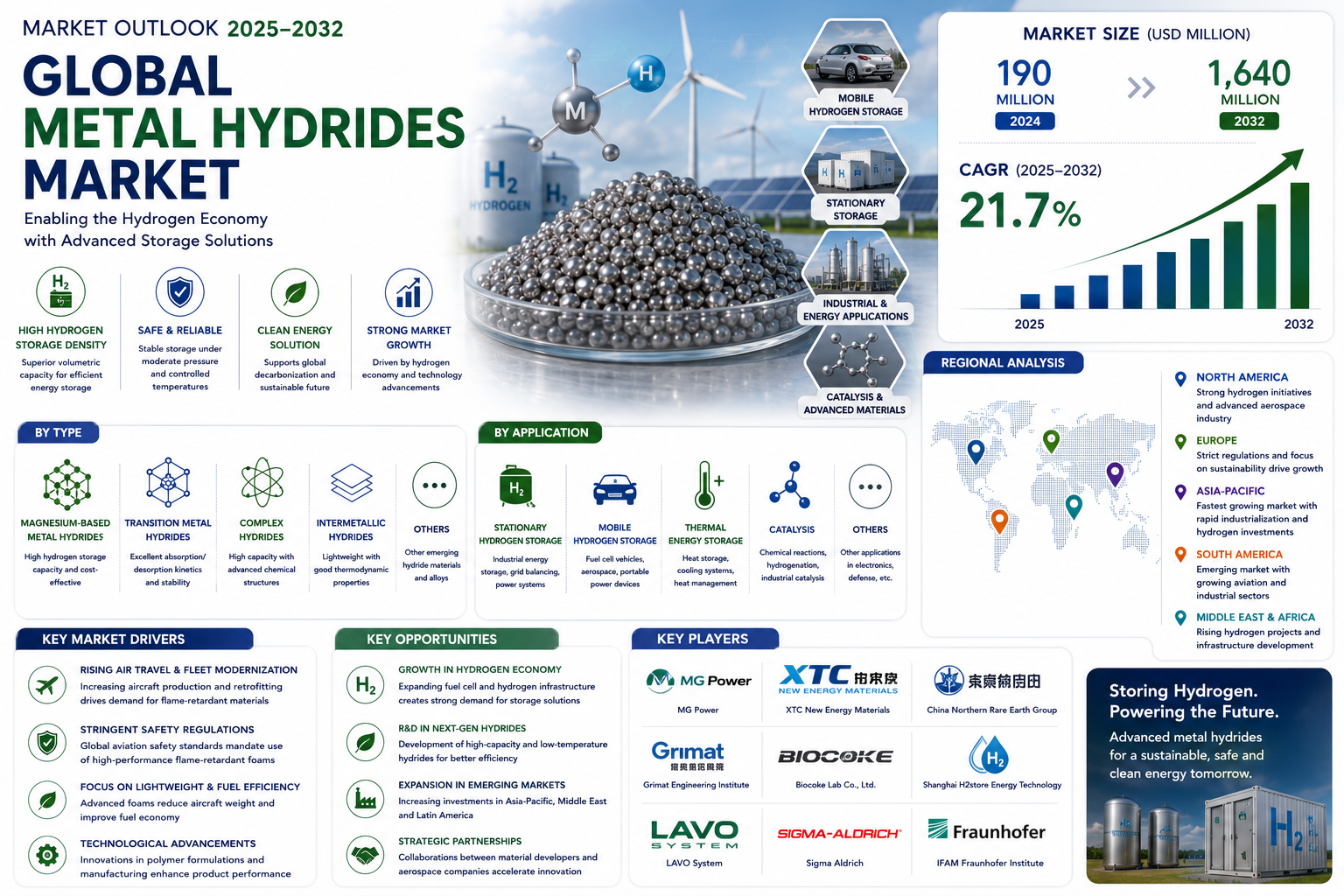

Global Metal Hydrides Market to Reach USD 1,640 Million by 2032, Growing at 21.7% CAGR

Global metal hydrides market size was valued at USD 413 million in 2024 and is projected to reach USD 1640 million by 2032, growing at a CAGR of 21.7% during the forecast period.

Metal hydrides are compounds formed by the reaction of metals or alloys with hydrogen, where hydrogen exists either as a negatively charged ion (H⁻) or in a covalently bonded state. These materials exhibit excellent hydrogen storage capacity and are widely used in solid-state hydrogen storage, hydrogen fuel cells, thermal energy storage, catalysis, and nuclear reactor control. Based on their chemical bonding and structure, metal hydrides can be classified into ionic hydrides (e.g., LiH, NaH), covalent hydrides (e.g., TiH₂), transition metal hydrides (e.g., LaNi₅H₆), and complex hydrides (e.g., Mg₂FeH₆).

