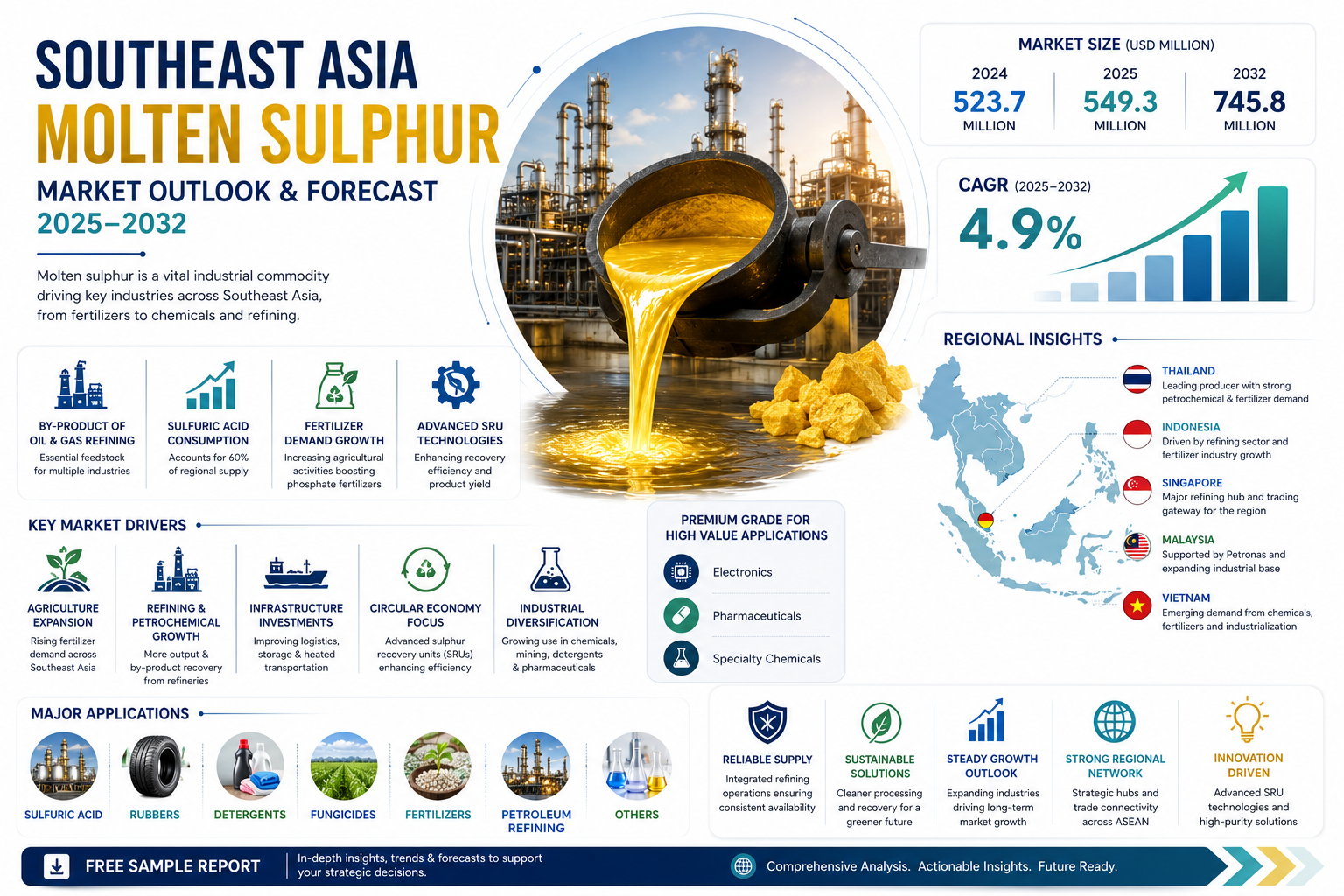

Southeast Asia Molten Sulphur Market to Reach USD 745.8 Million by 2032, Growing at 4.9% CAGR

The Southeast Asia Molten Sulphur market size was valued at USD 523.7 million in 2024. The market is projected to grow from USD 549.3 million in 2025 to USD 745.8 million by 2032, exhibiting a CAGR of 4.9% during the forecast period.

