Aircraft EMI Protection Coatings Market to Reach USD 0.6 Billion by 2036 on Rising Aviation Innovation

Aircraft Topcoats for Lightning and EMI Protection Market to Reach USD 0.6 Billion by 2036, Driven by Aerospace Electrification and Advanced Composite Aircraft Adoption

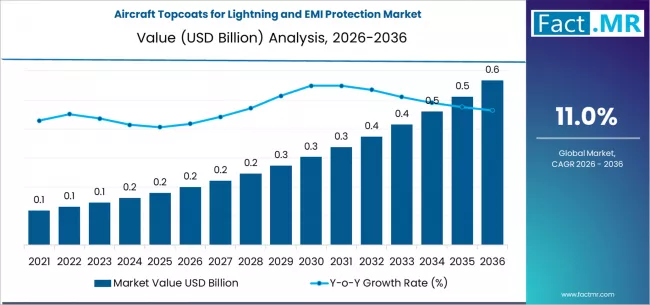

The global Aircraft Topcoats for Lightning and EMI Protection Market is poised for substantial expansion, with market valuation projected to increase from USD 0.2 billion in 2026 to USD 0.6 billion by 2036, registering a robust CAGR of 11.0% during the forecast period. Growing integration of advanced avionics, increasing use of composite airframes, and rising regulatory emphasis on aircraft safety and electromagnetic compatibility are accelerating demand for high-performance conductive topcoat technologies.

Modern aircraft platforms require sophisticated lightning strike protection and electromagnetic interference (EMI) shielding solutions to safeguard critical electronic systems. As aerospace manufacturers continue to prioritize lightweight materials and next-generation aircraft architectures, advanced conductive topcoats are becoming an essential component of aircraft design and operational reliability.

Market Overview and Strategic Insights

The Aircraft Topcoats for Lightning and EMI Protection Market is emerging as a critical segment within the aerospace coatings industry. The increasing deployment of carbon-fiber-reinforced composites and advanced electronics across commercial and defense aircraft is creating sustained demand for conductive surface protection technologies.

Key growth factors include:

- Rising adoption of composite aircraft structures

- Increasing aircraft electrification and digitalization

- Growing demand for lightning strike protection systems

- Enhanced regulatory focus on aircraft safety and EMI compliance

- Expansion of commercial aviation fleets worldwide

- Technological advancements in conductive coating formulations

The market is expected to create an absolute dollar opportunity of approximately USD 0.4 billion between 2026 and 2036.

Key Market Projections

|

Metric |

Value |

|

Market Size (2026) |

USD 0.2 Billion |

|

Forecast Market Size (2036) |

USD 0.6 Billion |

|

CAGR (2026-2036) |

11.0% |

|

Leading Segment |

Conductive Topcoat Systems |

|

Segment Share |

50.6% |

|

Leading Substrate Segment |

Composite Structures |

|

Segment Share |

48.4% |

|

Fastest Growing Country |

China |

|

China CAGR |

12.8% |

Analyst Perspective

“Aircraft manufacturers are increasingly adopting conductive topcoat systems that provide both lightning strike mitigation and EMI shielding capabilities. As aerospace platforms become more electrically intensive and composite-rich, these advanced coatings are transitioning from optional enhancements to mission-critical technologies,” says a Fact.MR analyst.

Competitive Landscape and Market Share Analysis

The competitive environment remains moderately consolidated, characterized by global aerospace coatings specialists, advanced materials providers, and electromagnetic protection technology developers.

Key market participants include:

- PPG Industries

- AkzoNobel

- Sherwin-Williams

- Solvay

- 3M

- Henkel

- Toray

- Hexcel

- Arkema

- Dow

Industry leaders continue investing in:

- Conductive nanomaterial technologies

- Aerospace-qualified coating formulations

- Multi-functional protective systems

- Lightweight EMI shielding solutions

- Long-term OEM partnerships

Competitive differentiation increasingly depends on coating conductivity performance, durability, certification capabilities, and integration compatibility with advanced composite structures.

Production Analysis vs. Consumption Economy

Production Hubs

Manufacturing activities are concentrated across:

- United States

- Germany

- France

- United Kingdom

- Japan

- China

These countries possess advanced aerospace manufacturing ecosystems, established coating technology capabilities, and strong aircraft OEM presence.

Consumption Trends

Demand is expanding rapidly across:

- Commercial aircraft OEMs

- Defense aviation programs

- Maintenance, Repair, and Overhaul (MRO) facilities

- Tier-1 aerostructure manufacturers

North America currently leads consumption due to extensive aerospace manufacturing infrastructure, while Asia-Pacific is witnessing accelerated adoption driven by aircraft fleet expansion and indigenous aerospace development programs.