The market growth is primarily driven by advancements in hydrogen energy technologies and increasing demand for efficient energy storage solutions. The U.S. accounted for a significant market share in 2024, while China is emerging as a fast-growing regional market. Magnesium-based metal hydrides are expected to show strong growth potential due to their high hydrogen storage density. Key players such as MG Power, XTC New Energy Materials, and China Northern Rare Earth are actively developing innovative solutions to meet the growing demand across stationary and mobile hydrogen storage applications.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/295540/metal-hydrides-market

Market Overview & Regional Analysis

The North American metal hydrides market is driven by clean energy initiatives and technological advancements in hydrogen storage solutions. The U.S. dominates the region with significant investments in hydrogen infrastructure, particularly for fuel cell applications. The Department of Energy's $7 billion hydrogen hub program underscores the growing emphasis on metal hydrides for energy storage. Canada follows closely, leveraging its renewable energy resources to develop hydrogen-based energy systems. Industry players are focusing on magnesium-based hydrides due to their high hydrogen storage capacity, though cost and thermal management remain key challenges.

Europe leads in sustainable hydrogen technologies, with the EU's Hydrogen Strategy targeting 40 GW of electrolyzer capacity by 2030. Countries like Germany and France are pioneering research into metal hydrides for both stationary and mobile hydrogen storage, backed by strong policy support. However, the high production costs of advanced hydrides hinder widespread adoption. The Nordic countries are emerging as innovation hubs, particularly for thermal energy storage applications. Strict regulatory frameworks ensure that environmental and safety standards heavily influence material development paths.

As the fastest-growing market, Asia-Pacific benefits from China's aggressive hydrogen energy roadmap and Japan's fuel cell vehicle proliferation. China accounts for over 35% of global hydrogen production, creating substantial demand for storage solutions. India's National Hydrogen Mission is driving R&D in hydride technologies, though commercialization remains nascent. While cost-effective solutions currently dominate, there's growing investment in complex hydrides with better performance characteristics. The region's manufacturing capabilities position it as both a major consumer and future exporter of metal hydride products.

South America presents an emerging market with Chile's green hydrogen ambitions leading regional growth. Brazil's automotive sector shows increasing interest in hydrogen technologies, creating demand potential. However, underdeveloped hydrogen infrastructure and limited R&D funding slow market penetration. Argentina's lithium resources could enable future development of lithium-based hydrides. Economic instability in several countries creates investment uncertainty, causing most activity to concentrate in stable markets with clear energy transition policies.

The Gulf Cooperation Council (GCC) countries are pivoting from oil to hydrogen as part of diversification strategies, with Saudi Arabia's NEOM project incorporating large-scale hydrogen storage. South Africa's mineral resources support hydride material production, while North African nations explore hydrogen exports to Europe. Infrastructure gaps and water scarcity for hydrogen production present hurdles. The market shows long-term promise as renewable energy projects mature, with metal hydrides positioned as critical for stabilizing intermittent energy supply across the region.

Key Market Drivers and Opportunities

Global shift toward clean energy is creating unprecedented demand for efficient hydrogen storage solutions, with metal hydrides emerging as a key enabling technology. As countries implement ambitious carbon neutrality targets – with over 140 nations now committed to net-zero emissions – hydrogen-based energy systems are gaining traction. Metal hydrides offer superior volumetric storage density compared to compressed gas or liquid hydrogen, with some alloys capable of storing hydrogen at densities exceeding liquid hydrogen at standard conditions. The European Union's recently announced Hydrogen Strategy, targeting 40GW of electrolyzer capacity by 2030, exemplifies the policy momentum driving this sector forward.

Breakthroughs in fuel cell design and materials science are creating new opportunities for metal hydride integration across transportation and stationary applications. Recent innovations in proton-exchange membrane (PEM) fuel cells now enable operating temperatures compatible with magnesium-based hydrides, previously limited by their higher desorption temperatures. The fuel cell vehicle market, projected to grow at 25% CAGR through 2030, increasingly relies on metal hydride systems for onboard hydrogen storage. Japan's ENE-FARM program, which has deployed over 400,000 residential fuel cell systems since 2009, demonstrates the viability of this technology at commercial scale. Furthermore, research breakthroughs in complex hydrides are overcoming traditional limitations. Recent developments in catalyst-doped sodium alanates have achieved hydrogen release temperatures below 100°C, making these materials viable for portable applications. Such technological advancements are rapidly expanding the addressable market for metal hydride solutions.