Molten sulphur is liquid elemental sulphur, a critical industrial commodity primarily produced as a byproduct of oil and gas refining and natural gas processing. It serves as a fundamental raw material for the production of sulfuric acid, which is arguably its most significant application. Other key uses include the manufacturing of fertilizers, particularly phosphate fertilizers, rubber vulcanization in the tire industry, and various chemical synthesis processes.

Market growth is underpinned by the robust expansion of the regional petrochemical and fertilizer industries. For instance, the sulfuric acid production sector, which consumes 60% of the regional supply, is a primary driver. Furthermore, increasing agricultural activities are fueling demand for phosphate fertilizers, which in turn boosts consumption. The market is also characterized by technological advancements in sulphur recovery units (SRUs) at refineries, enhancing yield and efficiency. Key regional players such as PTT Global Chemical, Petronas, and Pertamina are significant contributors to the market's supply chain, with ongoing investments in refining capacity supporting steady production.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/279761/asia-southeast-molten-sulphur-market

Market Overview & Regional Analysis

Thailand leads the Southeast Asia Molten Sulphur market as a primary production hub within the top trio alongside Singapore and Indonesia, which together dominate regional output. Its robust petrochemical industry generates molten sulphur as a refining byproduct, fueling sulfuric acid production, the largest consumption segment. Fertilizer manufacturing and rubber vulcanization, driven by automotive and tire sectors, represent key demand areas. The shift towards circular economy principles has improved sulphur recovery efficiency from oil and gas operations. High-purity molten sulphur demand surges for specialty chemicals in electronics and pharmaceuticals. Major players like Thai Oil Public Company Limited and PTT Global Chemical Public Company Limited enhance competitiveness through advanced technologies. Strategic investments in heated transportation and storage facilities address logistics challenges, ensuring reliable supply chains. This positions Thailand centrally in regional market dynamics, supporting moderate growth amid expanding industrial applications.

Thailand's refineries excel in molten sulphur output from oil and gas byproducts, with leading firms optimizing recovery processes for consistency and volume. Efficient supply chains support regional exports, bolstered by major producers like Thai Oil and PTT Global Chemical. Sulfuric acid production dominates consumption, followed by fertilizers and rubber vulcanization. Automotive and tire industries drive steady demand growth, while phosphoric acid applications reflect expanding agriculture needs. Investments in heated storage and transportation solutions grow to maintain molten state integrity. These advancements mitigate handling challenges, enhancing market reliability and trade efficiency. High-purity sulphur for electronics and pharmaceuticals sees rising adoption. Circular recovery practices and petrochemical expansion promise sustained market momentum.

Indonesia contributes substantially to regional molten sulphur production through its oil and gas sector, with Pertamina playing a pivotal role in refining byproducts. Demand primarily arises from sulfuric acid and fertilizer manufacturing, essential for agriculture. Petroleum refining applications further support consumption. Alignment with regional trends in recovery efficiency and logistics improvements strengthens supply dynamics. The fertilizer industry's growth, tied to phosphoric acid production, underscores Indonesia's market significance amid Southeast Asia's industrial expansion.

Singapore, a premier refining hub, generates key molten sulphur volumes, led by global players like Chevron Corporation, Royal Dutch Shell, and ExxonMobil. High-purity variants cater to specialty chemicals, electronics, and pharmaceuticals. Its strategic location facilitates trade and distribution across the region. Advanced storage infrastructure ensures quality preservation. Sulfuric acid remains the core application, with focus on efficient logistics and value chain integration driving competitive positioning.

