Oil Spill Management Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

"Latest Insights on Executive Summary Oil Spill Management Market Share and Size

1. Introduction

In recent decades, the world’s heavy reliance on oil for energy, transportation, and industrial uses has come with a serious environmental risk: oil spills. Whether from offshore drilling platforms, pipelines, tanker accidents, or operational leaks, oil spills can inflict severe damage on marine and coastal ecosystems, fisheries, tourism, and local communities. The Oil Spill Management Market — encompassing prevention, response, cleanup, remediation, and support services — plays a critical role in mitigating these risks.

As governments and corporations face increasing scrutiny on environmental responsibility, this market has become ever more relevant. The growing emphasis on sustainability, stricter regulations, and higher public awareness have elevated demand for robust oil spill management capabilities. Moreover, as oil and gas activities expand — especially in deepwater and Arctic regions — the exposure to spill risk rises, reinforcing the importance of preparedness and response capabilities.

Analysts estimate that the global oil spill management market was valued around USD 150–162 billion in 2024 . Projections foresee a moderate growth trajectory, with compound annual growth rates (CAGR) in the range of 2.5 % to 3.3 % over the 2025–2030 (or 2032/2033) period. This growth will be driven by stricter environmental regulation, rising spill incidents, and technological innovation.

Get strategic knowledge, trends, and forecasts with our Oil Spill Management Market. Full report available for download:

https://www.databridgemarketresearch.com/reports/global-oil-spill-management-market

2. Market Overview

Scope & Size

The oil spill management market covers a wide set of services and technologies: preventive measures (e.g. leak detection, pipeline integrity monitoring), spill response (containment, recovery, dispersants, bioremediation), contingency planning, consulting and training, and post-spill remediation and restoration. It also spans various spill types (marine, pipeline, rail, onshore) and zones (offshore, onshore, coastal) across different geographies.

While precise numbers vary by source, a representative estimate places the 2024 market at USD 150.6 billion with a projected rise to USD 193.7 billion by 2033, implying a CAGR of ~2.55 % over 2025–2033 IMARC Group. Another authoritative estimate places the market at USD 162.0 billion in 2024 and forecasts it to reach USD 207.95 billion by 2032 (CAGR ~3.17 %) Data Bridge Market Research. Others project somewhat more conservative growth: for instance, IMARC suggests a ~2.5 % CAGR over the next decade IMARC Group.

Given the inherent uncertainty and diversity of sub-segments, a reasonable working range is that the total market will grow from USD 150–165 billion today to USD 190–210 billion by around 2030–2033.

Historical Trends & Current Positioning

Over the past decade, the oil spill management sector has evolved from being reactive (focused on cleanup) to more integrated, with preventive and contingency planning gaining prominence. Early growth was spurred by high-profile disasters (e.g. Deepwater Horizon, Exxon Valdez) and the global push for environmental accountability. More recently, improvements in sensor technologies, remote monitoring, and digital modeling have enabled better leak detection and risk management, shifting investments upstream.

In current positioning, the market is moderately fragmented: a few large global service providers coexist with many regional/niche players, particularly in vessel operations, booms, sorbents, and consulting. The key differentiation now is not just capabilities, but speed, reliability, regulatory compliance, and ecosystem integration.

Demand–Supply Dynamics

Demand side: Demand is driven by oil & gas operators (exploration, production, transport), governments enforcing spill liability, and insurance/financing conditions that require environmental risk mitigation. Rising offshore/deepwater exploration, pipeline build-outs, and shipping traffic amplify exposure. Public pressure and ESG mandates further push operators to invest in stronger management systems.

Supply side: Suppliers include specialized equipment manufacturers (e.g. booms, skimmers, dispersants), technology providers (sensors, drones, modeling software), and service firms (response contractors, consulting, training). The supply base must maintain readiness, logistics capability, and regional presence to deliver rapid response. Key supply constraints include high capital cost, training, mobilization delays, and regulatory permitting.

Because response speed is critical, there is a premium on supply chains with regional response bases, strategically placed inventories, and satellite/back-up assets. Some clients contract standby services in key zones, which provides more predictable revenue streams for suppliers.

Overall, the market sees moderate demand growth, while supply competition is intensifying (especially in new geographies and technology niches). The balance leans toward favorable conditions for innovative and agile providers.

