Neodymium Market to Reach US$ 5.0 Billion by 2036 Amid Rising Demand from EVs and Wind Energy

The global neodymium market is poised for significant growth over the coming decade as the accelerating adoption of electric vehicles (EVs), expansion of renewable energy infrastructure, and increasing deployment of high-performance permanent magnets continue to reshape industrial demand patterns. According to the latest market assessment, the global neodymium market was valued at US$ 2.1 billion in 2025 and is projected to reach US$ 5.0 billion by 2036, registering a compound annual growth rate (CAGR) of 8.0% during the forecast period from 2026 to 2036.

Neodymium has emerged as one of the most strategically important rare earth elements due to its exceptional magnetic, optical, and metallurgical properties. The material serves as a critical component in neodymium-iron-boron (NdFeB) permanent magnets, which are widely utilized in electric vehicle motors, wind turbine generators, robotics, consumer electronics, industrial automation equipment, and defense technologies.

As governments and industries worldwide intensify their focus on decarbonization and electrification, neodymium demand is increasingly being driven by structural growth sectors rather than traditional consumer electronics applications. This transition is expected to create long-term opportunities throughout the rare earth value chain.

Electric Vehicle Adoption Creates Strong Demand Foundation

The rapid expansion of the global electric vehicle industry continues to be one of the most influential factors supporting neodymium consumption. Modern electric vehicles rely heavily on permanent magnet synchronous motors that utilize NdFeB magnets to deliver superior performance, higher torque density, improved energy efficiency, and compact design advantages.

Industry estimates indicate that a typical battery-electric passenger vehicle contains approximately 1–2 kilograms of magnet-grade neodymium. Commercial electric vehicles, including buses and light-duty trucks, often require significantly larger quantities due to higher power requirements.

With global electric vehicle sales surpassing 14 million units in recent years and adoption rates expected to remain strong across major automotive markets, demand for neodymium-containing magnets is projected to increase substantially. Manufacturers are increasingly favoring permanent magnet motor technologies to improve vehicle range and performance, reinforcing the material's strategic importance within the transportation sector.

Furthermore, the growing popularity of electric two-wheelers, hybrid vehicles, electric delivery fleets, and heavy-duty electric trucks is expected to broaden the demand base for neodymium products over the next decade.

Renewable Energy Expansion Accelerates Market Growth

The global transition toward renewable energy is creating another powerful demand engine for neodymium producers. Wind energy systems, particularly direct-drive and hybrid-drive turbines, depend heavily on NdFeB permanent magnets to achieve higher efficiency and reduced maintenance requirements.

Unlike conventional generator systems, permanent magnet generators offer lower mechanical losses and improved operational reliability. These advantages are especially valuable in offshore wind installations, where maintenance costs can be substantial.

Large onshore wind turbines typically require between 150 and 250 kilograms of NdFeB magnets per unit. Offshore turbines, especially those exceeding 10 megawatts in capacity, may utilize between 400 and 600 kilograms of magnet material per installation. As countries continue investing in renewable power generation to meet carbon neutrality targets, demand for neodymium is expected to rise accordingly.

Growing offshore wind development across Europe, Asia Pacific, and North America is anticipated to create sustained demand for rare earth permanent magnets throughout the forecast period. This trend is strengthening the role of neodymium as a foundational material within the global clean energy economy.

Permanent Magnets Continue to Dominate Market Demand

Among all application categories, permanent magnets remain the dominant segment within the global neodymium market. The segment accounted for the overwhelming majority of demand in 2025, representing approximately 84% of total market share.

NdFeB magnets are recognized as the most powerful commercially available permanent magnets. Their superior magnetic strength and energy efficiency make them indispensable for advanced industrial applications requiring compact, lightweight, and high-performance magnetic systems.

Beyond electric vehicles and wind turbines, permanent magnets are increasingly utilized in industrial robotics, automated manufacturing systems, aerospace technologies, precision machinery, consumer electronics, and healthcare equipment. As automation and digital transformation continue to advance worldwide, demand for these magnets is expected to remain robust.