Vietnam's developing petrochemical landscape boosts molten sulphur utilization in sulfuric acid production and fertilizers, spearheaded by Vietnam Oil and Gas Group (PetroVietnam). Emerging demand in detergents, fungicides, and other applications reflects industrial diversification. Investments in manufacturing technologies and industry chains enhance self-sufficiency. Regional trends in sulphur recovery and logistics support Vietnam's gradual market integration and growth potential.

Malaysia leverages Petronas and Hengyi Industries for molten sulphur from refining processes, serving sulfuric acid, fertilizers, rubber, and petroleum refining sectors. Strategic focus on value chain analysis and sustainable practices aligns with circular economy shifts. Logistics enhancements and high-purity demand for downstream uses bolster resilience. The market benefits from regional petrochemical synergies, positioning Malaysia as a steady contributor.

Key Market Drivers and Opportunities

Southeast Asia's agricultural sector, a cornerstone of the regional economy, is experiencing robust expansion, particularly in palm oil, rice, and rubber production across Indonesia, Thailand, and Vietnam. This surge directly boosts demand for molten sulphur, essential for manufacturing sulphuric acid used in phosphate fertilizers. With fertilizer consumption in the region reaching 25 million metric tons annually and growing at 5.2% CAGR through 2028, refineries and suppliers are ramping up molten sulphur output to meet this need.

The proliferation of oil refineries and petrochemical complexes in Malaysia and Indonesia generates substantial molten sulphur as a byproduct during crude oil desulphurization. For instance, regional refining capacity has increased by 15% over the past five years, yielding over 2.5 million tons of molten sulphur yearly. This byproduct not only supports local industries but also positions Southeast Asia as a net exporter, enhancing market dynamics.

Government subsidies for agriculture in Vietnam and Thailand have accelerated fertilizer adoption, indirectly driving molten sulphur demand by 7% year-on-year. Furthermore, infrastructure investments under ASEAN initiatives are improving supply chains, making molten sulphur more accessible for downstream applications like mining and chemical manufacturing. While short-term fluctuations occur, the long-term trajectory remains upward due to these intertwined industrial advancements.

Southeast Asia's burgeoning petrochemical industry, with new complexes in Vietnam's Long Son and Malaysia's Pengerang, presents prime avenues for molten sulphur integration in acid production. Projected capacity additions of 5 million tons by 2030 could absorb an extra 1.2 million tons of sulphur annually. In mining, Indonesia's nickel boom requires sulphuric acid for leaching processes, opening doors for local molten sulphur supply chains. Growth in battery manufacturing for EVs further amplifies this demand, potentially adding 8% to regional consumption. Technological innovations like advanced heating pipelines and blended sulphur products mitigate logistics woes, fostering intra-regional trade. Collaborations under RCEP could streamline tariffs, unlocking export potential to Australia and India.

Challenges & Restraints

Transporting molten sulphur requires specialized heated tankers and railcars to maintain temperatures above 130°C, posing significant logistical challenges in Southeast Asia's archipelago geography. Delays from port congestions in Singapore and Indonesia can lead to solidification, resulting in up to 10% product loss and escalated costs estimated at $50-70 per ton. Fluctuating energy prices further compound these issues, as heating requirements strain operational budgets amid volatile bunker fuel costs. Additionally, monsoonal weather disrupts maritime routes, impacting timely delivery to key markets like the Philippines.

Refinery maintenance shutdowns and crude slate variations cause irregular molten sulphur output, with Southeast Asia experiencing supply dips of 20% during peak turnaround periods. This unpredictability challenges end-users in planning procurement. Granulated and solid sulphur imports from the Middle East undercut molten sulphur on price, capturing 30% market share in cost-sensitive segments despite higher handling costs.

Heightened environmental standards across Southeast Asia, including Indonesia's sulphur emission caps and Thailand's cleaner production mandates, restrict molten sulphur handling and storage. Compliance costs have risen by 12-15% for facilities, deterring smaller players and consolidating the market among major refiners. Moreover, the push towards low-sulphur fuels under IMO 2020 has paradoxically reduced byproduct yields from some refineries, tightening supply. However, this also incentivizes efficiency upgrades. Regional H2S emission limits add layers of permitting delays, slowing project timelines by 6-9 months. Trade barriers and tariffs on sulphur imports/exports between ASEAN members create uneven playing fields, particularly affecting landlocked areas in Laos and Myanmar. These factors collectively temper market expansion despite underlying demand.