3. Key Market Drivers

Several major drivers underpin continued growth in oil spill management:

1. Stricter Environmental & Safety Regulations

Governments globally have tightened regulations mandating oil spill prevention, response preparedness, and liability regimes. In many jurisdictions, oil companies must maintain approved contingency plans, standby equipment, and bonding. Fines and reputational damage from noncompliance are significant. This regulatory pressure pushes operators to engage professional spill management firms.

2. Rising Oil & Gas Exploration, Transport & Infrastructure

Expansion of offshore and onshore drilling, pipeline networks, and shipping routes increases the probability of spills. In frontier geographies — deepwater, Arctic, or remote coasts — risk is higher and demands specialized capabilities. As oil production and trade volumes grow, spill management becomes a scaling necessity.

3. Technological Advancements

Advances in sensors, remote monitoring, drones, satellite imaging, and AI-based modeling have enhanced early detection, predictive spill modeling, and response optimization. Such technologies reduce response time, improve precision, and lower costs, making spill management more efficient and attractive.

For example, real-time satellite sensing combined with AI anomaly detection can flag leaks earlier, enabling quicker containment. Drones and autonomous surface vessels support remote assessments. Bioremediation agents and novel dispersants continue to improve cleanup effectiveness. Wiley Online Library+2ScienceDirect+2

4. ESG, Corporate Reputation & Insurance Pressure

Operators face growing ESG (environmental, social, governance) scrutiny from investors, NGOs, and consumers. A single spill can severely damage reputation, lead to litigation, and devalue stock. Insurance underwriters often require robust spill management plans and performance records as a condition for coverage. This drives firms to engage proactive and credible spill management partners.

5. Increasing Public & Stakeholder Awareness

Media coverage, activism, and public expectations heighten pressure on companies and regulators to respond swiftly and transparently to spill incidents. Governments may demand independent verification. The need for credible, documented spill-management capability is now more crucial than ever.

6. Investments & Funding Support

Some governments provide funding, subsidies, or mandates to support national spill-response capacity, coastal protection, and marine restoration. Public–private partnerships, grants for R&D in cleanup technologies, and funds for coastal resilience can indirectly stimulate market growth.

4. Market Challenges

Despite the opportunity, there are notable restraints and risks:

1. High Capital & Operational Costs

Maintaining rapid-response capacity (vessels, booms, skimmers, dispersants, personnel) is capital-intensive. Mobilization costs, logistics, warehousing, and periodic drills impose recurring expenses. Some spill events require mobilizing expensive assets from distant bases, eroding profitability.

2. Geographic & Logistical Constraints

In remote, harsh, or deepwater locations, logistics (transportation, access, weather, permitting) complicate response. Arctic, polar, or equatorial storms may render equipment ineffective. The inability to pre-stage assets in all zones is a bottleneck.

3. Regulatory & Permitting Hurdles

Cross-jurisdictional regulation, environmental permitting delays, import/export clearance of chemicals, and ownership of response assets can complicate operations. Differences in acceptable dispersant types, waste disposal rules, and environmental impact thresholds vary regionally and must be navigated carefully.

4. Competitive Pressure & Margin Compression

As more players enter with differentiated technologies or regional capabilities, price competition intensifies. Clients may demand fixed-price or performance-based contracts, squeezing margins.

5. Response Uncertainty & Liability Risk

Oil spill events are unpredictable in scale, complexity, and environmental conditions. Underestimating severity can lead to cost overruns and reputation damage. Liability is high — any misstep can lead to litigation, fines, or reputational loss.

6. Limited Data & Monitoring Gaps

In many regions, baseline environmental data, real-time monitoring, and modeling capabilities are inadequate. This limits planning, decision making, and rapid change response. MDPI+1

7. Technology & Material Limitations

Not all technologies are equally effective under all conditions. Dispersants may harm some ecosystems; mechanical recovery has diminishing returns in rough seas; bioremediation is slower. Ongoing R&D is needed to fill gaps.

5. Market Segmentation

We can segment the oil spill management market along three common axes: by type/technology, by application/use case, and by region.

By Type / Technology

Mechanical containment & recovery: booms, skimmers, containment vessels, sorbents

Chemical methods: dispersants, gelling agents, emulsifiers

Biological / bioremediation: microbial degradation, enzymatic formulations

Physical / manual: manual cleanup, absorbent pads, shoreline protection

Monitoring & detection technologies: sensors, drones, satellite systems, leak detection

Consulting, training & software: modeling, simulation, planning, drills

Among these, mechanical containment and recovery remain the dominant segment due to their universal applicability. Monitoring & detection is one of the fastest-growing sub-segments, driven by digitalization and early-warning needs.