Supply Chain and Value Chain Assessment

The market's value chain includes:

Raw Material Suppliers → Specialty Chemical Manufacturers → Conductive Material Providers → Aerospace Coating Manufacturers → Aircraft OEMs → Tier-1 Suppliers → MRO Service Providers → End Users

Critical raw materials include:

- Conductive nanoparticles

- Carbon-based additives

- Metallic conductive fillers

- Advanced polymer resins

- Specialty aerospace-grade chemicals

Supply chain resilience is becoming increasingly important as aerospace manufacturers seek secure sourcing strategies for high-performance coating materials.

Strategic Procurement Intelligence

Procurement decisions are increasingly influenced by:

- Coating conductivity performance

- Aerospace certification requirements

- Lifecycle maintenance costs

- OEM qualification standards

- Supplier reliability

- Environmental compliance requirements

Long-term supply agreements between coating manufacturers and aircraft OEMs are becoming more common to ensure material consistency and regulatory compliance.

Country Opportunity Assessment

China

China is projected to be the fastest-growing market, expanding at a CAGR of 12.8% through 2036. Growth is supported by:

- Expanding domestic aerospace production

- Growing commercial aviation fleet

- Government investments in aerospace technology

- Increased adoption of advanced aircraft materials

United States

The U.S. remains the largest aerospace technology hub globally, benefiting from:

- Strong aircraft manufacturing activity

- Advanced defense programs

- High adoption of composite aircraft structures

- Continuous aerospace innovation investments

Germany

Germany continues to offer significant opportunities through:

- Advanced aerospace engineering capabilities

- Strong regulatory compliance standards

- Growing focus on aircraft efficiency and safety

Technology and Innovation Outlook

Emerging technology trends include:

- Nanotechnology-enabled conductive coatings

- Graphene-enhanced EMI shielding systems

- Lightweight multifunctional topcoat formulations

- Self-healing protective coatings

- Smart surface monitoring technologies

- Advanced lightning strike dissipation systems

Future innovation will focus on achieving higher conductivity levels while reducing coating weight and maintenance requirements.

Investment Outlook

Investments are expected to accelerate in:

- Conductive material development

- Aerospace coating R&D

- Composite aircraft protection technologies

- EMI shielding innovations

- Sustainable aerospace coatings

The market presents attractive opportunities for chemical manufacturers, aerospace suppliers, specialty materials providers, and technology investors seeking exposure to next-generation aviation infrastructure.

Need Customized Market Intelligence?

Fact.MR offers customized research solutions tailored to specific business objectives, including:

- Country-specific market analysis

- Competitive benchmarking

- Supply chain intelligence

- Procurement strategy assessment

- Technology landscape evaluation

- Investment opportunity mapping

Other Related Report:

Controlled Release Fertilizer Market

Paper Packaging Materials Market

About Fact.MR

Fact.MR is a leading market research and consulting firm providing actionable intelligence across industries worldwide. Through comprehensive market analysis, data-driven insights, and strategic consulting expertise, Fact.MR helps organizations identify emerging opportunities and make informed business decisions.

Media Contact

Fact.MR

US Sales Office:

11140 Rockville Pike,

Suite 400,

Rockville, MD 20852,

United States

Phone: +1 (628) 251-1583

Categories

Read More

Buy Verified Bybit Accounts Buy Verified Bybit Accounts In the ever-evolving world of cryptocurrency trading, many investors are seeking reliable and efficient platforms to maximize their potential. One popular choice among traders is Bybit, a leading exchange known for its advanced features and user-friendly interface. For those looking to enhance their trading experience, it’s...

(圖/ 中華超傳媒) 為強化雲嘉南地區創新創業能量,國立中正大學創新創業基地(中正創基)28日於校內創新創業基地大會議廳舉辦「嘉義創新創業聯盟第九次大會」,集結產官學研代表、新創團隊與地方單位共襄盛舉,交流基地年度成果並探討跨域合作新契機。活動由校長蔡少正開場致詞,副校長洪新原則簡報基地近年推動成果,現場氣氛熱絡。 MGBOX (圖/ 中華超傳媒) 中正創基今年在創業競賽與政府補助計畫中表現亮眼。其中,於教育部青年發展署114年度 U-start 創新創業計畫第二階段競賽中,「濾淨玻璃」與「Emere IDE」兩支輔導團隊成功脫穎而出。 (圖/ 中華超傳媒) 濾淨玻璃團隊以廢棄玻璃再製成高效能水處理濾材,兼具高過濾效能、耐用度及營運成本低等優勢,第一階段獲補助50萬元後,第二階段再獲70萬元,累計補助達120萬元。另一團隊 Emere IDE...