The integration of metal hydrides into renewable energy systems presents substantial growth potential. Hydride-based thermal energy storage systems are gaining attention for addressing intermittency in solar and wind power, with pilot projects demonstrating efficiency advantages over conventional battery solutions. These systems leverage the exothermic nature of hydrogen absorption to store and release thermal energy on demand, achieving round-trip efficiencies exceeding 70% in recent trials.

Advances in nanotechnology and computational materials design are unlocking previously unavailable hydride formulations. Machine learning-assisted discovery of novel alloy compositions has accelerated materials development cycles by up to 80% compared to traditional methods. Researchers recently identified several ternary hydride systems with theoretically predicted capacities exceeding 7 wt%, potentially overcoming longtime gravimetric capacity limitations.

Challenges & Restraints

The metal hydrides market faces significant barriers related to production economics, with rare earth elements like lanthanum and cerium constituting substantial portions of many high-performance alloys. Current production costs for commercial-grade hydrogen storage alloys range significantly higher than conventional storage methods, creating adoption hurdles in price-sensitive markets. Complex activation procedures – often requiring multiple hydrogen absorption/desorption cycles under controlled conditions – further increase system implementation costs.

Many promising metal hydride formulations remain impractical due to unfavorable thermodynamic properties. Certain high-capacity alloys require temperatures above 300°C for hydrogen release, limiting applications where thermal management is challenging. Researchers continue struggling to simultaneously optimize storage capacity, kinetics, and operating temperatures across different hydride classes. The nascent hydrogen economy lacks supporting infrastructure for metal hydride-based systems. Standardization of refueling protocols, recycling processes, and safety certifications remains incomplete across most regions. This uncertainty discourages investment across the value chain, from material suppliers to end-users.

Long-term performance degradation presents persistent challenges for metal hydride deployment. Many alloys suffer progressive capacity loss through hydrogen cycling, with some formulations losing over 30% of initial storage capacity within 500 cycles. Microstructural changes including particle pulverization and surface oxidation contribute to this performance decay. The industry continues to invest heavily in surface modification techniques and protective coatings to mitigate these effects.

Proper handling of pyrophoric hydrides requires specialized infrastructure from production through disposal. Accidental air exposure of certain activated alloys can cause spontaneous ignition, necessitating stringent safety protocols. These requirements add complexity to logistics and maintenance operations. Evolving hydrogen storage regulations create compliance challenges. Jurisdictional differences in pressure vessel codes, transportation rules, and material handling standards complicate global market access. Recent updates to ISO 16111 standards illustrate the dynamic regulatory landscape affecting metal hydride systems.

Market Segmentation by Type

● Magnesium-based Metal Hydrides

● Transition Metal Hydrides

● Complex Hydrides

● Intermetallic Hydrides

● Others

Magnesium-based Metal Hydrides segment leads due to high hydrogen storage efficiency.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/295540/metal-hydrides-market

Market Segmentation by Application

● Stationary Hydrogen Storage

● Mobile Hydrogen Storage

● Thermal Energy Storage

● Catalysis

● Others

Stationary Hydrogen Storage segment dominates for industrial and energy applications.

Market Segmentation and Key Players

● MG Power (Switzerland)

● XTC New Energy Materials (China)

● Grimat Engineering Institute (China)

● China Northern Rare Earth Group (China)

● Biocoke Lab Co., Ltd. (Japan)

● Shanghai H2store Energy Technology (China)

● LAVO System (Australia)

● Sigma Aldrich (Germany)

● IFAM Fraunhofer Institute (Germany)

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Metal Hydrides, covering the period from 2024 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

● Sales, sales volume, and revenue forecasts

● Detailed segmentation by type and application

The report features in-depth competitive intelligence including:

● Market share analysis of leading manufacturers

● Production capacity expansions

● Product portfolio assessments

● Strategic partnership evaluations

Our research methodology combines primary interviews with industry leaders and comprehensive data analysis of:

● Production facilities and their geographical distribution

● Raw material sourcing patterns

● End-user industry consumption trends

● Regulatory impact assessments

Get Full Report Here: https://www.24chemicalresearch.com/reports/295540/global-aluminum-plate-sheet-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

