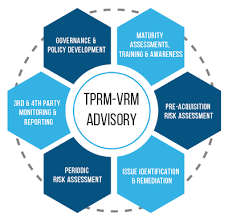

Identifying Core Drivers of the Third Party Risk Management Market

The engine propelling the rapid and pervasive adoption of third-party risk management solutions is fueled by a set of powerful and interconnected Third Party Risk Management Market Drivers that have fundamentally altered the corporate risk landscape. These drivers are not temporary market fluctuations but deep, structural changes in the global business environment that have elevated the management of the extended enterprise from a peripheral concern to a central pillar of corporate governance. The most potent and undeniable driver is the relentless and ever-expanding wave of regulatory and compliance mandates. In the wake of numerous high-profile data breaches and financial crises that were traced back to third-party failures, regulators and industry bodies across the globe have responded with a host of stringent new rules. From the financial sector's OCC Bulletin 2013-29 in the U.S. to the EU's General Data Protection Regulation (GDPR) and the Digital Operational Resilience Act (DORA), the message from authorities is clear and unambiguous: organizations are ultimately accountable for the risks introduced by their vendors, partners, and suppliers. The threat of severe financial penalties, public censure, and increased regulatory scrutiny for non-compliance acts as a powerful, non-discretionary driver that forces companies, particularly in regulated industries, to invest in formal, auditable TPRM programs and the technologies that support them.

The second critical driver, which is inextricably linked to the first, is the dramatic and visible increase in the frequency and impact of third-party-related security incidents. The modern attack surface has fundamentally shifted. Cyber adversaries, recognizing that large enterprises have often hardened their own direct defenses, are now systematically targeting the "soft underbelly" of the digital supply chain: smaller, less secure vendors who have trusted access to the larger organization's data and networks. High-profile incidents like the SolarWinds and Kaseya breaches were classic examples of supply chain attacks, where the compromise of a single software vendor led to the downstream compromise of thousands of their customers. These incidents have served as a brutal wake-up call for boards and executives, demonstrating in the starkest possible terms that their organization's security is only as strong as its weakest link. This elevated and well-publicized threat landscape is a powerful driver of demand, compelling companies to move beyond simple compliance and invest in TPRM solutions that can provide genuine visibility into the cybersecurity posture of their third parties and offer early warnings of potential compromise.

A third, and profoundly strategic, driver is the fundamental change in business operating models brought about by digital transformation and the wholesale shift to outsourcing. In the pursuit of cost-efficiency, agility, and access to specialized skills, modern enterprises have outsourced a vast array of their core business functions to third-party providers. Critical operations that were once performed in-house, such as IT infrastructure (now hosted in the cloud by AWS or Azure), customer relationship management (managed via Salesforce), human resources, and even core elements of product development, are now entrusted to external partners. While this model offers significant strategic advantages, it also means that an organization's most sensitive data and its ability to function are now deeply and operationally dependent on the resilience and security of its key third parties. A significant outage or security failure at a single critical SaaS provider could bring a company's entire operations to a grinding halt. This deep level of operational entanglement is a powerful driver for TPRM, as it creates a business continuity imperative to continuously assess, monitor, and manage the risks associated with these mission-critical dependencies.

閱讀更多

In solar PV combiner boxes, EV charging stations, and outdoor telecom cabinets, the Cable Gland Adaptor offers a practical solution for thread compatibility and long-term sealing. Appearing again mid-sentence, the Cable Gland Adaptor ensures secure mechanical transitions between mismatched gland types without jeopardizing IP ratings. Zhejiang Hongjuesi Connectors (HJSI) delivers adaptors...

(圖/ 新北市政府) 淡北道路工程持續推進,四大工區全面展開施工。新北市長侯友宜今(10)日前往關渡大橋觀景台視察整體進度時表示,目前工程已完成約14.62%,感謝施工團隊全力趕工、穩健推進,預計可於118年6月如期完工。屆時通車後,將大幅提升淡水地區交通量能,改善通勤族長期受困的壅塞問題。 (圖/ 新北市政府) 侯友宜指出,淡北道路全長5.45公里,四大工區同步展開建設,市府將持續緊盯工程進度,與施工團隊並肩作戰,逐一克服挑戰。他並責成相關單位與施工團隊務必加強安全防護措施,確保工程品質與人員安全,同時優化周邊道路環境與交通維持計畫,以降低施工期間對當地交通造成的影響。 (圖/ 新北市政府)...

If you run a hotel, tour, or restaurant, you already know how much travelers rely on TripAdvisor. Many guests scroll reviews in bed, compare ratings on their phone, then book within minutes. So when growth is slow and competitors race ahead, some owners start to wonder if they should Buy TripAdvisor Reviews to speed things up. It sounds quick and simple. This guide explains what buying reviews...

Buy Verified PayPal Accounts Introduction to PayPal In today's digital world, PayPal stands out as a leading platform for online transactions. Whether you're shopping on e-commerce sites, sending money to friends, or receiving payments for freelance work, having a reliable payment method is crucial. But there’s one thing that can take your PayPal experience to the next level:...