By Application / Use Case

Prevention & Monitoring: leak detection, pipeline integrity, remote sensors

Spill Response / Containment: rapid deployment of containment booms, skimmers, dispersants

Contingency Planning & Consulting: risk assessment, drills, training, planning

Post-spill Remediation & Restoration: cleaning, soil/water remediation, ecological rehabilitation

Waste Disposal & Treatment: handling collected oil and contaminated materials

In growth terms, the prevention/monitoring and post-spill remediation segments are gaining share, as more customers invest upstream to reduce risk and downstream to repair damage.

By Region

North America (USA, Canada)

Europe (Western & Eastern)

Asia-Pacific (APAC) (China, India, Southeast Asia, Australia)

Latin America (Brazil, Mexico, others)

Middle East & Africa (MEA)

Currently, North America and Europe hold significant shares due to high regulatory demands, mature oil industries, and environmental consciousness. APAC is the fastest-growing region, driven by rising energy demand, offshore exploration, and expanding maritime trade. Latin America and ME&A are poised for growth as infrastructure and oil/gas activities increase, though volatility and regulatory gaps pose risks.

6. Regional Analysis

North America

The U.S. is a mature market with tight regulatory oversight (e.g. U.S. Coast Guard, EPA). Operators routinely maintain spill response agreements and standby capacity. Canada also has strong regulatory frameworks. Growth is steady, driven by aging infrastructure, pipeline expansions, and offshore activity (e.g. Gulf of Mexico). Asset deployment, partnerships with government agencies, and training services are key differentiators.

Europe

Europe leads in regulatory stringency (EU directives, marine protection zones) and environmental activism. The North Sea and Baltic Sea regions require high readiness. Countries such as Norway, UK, Netherlands, and Denmark host advanced spill response capabilities. Demand is stable but premium on technology-driven, low-impact solutions (e.g. bioremediation, real-time monitoring).

Asia-Pacific (APAC)

This is an emerging hotspot. Nations like India, China, Southeast Asia, Australia, and Malaysia are expanding offshore drilling and shipping. Environmental incidents and coastal sensitivity drive demand. Many operators are entering into contracts for baseline monitoring, response fleet development, and technology transfer. This region often offers the fastest revenue growth.

Latin America

Latin American markets such as Brazil, Mexico, and Argentina are increasing oil/gas activities and pipeline networks. Environmental disasters in ecologically sensitive zones (e.g. Amazon delta, Atlantic coast) trigger demand for spill management. However, economic and regulatory instability may slow consistent investment.

Middle East & Africa (MEA)

Oil & gas is central in the Middle East, creating inherent risk exposure. Gulf states (UAE, Saudi Arabia, Qatar) are already developing spill-response capacity. In Africa, countries such as Nigeria, Angola, and others see repeated spill incidents, heightening demand. However, lack of infrastructure, instability, and funding constraints are challenges.

Overall, while North America and Europe remain stable pillars, APAC, Latin America, and MEA represent high-potential growth zones.

7. Competitive Landscape

Key players in the oil spill management domain include (but are not limited to):

Oil Spill Response Limited (OSRL)

Cura Emergency Services / CURA Group

Fender & Spill Response Services

SkimOil

OMI Environmental Solutions

Osprey Spill Control

American Green Ventures

National Oilwell Varco (NOV) – spill equipment divisions

Ecolab (in remediation / chemical agents)

Cameron / Schlumberger (response or containment equipment)

Control Flow Inc.

These companies compete through a mix of strategies:

Innovation & technology leadership: Some firms emphasize advanced monitoring, autonomous response, AI modeling, and novel cleanup chemistries to differentiate.

Geographic partnerships / regional coverage: Establishing response bases in key coastal zones through alliances or local acquisitions helps reduce response time.

Mergers & acquisitions: Consolidation (smaller niche specialists absorbed by larger service providers) helps scale capabilities and widen geographic reach.

Long-term contracts & retainer models: Rather than solely reacting, providers secure multi-year preparedness contracts with large oil operators or governments.

Performance / outcome-based pricing: Some providers offer contracts with penalties/rewards tied to containment speed, percentage recovery, or environmental impact.

Training, consulting & certification services: Service providers increasingly bundle training, drills, certification, and planning services to become full-spectrum partners.