Market Segmentation by Type

● Purity>99.8%

● Purity>99.5%

Purity >99.8% emerges as the leading segment within the Southeast Asia Molten Sulphur market. This ultra-high purity grade is essential for sophisticated applications in specialty chemicals, particularly supporting the burgeoning electronics and pharmaceutical sectors. Its minimal impurity profile ensures reliable performance in precision manufacturing processes, aligning perfectly with the region's push towards high-tech industries and quality-driven production standards.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/279761/asia-southeast-molten-sulphur-market

Market Segmentation by Application

● Sulfuric Acid

● Rubbers

● Detergents

● Fungicides

● Fertilizers

● Petroleum Refining

● Others

Sulfuric Acid commands the forefront of applications in the Southeast Asia Molten Sulphur market. Serving as the cornerstone input for sulfuric acid manufacturing, it fuels diverse downstream sectors amid the region's petrochemical boom. Integrated refineries and chemical facilities across Southeast Asia prioritize this application for its versatility in enabling essential industrial processes and value-added product development.

Market Segmentation and Key Players

● Pertamina (Indonesia)

● Petronas (Malaysia)

● Thai Oil Public Company Limited (Thailand)

● PTT Global Chemical Public Company Limited (Thailand)

● Philippine National Oil Company (Philippines)

● Chevron Corporation (Singapore Operations)

● Royal Dutch Shell (Singapore)

● ExxonMobil Corporation (Singapore)

● Hengyi Industries (Malaysia)

● Vietnam Oil and Gas Group (PetroVietnam) (Vietnam)

Report Scope

This report presents a comprehensive analysis of the Global and regional markets for Southeast Asia Molten Sulphur, covering the period from 2025 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

● Sales, sales volume, and revenue forecasts

● Detailed segmentation by type and application

The report features in-depth competitive intelligence including:

● Market share analysis of leading manufacturers

● Production capacity expansions

● Product portfolio assessments

● Strategic partnership evaluations

Our research methodology combines primary interviews with industry leaders and comprehensive data analysis of:

● Production facilities and their geographical distribution

● Raw material sourcing patterns

● End-user industry consumption trends

● Regulatory impact assessments

Get Full Report Here: https://www.24chemicalresearch.com/reports/279761/global-aluminum-plate-sheet-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

Categories

Read More

(圖/ 嘉義市木蘭國際同濟會) 為關懷嘉義地區弱勢學童並傳遞社會溫暖,嘉義市木蘭國際同濟會將於近日舉辦第38屆年度公益活動——「木蘭送暖・原聲傳愛」冬季制服籌募音樂會,透過音樂結合公益行動,號召社會各界攜手為學童送上冬日暖流。 本次活動以「一善三助」為核心精神,捐助所得將專款用於協助嘉義地區約500位弱勢國小學童添購冬季制服,同時延伸關懷至南投布農族與新竹泰雅族部落學童,透過藝術表演建立自信,拓展視野,走向國際舞台。 音樂會特別邀請「台灣原聲童聲合唱團」與榮獲國際大賽金質獎的「泰雅男伶」,以及原住民歌謠比賽冠軍「南賢天老師」聯手演出,將以悠揚純淨的天籟美聲,喚起社會大眾對弱勢兒童教育與成長需求的關注,讓音樂成為傳愛的橋樑。 (圖/ 嘉義市木蘭國際同濟會)...

Buy Old Gmail Accounts Are you looking to enhance your online presence and communication capabilities? Delve into the realm of old Gmail accounts - a strategic solution to amplify your digital footprint. In this insightful article, discover the untapped potential and benefits of investing in established Gmail accounts. Expect to uncover a treasure trove of opportunities that will revolutionize...