Dicing Blades for Semiconductor Packaging Market to Reach USD 446.7 Million by 2032 at 6.7% CAGR Driven by Advanced Packaging Expansion

Global Dicing Blades for Semiconductor Packaging Market was valued at USD 267.3 million in 2024 and is projected to reach USD 446.7 million by 2032, expanding at a CAGR of 6.7% during the forecast period 2026–2034. Market growth reflects broader semiconductor industry expansion, supported by rising demand for precision wafer singulation in advanced packaging environments.

Dicing blades are precision cutting tools used in semiconductor manufacturing for wafer singulation, the process of separating individual dies from processed silicon wafers. These blades incorporate diamond abrasives to achieve micron-level cutting accuracy while minimizing chipping, kerf loss, and thermal damage. The market is primarily segmented into hubless and hub-type blades, with hubless variants accounting for approximately 62% of global share due to superior performance in thin-wafer and high-precision applications.

👉 Access the complete industry analysis and demand forecasts here:

https://semiconductorinsight.com/report/dicing-blades-for-semiconductor-packaging-market/

Market Definition and Dynamics

The dicing blades market operates as a critical enabler within the semiconductor packaging value chain. As advanced packaging technologies such as 3D IC integration and fan-out wafer-level packaging (FOWLP) scale globally, demand for ultra-thin, high-precision cutting tools continues to increase. Transition toward sub-7nm nodes and wafer thinning below 50μm further intensifies requirements for blade precision and reduced subsurface damage.

Market Drivers

- Expansion of the global semiconductor industry supporting increased wafer processing volumes

- Growing adoption of advanced packaging technologies including 3D IC and FOWLP

- Rising transition to 300mm wafers requiring extended blade life and cutting stability

- Increasing IoT and 5G semiconductor production driving higher wafer throughput

Market Restraints

- Volatility in synthetic diamond pricing and tungsten carbide substrate availability

- High production costs impacting profitability in price-sensitive markets

- Technical challenges in heterogeneous integration and ultra-thin wafer dicing

Market Challenges

- Shortage of skilled professionals in precision machining and materials science

- Compatibility constraints with diverse dicing saw equipment platforms

- Operational downtime concerns during transition to ultra-thin blade configurations

Market Opportunities

- Rapid growth of silicon carbide (SiC) and gallium nitride (GaN) power devices requiring specialized cutting solutions

- Integration of smart blade technologies with embedded wear monitoring sensors

- Automation and Industry 4.0 adoption improving predictive maintenance and yield optimization

Competitive Landscape

The global dicing blades market is moderately consolidated, with leading manufacturers leveraging proprietary diamond abrasive technologies and precision engineering expertise. Market competition centers on blade durability, kerf optimization, and compatibility with advanced wafer processing equipment.

List of Key Dicing Blades Manufacturers

- DISCO Corporation

- ADT (Advanced Dicing Technologies)

- Kulicke & Soffa (K&S)

- Ceiba Technologies

- UKAM Industrial Superhard Tools

- Kinik Company

- ITI (International Tool Industries)

- Asahi Diamond Industrial

- DSK Technologies

- ACCRETECH

- Zhengzhou Sanmosuo

- Shanghai Sinyang Semiconductor

Segment Analysis

By Type

- Hubless Type

- Resin-bonded

- Metal-bonded

- Electroplated

- Others

- Hub Type

- Nickel-based

- Phenolic resin-based

- Others

By Application

- 300mm Wafer

- 200mm Wafer

- Others (150mm and smaller wafers)

By Material

- Diamond Blades

- CBN (Cubic Boron Nitride) Blades

- Others (Abrasive-based)

By End-User

- Foundries

- IDMs (Integrated Device Manufacturers)

- OSAT Providers

- Research Institutions

Regional Insights

Asia-Pacific accounts for over 65% of global dicing blade consumption, supported by concentrated semiconductor manufacturing in China, Taiwan, South Korea, and Japan. North America benefits from renewed domestic semiconductor investments and strong adoption of hubless blades for advanced nodes. Europe maintains steady demand in automotive and industrial semiconductor applications, emphasizing high-performance diamond-embedded blade solutions. South America represents a developing market primarily focused on backend packaging operations, with price-sensitive demand centered around hub-type blades for 200mm wafer processing.