In comparative terms, large players can leverage capital scale and cross-region coverage, while niche players may excel in innovation, speed, or specialization (e.g. Arctic response, drone-based monitoring). The bar for entry is high, given capital, logistics, and regulatory requirements.

8. Future Trends & Opportunities

Looking ahead over the next 5–10 years, the oil spill management market is poised for evolution:

Accelerated Digital & Autonomous Response

Expect deeper integration of AI, machine learning, autonomous vessels or drones, predictive modeling, and real-time optimization. The ability to simulate spill trajectories in real time, optimize deployment, and self-adapt during operations will be critical.

Decentralized & Pre-Staged Response Hubs

More providers and governments will pre-stage assets and warehouses near high-risk zones (e.g. shipping chokepoints, offshore basins). This reduces response time and logistical drag.

Green / Eco-Friendly Cleanup Solutions

Bioremediation, enzyme-based agents, and low-impact dispersants will gain share over harsher chemical methods. “Eco-friendly cleanup” will be a differentiator in sensitive zones.

Modular & Flexible Deployment Systems

Portable, modular spill response units — e.g. containerized boom kits, mobile skimming units — allow rapid deployment to new or unexpected sites.

Integration with Carbon & Environmental Markets

As carbon accounting, marine protection, and biodiversity credits gain traction, spill prevention and habitat restoration may become monetized. Operators might invest in proactive spill management partly as a compliance or offset strategy.

Public–Private & Multi-Stakeholder Models

Governments may partner with private firms to subsidize national response capacity, share infrastructure, or coordinate regional “centers of excellence.” Cross-border spill risk zones may drive multinational cooperation.

Expansion into Adjacent Remediation Markets

Providers may branch into broader environmental remediation markets (e.g. soil/groundwater cleanup, chemical spill response), leveraging their logistics and environmental technology expertise.

Niche & Extreme-Environment Opportunities

Markets such as Arctic, polar, deep-sea, mangrove, and coral reef zones will demand specialized capabilities, creating premium segments.

Demand from Non-Oil Sectors

While oil dominates, other sectors (chemicals, shipping, petrochemicals) may increasingly demand spill management capabilities, broadening addressable demand.

9. Conclusion

The oil spill management market occupies a critical intersection of environmental stewardship, industrial risk, and regulatory compliance. Despite moderate growth forecasts (CAGR ~2.5 %–3.3 %), the market’s real value lies in its strategic importance, high-stakes operations, and evolving technological frontier.

Key takeaways:

The market is sizable — estimated around USD 150–162 billion in 2024, expected to grow to USD 190–210 billion by 2030–2033.

Drivers include stricter regulation, expanding oil infrastructure, ESG pressures, and technological innovation.

Challenges include high costs, logistical constraints, regulatory complexity, and competition.

Market segmentation reveals strong growth in monitoring/prevention and remediation, with mechanical recovery still dominant.

APAC, Latin America, and MEA are emerging growth regions, though North America and Europe remain mature strongholds.

Competitive strategies center on geographic reach, innovation, contracts, and bundling services.

Future opportunities lie in digital transformation, eco-friendly methods, modular systems, and integration with broader environmental markets.

For businesses, investors, and policymakers:

Businesses / service providers should invest in R&D, build regional response hubs, and form long-term contracts with operators and governments.

Oil & gas operators should treat spill management not as a cost, but as core risk mitigation and ESG necessity — partner with high-caliber providers early.

Investors may find opportunity in niche technology innovators (e.g. AI monitoring, autonomous cleanup vessels, bioremediation) or platform companies that scale geographically.

Policy makers must harmonize regulations, encourage public–private response capacity, and incentivize green technology adoption.

In summary, the oil spill management market will remain a vital but challenging domain — one that demands constant innovation, operational excellence, and strategic vision. Stakeholders who understand the evolving landscape, commit to capabilities, and align with emerging trends will be best positioned to capture long-term potential.

FAQ (Frequently Asked Questions)

Q1: What is the projected CAGR for the oil spill management market?

A: Sources generally estimate a CAGR between 2.5 % and 3.3 % over the 2025–2030 (or 2032/2033) period. P&S Intelligence+4IMARC Group+4Data Bridge Market Research+4

Q2: Which region is expected to grow fastest?

A: The Asia-Pacific region is often cited as the fastest-growing, driven by expanding offshore drilling, maritime traffic, and rising regulatory and environmental awareness.

Q3: Which segment (technology or service) is gaining importance?