The increasing integration of permanent magnet technologies into emerging applications further reinforces the long-term growth prospects of the neodymium market.

Supply Chain Security Becomes a Strategic Priority

The global neodymium industry is characterized by a highly concentrated supply chain structure. China continues to maintain a dominant position in rare earth mining, separation, processing, and magnet manufacturing activities.

This concentration has heightened concerns regarding supply chain resilience, particularly among governments and industries seeking secure access to critical materials required for energy transition technologies. As a result, supply diversification has become a major strategic priority for stakeholders across North America, Europe, Australia, and other regions.

Automotive manufacturers, renewable energy developers, and industrial equipment producers are increasingly pursuing long-term supply agreements, vertical integration strategies, and localized production initiatives to reduce dependence on single-source supply networks.

The emphasis on supply security has elevated the importance of traceability, responsible sourcing, and regional processing capabilities within the global rare earth ecosystem.

Emerging Opportunities in Recycling and Alternative Supply Chains

One of the most promising developments within the neodymium market is the emergence of recycling technologies and non-Chinese supply chains. Industry participants are investing in projects designed to recover rare earth elements from end-of-life electric vehicle motors, wind turbine components, and industrial equipment.

Recycling offers several advantages, including lower energy requirements, reduced environmental impact, and improved supply chain sustainability. Industry forecasts suggest that recycled materials could account for 10% to 15% of global neodymium demand by 2030, helping mitigate supply risks while supporting circular economy objectives.

At the same time, significant investments are being directed toward developing rare earth processing facilities outside China. New projects across Australia, North America, and Europe are aimed at establishing alternative sources of NdPr oxides, metals, and alloys for global manufacturers.

These initiatives are expected to enhance market resilience and provide additional growth opportunities for companies operating throughout the rare earth value chain.

Asia Pacific Leads Global Consumption

Asia Pacific remains the largest regional market for neodymium, accounting for approximately 73% of global revenue in 2025. The region benefits from extensive rare earth processing infrastructure, advanced manufacturing capabilities, and strong demand from electric vehicle and renewable energy sectors.

China continues to play a central role in the industry, producing a significant share of the world's NdFeB magnets and serving as a major hub for downstream manufacturing activities. Japan and South Korea also contribute substantially through their advanced automotive, electronics, and industrial technology sectors.

Europe represents another important growth market, driven by increasing investments in electric mobility and offshore wind projects. The region's commitment to sustainability and carbon reduction objectives is expected to support long-term demand for neodymium-containing technologies.

North America is likewise witnessing increased activity as governments and private-sector organizations invest in domestic rare earth supply chains, renewable energy development, and next-generation manufacturing capabilities.

Competitive Landscape

The global neodymium market features a mix of established rare earth producers and emerging participants focused on supply chain diversification. Key industry players are actively investing in mining operations, separation facilities, metallization plants, and downstream magnet production capabilities.

Leading companies operating within the market include China Minmetals Rare Earth Co. Ltd., Lynas Rare Earth Ltd., Neo Performance Materials Inc., Arafura Resources, Alkane Resources Ltd., Australian Strategic Materials Ltd., American Elements, Noah Technologies Corporation, Metall Rare Earth Limited, and HEFA Rare Earth Canada Co. Ltd.

These organizations are pursuing strategic partnerships, capacity expansions, and technology investments to strengthen their positions in a rapidly evolving market environment.

Recent developments across the industry highlight growing efforts to establish integrated mine-to-metal supply chains, improve processing capabilities, and secure long-term customer relationships across automotive, renewable energy, robotics, and defense sectors.

Future Outlook

The outlook for the global neodymium market remains highly positive as electrification, industrial automation, and renewable energy deployment continue to accelerate worldwide. The material's indispensable role in high-performance permanent magnets positions it at the center of several transformative technological trends.

Over the forecast period, increasing electric vehicle production, expansion of wind energy infrastructure, development of advanced manufacturing systems, and investments in supply chain diversification are expected to drive sustained demand growth.