分类

閱讀更多

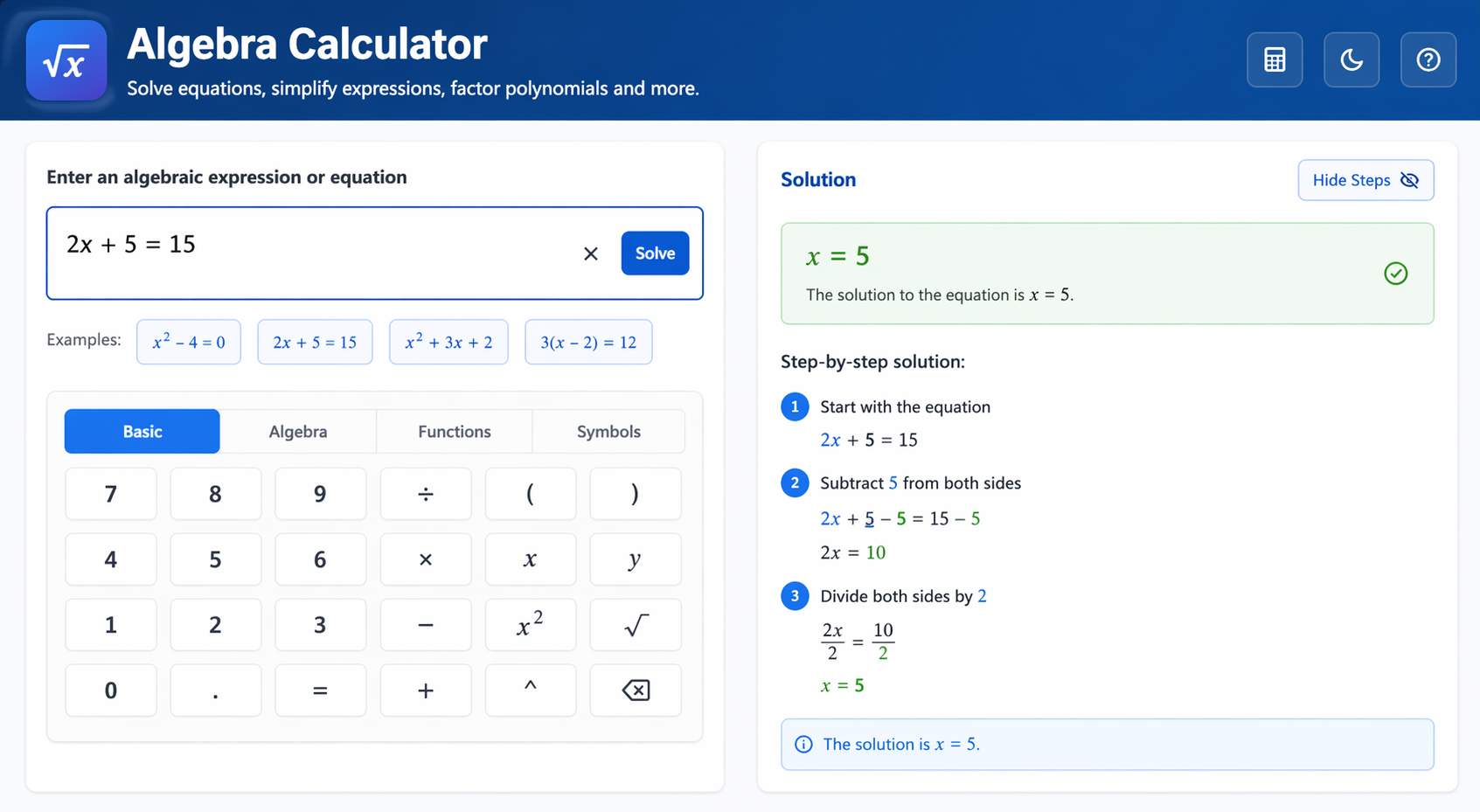

An Algebra Calculator is a very helpful tool for students, teachers, and anyone who works with numbers. Algebra can sometimes feel confusing because it includes variables, equations, and different rules. Many people struggle to solve algebra problems by hand, especially when the equations become long or complex. This is where an algebra calculator becomes useful. An algebra calculator helps you...

Buy Old Gmail Accounts: Unlock Trust, Access, and Growth 🐼📲📶💻🦋 Telegram: @progmbofficial 🐼📲📶💻🦋 WhatsApp: +1 (984) 291-3274 🐼📲📶💻🦋 Telegram: @progmbofficial 🐼📲📶💻🦋 Email: progmb.contact@gmail.com 🐼📲📶💻🦋 Visit Our Website: https://www.progmb.com/product/buy-old-gmail-accounts/ In today’s digital landscape, owning old Gmail accounts offers unique advantages for businesses and marketers....

The design and implementation of a modern, secure automation platform require a meticulous approach to engineering, where every component must work in harmony to ensure continuous operation. In the context of building a resilient Web Development Market platform, stakeholders must prioritize interoperability, virtualized management, and high-density performance. These platforms act as...

Best Websites to Buy Apple ID Accounts in Today Buy Apple ID Accounts with secure access and ready-to-use features for personal or business needs. Verified Apple ID accounts help users access the App Store, iCloud, Apple Music, FaceTime, and many other Apple services without hassle. These accounts are useful for developers, marketers, app testing, online services, and digital activities that...