A: While mechanical containment and recovery remain foundational, segments like monitoring & detection, bioremediation, and consulting/training are increasing their share.

Q4: What are the main barriers to growth?

A: Key barriers include high capital/operational cost, logistical challenges in remote zones, regulatory and permitting complexity, and competition-induced margin pressure.

Q5: What opportunities exist for new entrants?

A: Promising opportunities lie in niche or extreme-environment technologies (e.g. Arctic cleanup, autonomous drones), green remediation methods, and digital platforms for spill modeling and management.

Browse More Reports:

Global Candida Infections Drugs Market

Global Capnography Equipment Market

Global Cardiomyopathy Market

Global Cataplexy Treatment Market

Global Cattle and Porcine Swine Reproductive Diseases Market

Global Cell Based Assays Market

Global Cell Sorting Market

Global Cerebral Edema Treatment Market

Global Cervical Cancer Drug Market

Global Chatbot Market

Global Chilled and Deli foods Market

Global Chlorinated Rubber Coatings Market

Global Chocolate Milk Shake Market

Global Chromatography Food Testing Market

Global Chylomicronemia Market

Global Full Spectrum Cannabidiol (CBD) Infused Edibles Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com

"

閱讀更多

In today's rapidly advancing industrial environment, companies are constantly striving for ways to optimize fluid control systems for better performance, efficiency, and sustainability. Naishi, a leading Three-Way Ball Valve Factory In China, is at the forefront of this revolution, providing cutting-edge valve solutions that integrate intelligent automation and environmentally conscious design....

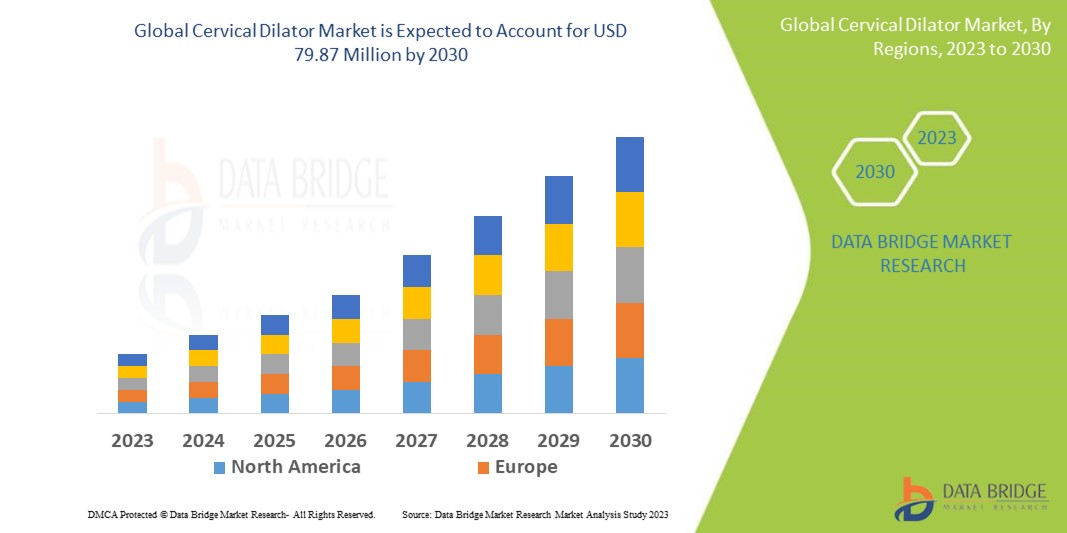

"Executive Summary Cervical Dilator Market Size and Share: Global Industry Snapshot CAGR Value The global cervical dilator market size was valued at USD 67.59 million in 2024 and is expected to reach USD 84.43 million by 2032, at a CAGR of 2.82% during the forecast period For an actionable market insight and lucrative business strategies, a faultless...

Introduction In the digital era, Gmail accounts are not just personal email addresses—they’re the backbone of online business, marketing, and brand management. Whether you’re running campaigns, managing multiple YouTube channels, or building online profiles for clients, a verified Gmail account is essential. Creating new Gmail accounts repeatedly can be tedious,...

Festive Collectible Introduction Scopely continues to embrace the festive season by introducing a delightful new collectible in Monopoly GO: the Camplight Token. This charming lantern-shaped item evokes feelings of cozy nights spent under the stars, adding a touch of warmth and nostalgia to your collection. It perfectly complements the current Cozy Comforts theme, making it an essential piece...