As governments prioritize critical mineral security and industries seek reliable access to strategic raw materials, neodymium is expected to remain a cornerstone of the global energy transition. Market participants that successfully expand production capabilities, strengthen recycling initiatives, and establish resilient supply networks are likely to benefit from the substantial opportunities emerging across the global neodymium landscape.

分类

閱讀更多

" According to the latest report published by Data Bridge Market Research, the Antimicrobial Drugs Market The global antimicrobial drugs market size was valued at USD 122.89 billion in 2025 and is expected to reach USD 174.76 billion by 2033, at a CAGR of 4.50% during the forecast period This Antimicrobial Drugs Market research report is generated with a...

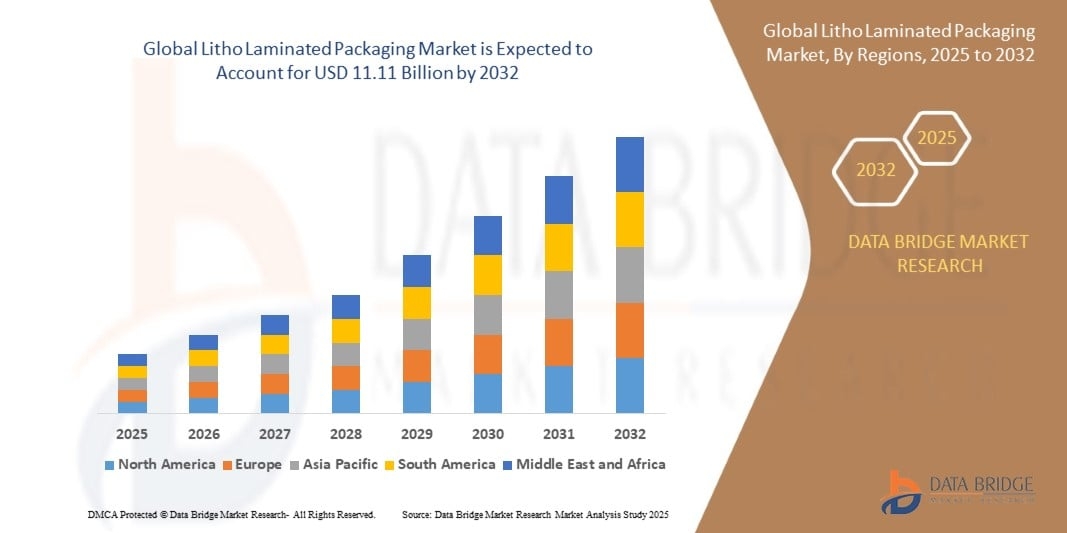

According to the latest report published by Data Bridge Market Research, the Litho Laminated Packaging Market The litho laminated packaging market size was valued at USD 7.46 billion in 2024 and is projected to reach USD 11.11 billion by 2032, with a CAGR of 5.10% during the forecast period of 2025 to 2032. The large scale Litho Laminated Packaging Marketing report studies and...

(圖/ AI生成) 在美歐關係持續緊張與數位主權議題升溫之際,法國政府正式啟動新一波數位自主行動。根據法國總理塞巴斯蒂安.勒科爾尼(Sébastien Lecornu)本週簽署的行政命令,法國政府官員將停止使用Zoom、Microsoft Teams等美國視訊會議軟體,並改採本土開發的視訊平台Visio。相關過渡作業預計於2026年底前完成。此舉被外界視為歐洲主要國家降低對美國數位基礎設施依賴的最新一步。 法國政府指出,Visio為「數位套件計畫」(suite...

According to the latest report published by Data Bridge Market Research, the Europe Surface Disinfectants Market CAGR Value The Europe Surface Disinfectants market was valued at USD 2.03 billion in 2025 and is projected to reach USD 3.33 billion by 2033, growing at a CAGR of 6.40% from 2026 to 2033. The Surface Disinfectants market is experiencing steady growth driven by rising...