👉 Access the complete industry analysis and demand forecasts here:

https://semiconductorinsight.com/report/dicing-blades-for-semiconductor-packaging-market/

📄 Download a free sample to explore segment dynamics and competitive positioning:

https://semiconductorinsight.com/download-sample-report/?product_id=103368

About Semiconductor Insight

Semiconductor Insight is a global intelligence platform delivering data-driven market insights, technology analysis, and competitive intelligence across the semiconductor and advanced electronics ecosystem. Our reports support OEMs, investors, policymakers, and industry leaders in identifying high-growth markets and strategic opportunities shaping the future of electronics.

🌐 https://semiconductorinsight.com

🔗 LinkedIn:Follow Us

📞 International Support: +91 8087 99 2013

Categories

Read More

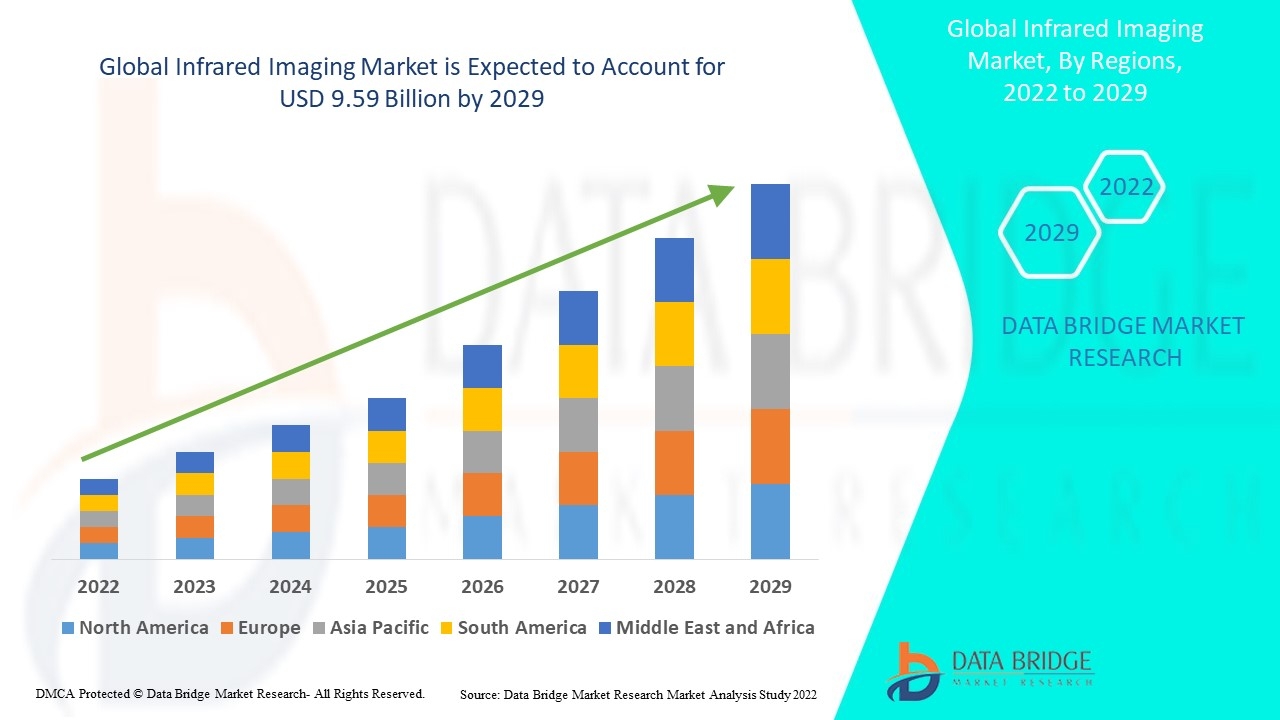

"Executive Summary Infrared Imaging Market Size and Share Across Top Segments Data Bridge Market Research analyses that the infrared imaging market will exhibit a CAGR of 6.85% for the forecast period of 2022-2029. This Infrared Imaging Market report is composed of a myriad of factors that have an influence on the market and include industry insight and critical success factors...

If you want to buy Facebook accounts, you probably want a quick, safe, and easy solution. Maybe you need to run ads, sell on Marketplace, or manage multiple pages. Whatever your reason, buying Facebook accounts can save you time and help you avoid the headaches of starting from scratch. In this guide, I’ll show you why it’s smart to buy Facebook accounts, how it works, and how to...

If you want to buy Facebook aged account, you’re probably looking for a shortcut to trust, speed, and results. You don’t want to wait for a new account to “grow up.” You want something that works right now. In this guide, I’ll show you why it’s smart to buy Facebook aged account, how it works, and how to do it safely—without any jargon or confusion.✅...